The state of the Dollar is in the hands of the Fed: a backlash or deeper drop?

July 29, 2020 @ 12:09 +03:00

Today, Federal Reserve will publish the results of the two-day scheduled meeting, with Chairman Powell delivering a press conference 30 minutes afterwards. No changes in the rate or stimulus programs are expected. However, it will be a crucial meeting for the markets.

Investors and traders will be closely watching how the Fed’s assessment of the prospects for economic recovery will change. In June, when the committee published its quarterly forecasts, there were hopes for a gradual recovery. However, after that, the number of new infections spiked to more than twice the number of lockdown highs in April. As a result, the lifting of the restrictions has stalled and in some cases has been tightened again. All this promises to add uncertainty to the forecasts or their reduction.

The debt markets pay just as much attention to this event. In recent days there has been more talk of the Dollar losing its “exorbitant privilege”. Since the 1960s, this term has been used to describe the advantages for the U.S. dollar’s reserve currency status. This status has helped to place bonds at lower rates than those of competing economies for years and to meet the high demand and first-class liquidity consistently. It should not be forgotten that the yield of American government securities is higher than in many European countries as well as Japan. This is alarming because the states need to borrow trillions of dollars in the markets. It is in the Fed’s power to support bond prices, thereby reducing their yields and debt service costs.

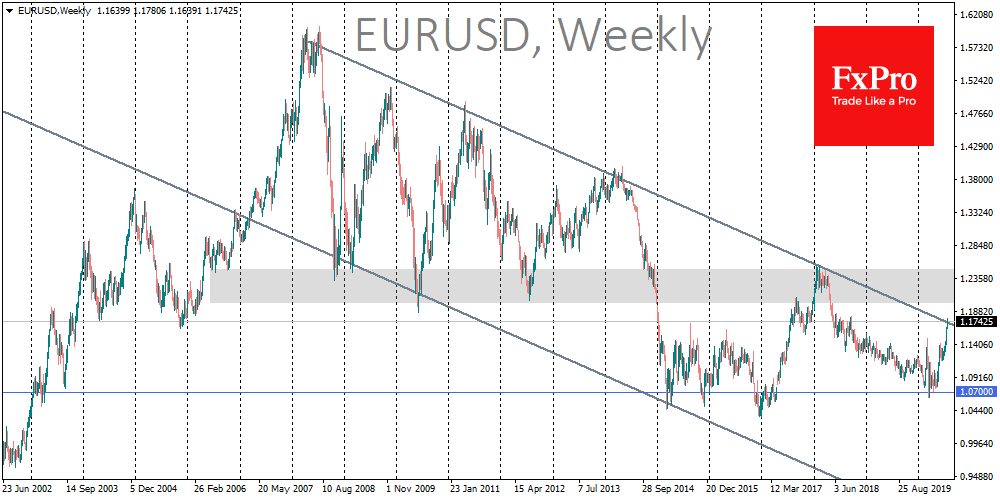

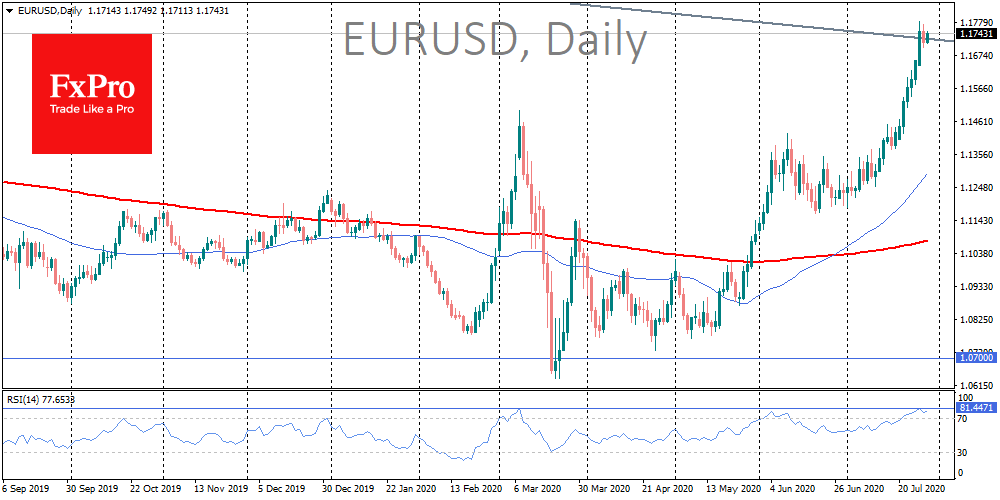

Perhaps the most interest still concerns the dynamics of the Dollar. Since the beginning of July, it has been showing an almost daily decline against its main competitors. On the long-term charts, EURUSD has been approaching the resistance level of the downtrend since 2011. Steady growth above the current levels (1.1750-1.1800) may become a signal of the start of a longer-term extension, as it was in the period from 2000 to 2008.

Without the Fed’s attention to the topic of the dollar weakening, the growth impulse of EURUSD may take it to 1.2000 in August and to 1.2500 by the end of the year. It is hard to take the discussion seriously that this is beneficial for American companies. After all, the USA is a net importer with a large trade deficit. A steady decline in the Dollar could quickly turn into pressure in the U.S. debt markets, which would put the Treasury in a challenging position.

If the Fed speaks about this, then Chairman Powell will try to convince the world of stability at the press conference. Combined with excessively overheated sales of the U.S. currency in the last few weeks, this could lead to a confident retracement of the Dollar to 1.1000. This scenario is seen as being the most likely, as it will allow the U.S. Treasury to buy time for new rounds of borrowing in debt markets.

It is unlikely for EURUSD to return to, or below 1.07 unless there is a repeat of March’s markets disaster when demand for the Dollar swept away everything in its path.

The FxPro Analyst Team

April 17, 2024 @ 17:10 +03:00

April 16, 2024 @ 17:37 +03:00

April 15, 2024 @ 16:30 +03:00

April 15, 2024 @ 13:53 +03:00