The Fed is keeping the dollar under pressure

March 18, 2026 @ 19:14 +03:00

- Concerns over the FOMC’s ‘dovish’ rhetoric are weakening the dollar.

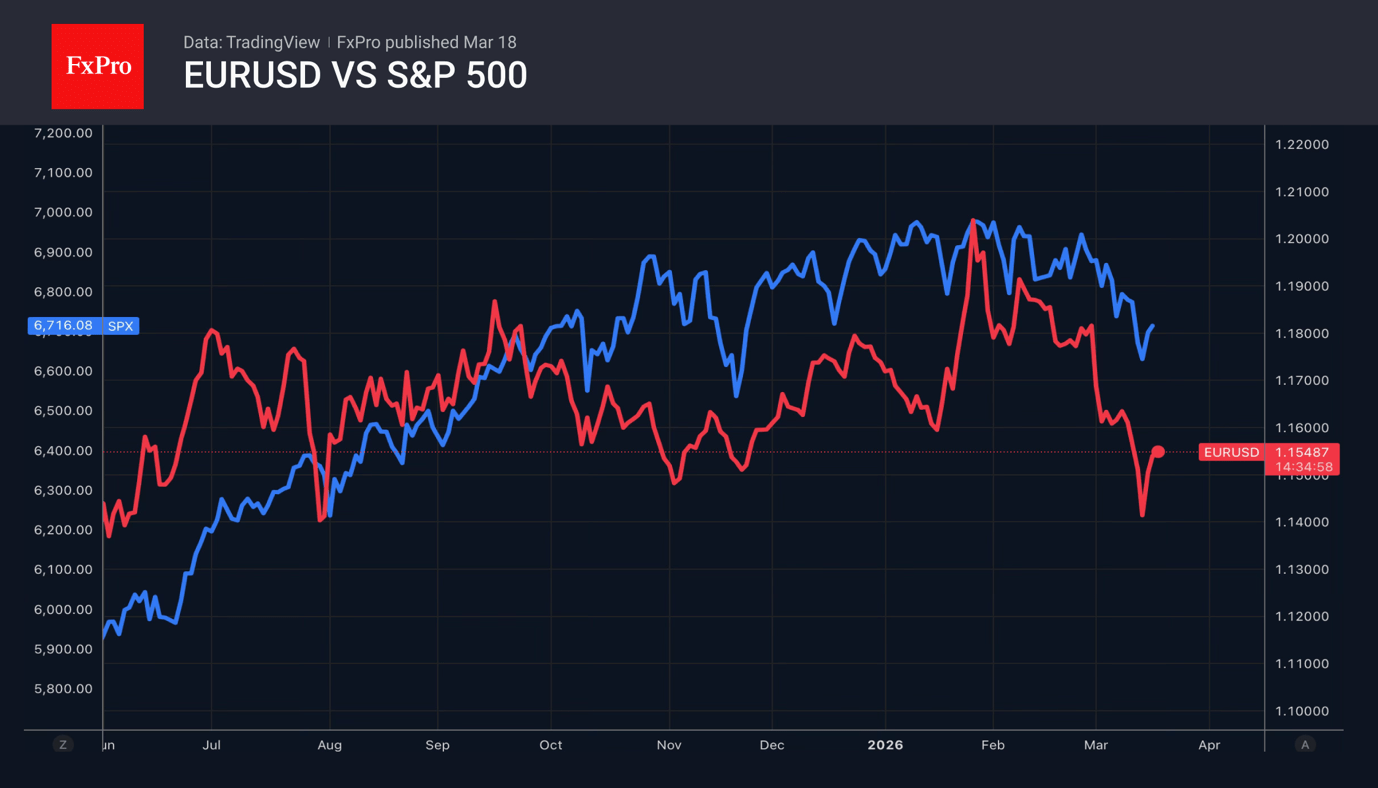

- US stock indices are providing support for the EURUSD.

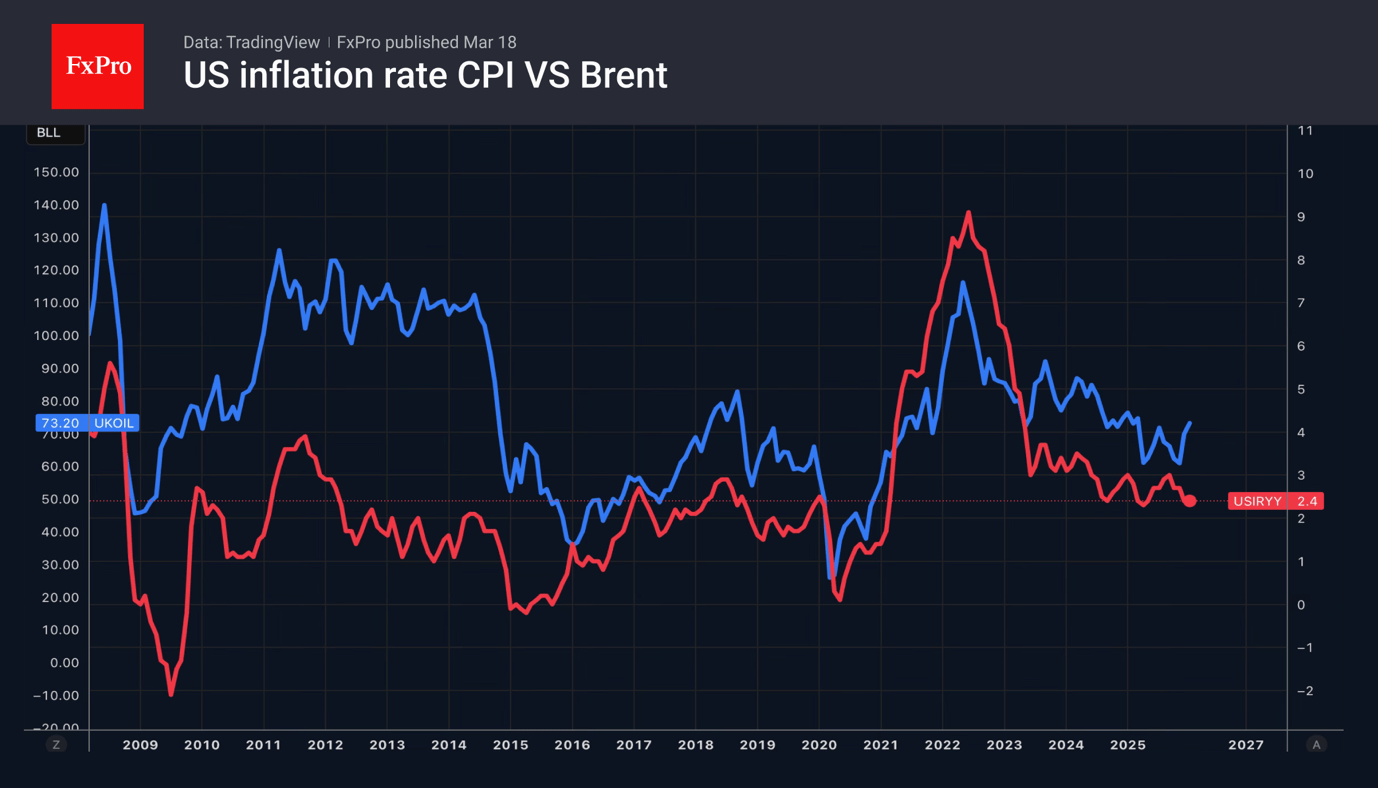

The US dollar is the only G10 currency that is both a safe-haven and an energy exporter, so it is unsurprising that the DXY has risen since the start of the Middle East conflict. Gas prices continue to rise, with Brent closing above the $100-per-barrel level, which was unthinkable at the start of the year, for the fourth day in a row. Some of the Fed’s tricks are working, but the S&P 500 rally is boosting risk appetite and forcing the EURUSD bears to retreat.

The stakes are clear. Brent crude risks soaring to $200 a barrel, which would cripple the global economy. The question is: how will central banks react? They usually view oil shocks as temporary phenomena and focus on core inflation. However, the ECB’s passivity in 2022 led to consumer prices rising into double figures. The European Central Bank has no intention of repeating that mistake.

FOMC is still divided. Stephen Miran, Christopher Waller and Michelle Bowman, all appointed by Donald Trump, are highly likely to vote in favour of cutting rates. They could feel more comfortable after the US President urged Jerome Powell to do so. As a result, the FOMC’s updated forecasts may turn out to be more ‘dovish’ than the futures market anticipates. Derivatives have abandoned the idea of two rate cuts in 2026. If the Fed signals that this remains on the table, the US dollar risks falling.

The euro felt support from an upbeat market mood amid rising indices over the past two days. NVIDIA expects to generate up to $1 trillion in revenue thanks to its Blackwell and Rubin chips, whilst OpenAI intends to set up a $10 billion joint venture with private investment firms. Investors’ belief that artificial intelligence will offset the negative impact of rising oil and petrol prices is pushing the S&P 500 and Nasdaq Composite higher.

Nevertheless, until the Strait of Hormuz reopens, fear in the US stock market is unlikely to give way to greed. A resumption of the stock indices’ rally will deprive the EURUSD of its key advantage. The ECB’s ‘hawkish’ rhetoric is unlikely to help the euro. Raising the deposit rate is a misguided decision since the eurozone economy is too weak to withstand monetary tightening.

The FxPro Analyst Team