Will the BoJ and the ECB join the Fed or show strategic prudence?

January 20, 2020 @ 12:54 +03:00

Monday is a day off in the American markets due to the Martin Luther King’s Day. Because of the holiday, trading on other markets also promises to be muted. However, the following week promises to be an eventful one, with decisions by major central banks, including the Bank of Japan, Bank of Canada and the ECB. The troika – Fed, ECB, and Bank of Japan – are the most influential global central banks, capable of significantly affecting trends in global markets as they did four years ago. Hence, it is worth paying more attention to their signals at the beginning of the year.

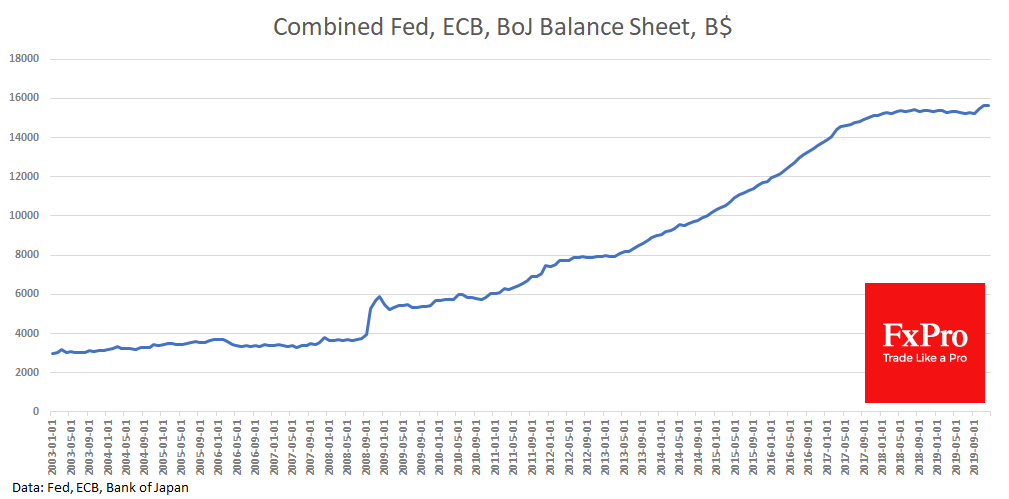

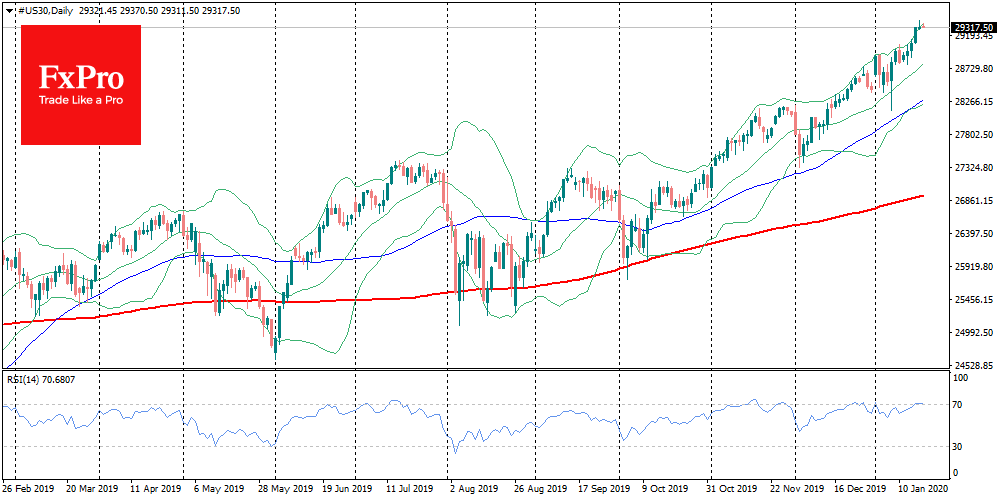

More and more observers point out that new highs by American indices on an almost daily basis linked with the interbank market liquidity pumping from the Fed. By early September, the Fed stopped letting its balance sheet shrink. It soon began to replenish it with short-term US government bonds to fill the repo market with liquidity, where at some point the rates jumped up to 10%, four times exceeding the target levels of the central bank.

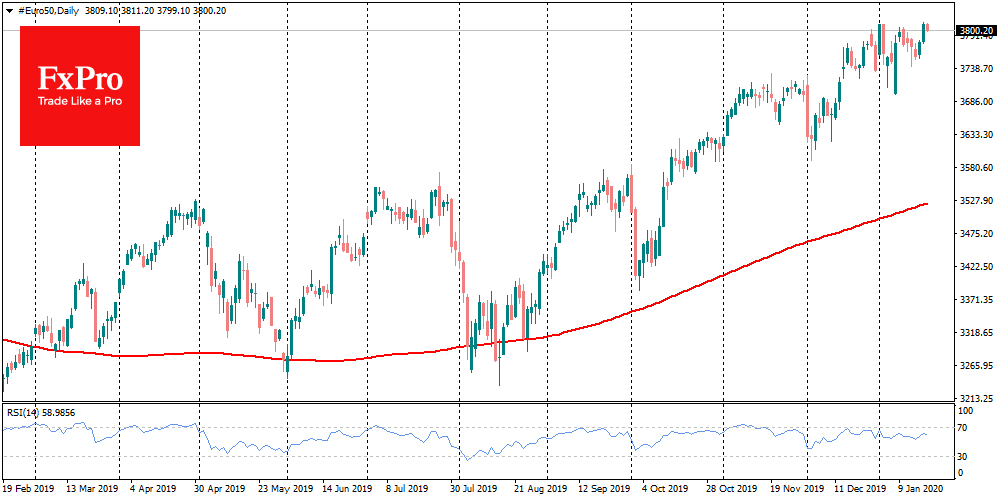

As soon as it became clear that the Fed’s emergency liquidity pumping measures in September, the US indices switched into a regime of the virtually unstoppable rally. The same can be said about the actions of the ECB, which in August announced the restoration of asset purchases on its balance sheet since November. Bank of Japan did not stop feeding the markets with liquidity. The total balance sheet of these three central banks is approaching $16 trillion, updating record highs. It can hardly be considered a coincidence the balance sheets growth of the largest central banks and the growth impulse in the markets.

However, the actions of the ECB and Bank of Japan look much more cautious than the Fed. Perhaps, this explains why American markets are much more active in updating their records. This week, the ECB promises a comprehensive monetary policy strategy review. If this revision brings the ECB closer to the Fed in terms of increasing aid to markets, it may refresh the growth of the eurozone stock markets. The same applies to the Bank of Japan, whose meeting will be held tomorrow morning.

If the ECB and Bank of Japan focus on the negative aspects of the existing movement in the stock markets, it may trigger a correction rollback and even become a defining feature of the full-year trends. The negative sides are widely known and often highlighted in the press. Buying government bonds on the central bank balance sheet is essentially government financing, which devalues the currency. Also, pumping markets with liquidity contributes to debt accumulation. At some point, they will have to pay for it. However, if central banks intend to soften the policy further, this moment of reckoning may be somewhat distant, but as a result more destructive.

The FxPro Analyst Team