Weekly review: Dollar in retreat, stocks in rally, gold is rising

May 08, 2026 @ 08:44 +03:00

US Dollar

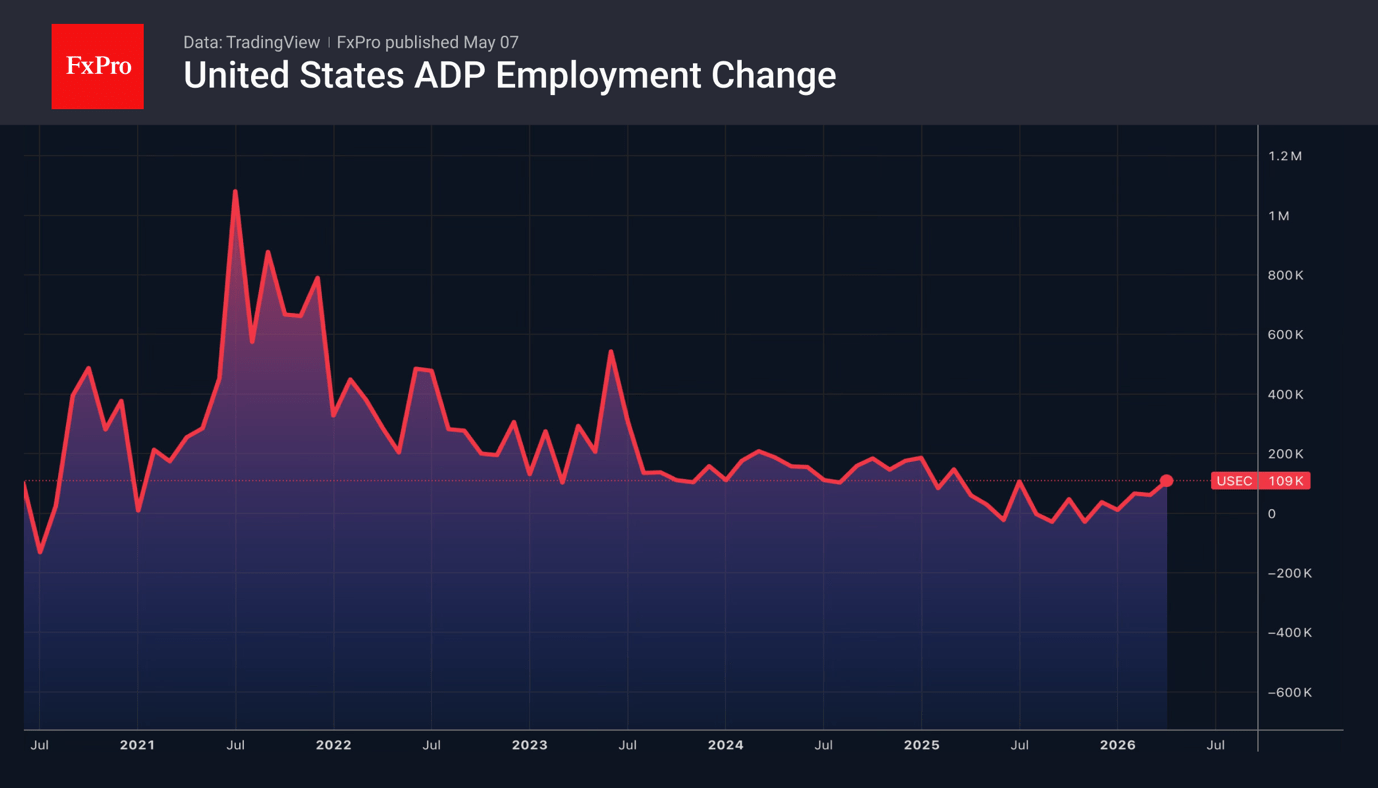

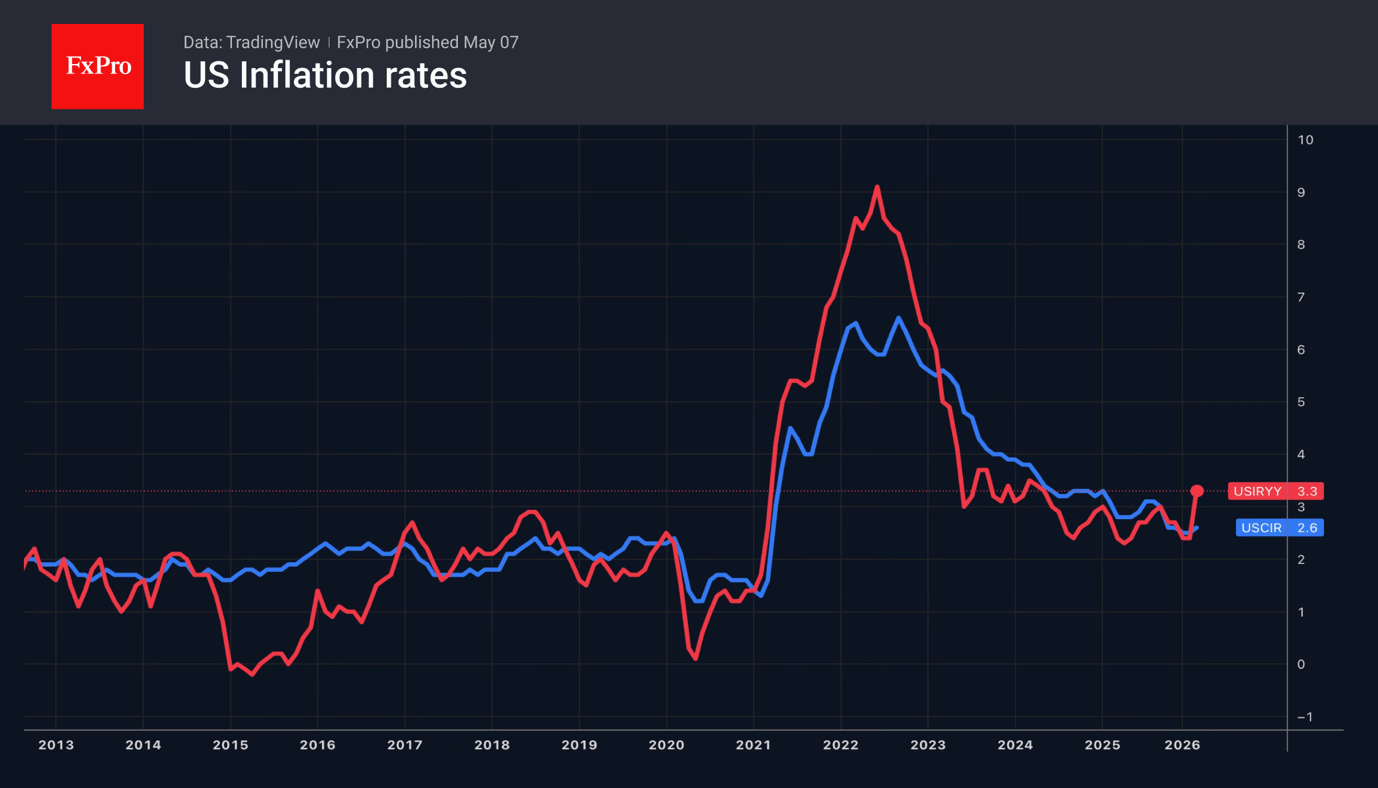

The US dollar bounced back from sellers amid doubts about a swift resolution to the Middle East conflict and positive US economic data. ADP reported a 109K increase in private sector employment in April, the best performance since the start of 2025. The stabilisation of the labour market against a backdrop of accelerating inflation allowed the DXY to rebound by 0.5% from the day’s lows, recouping half of its losses since the start of the day on Wednesday. However, this was short-lived.

The US and Iran are working to resume talks by May 15th. Markets react first and ask questions later. Consequently, rumours of a de-escalation of the conflict in the Middle East initially pushed the EURUSD to its highest since February, near 1.1800. However, subsequent doubts caused the pair to retreat.

Geopolitics will cause more pain for Europe than for the US. Even more so, as Donald Trump threatens to raise tariffs on European cars from 15% to 25%. The economic slowdown, coupled with rising inflation after the energy spike, is creating stagflationary risks, forcing the ECB to tread carefully. Even if rates are raised, it is unlikely to be by much. The differential will remain in favour of the Americans, limiting the upside potential of EURUSD.

Stock indices

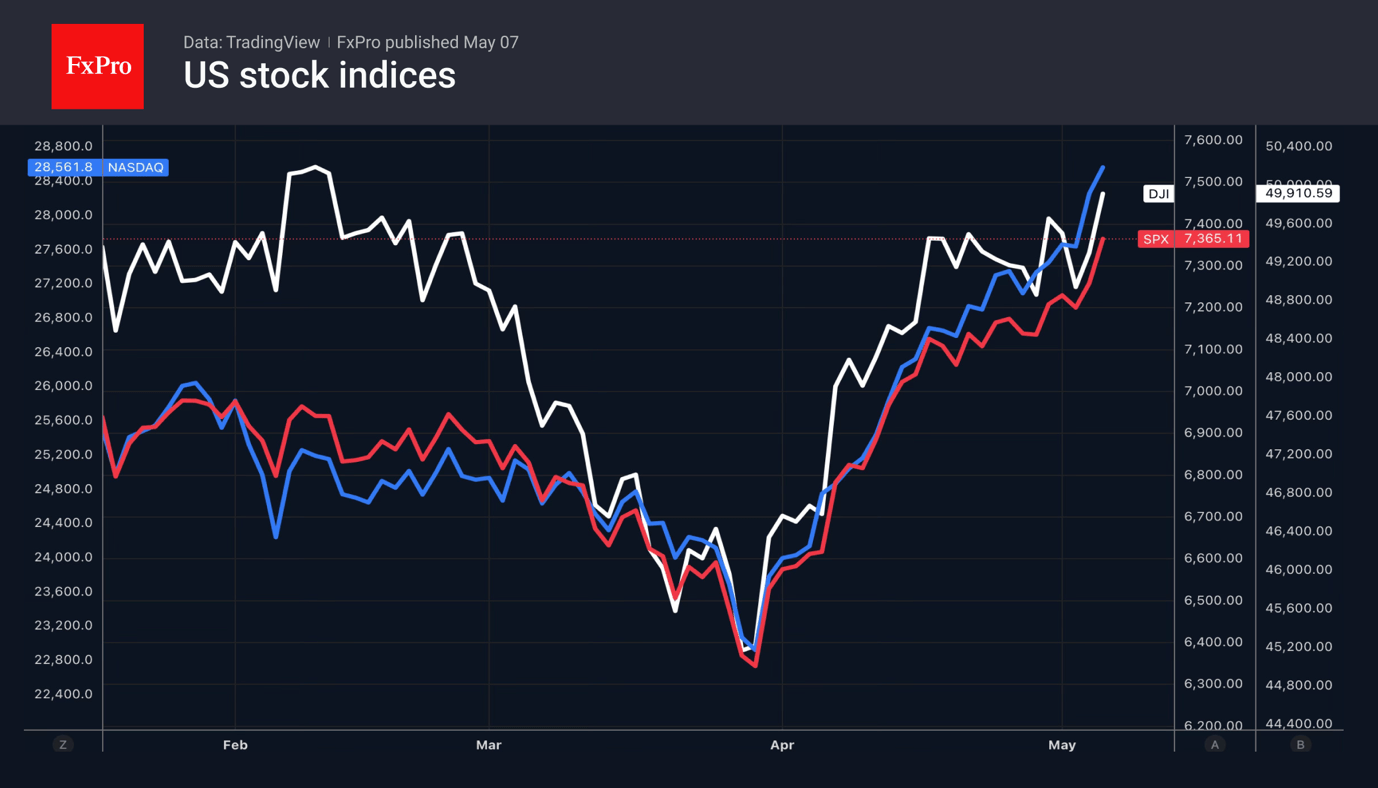

The S&P 500 continues to hit record highs thanks to upbeat corporate earnings, attractive valuations, the US economy’s strength, confidence in the de-escalation of the Middle East, and fiscal stimulus.

Thanks to Donald Trump’s One Big Beautiful Bill Act, Americans will pay $63 billion less in taxes in 2026 than in 2025, while the total amount of tax deductions will increase by $47 billion. This creates a kind of safety net for both the economy and the stock indices.

Around 80% of S&P 500 companies that have already reported their first-quarter results have exceeded earnings estimates. Morgan Stanley notes that issuers delivered a 6% positive earnings-per-share surprise, the best result in four years. In 2022, following the launch of ChatGPT, there was great excitement about the potential revenue from artificial intelligence technologies. Those expectations are now being realised.

Gold

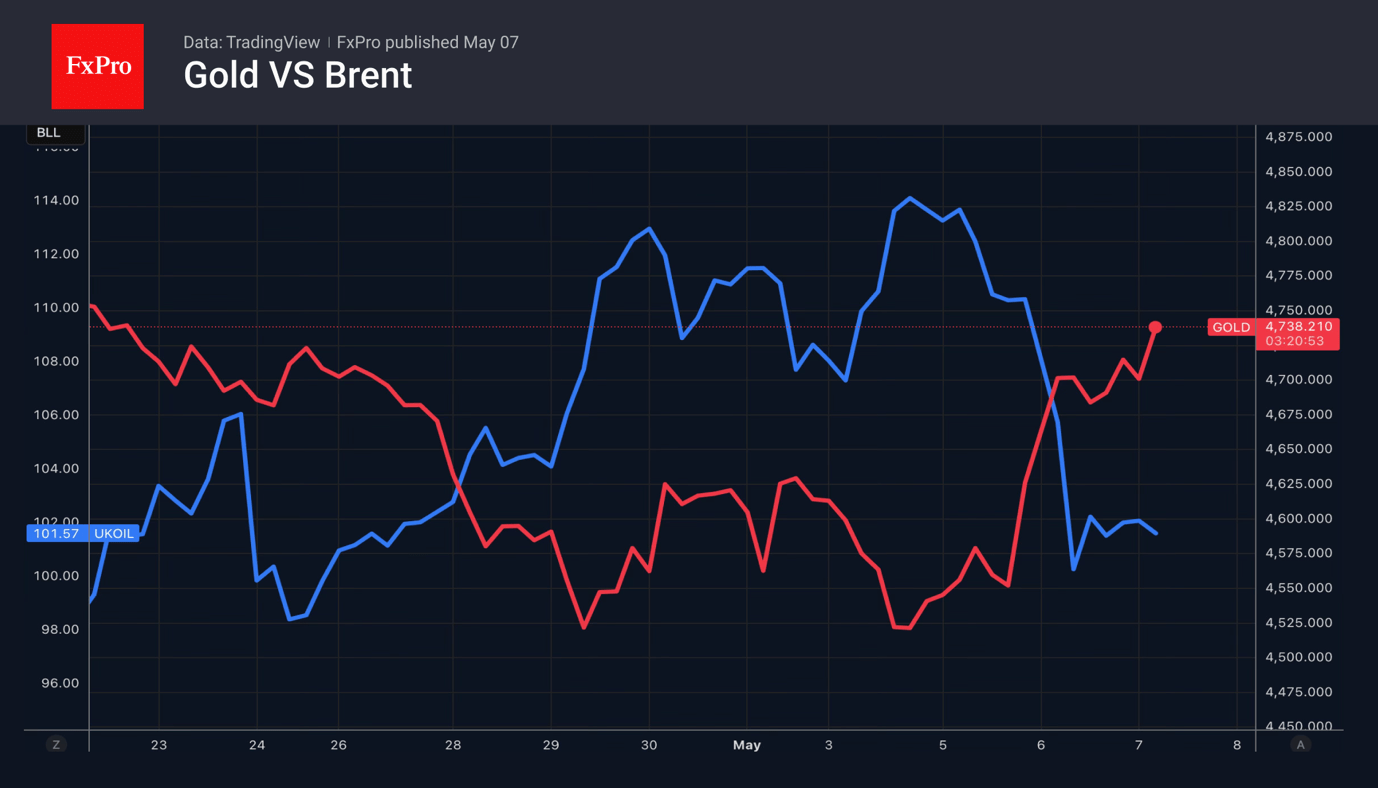

On Wednesday, rumours of a de-escalation in the Middle East helped gold post its best one-day performance since late March. The precious metal is reacting sensitively to the market’s reduced inflation expectations following the fall in oil prices. This makes a Fed rate hike in 2026 inadvisable.

Gold is unfazed by the fact that, according to World Gold Council data, central banks became net sellers in March. Turkey was the most active, with 60 tonnes. Azerbaijan’s reserves fell by 22 tonnes, and Russia’s by 16 tonnes. Regulators sold it on fears that the Middle East conflict would deal a blow to their economies. However, with the de-escalation of geopolitical tensions, central banks could resume net buying.

Also, without major central banks’ monetary tightening, we could see a revival of the debasement trade, which could support the commodity.

Crypto

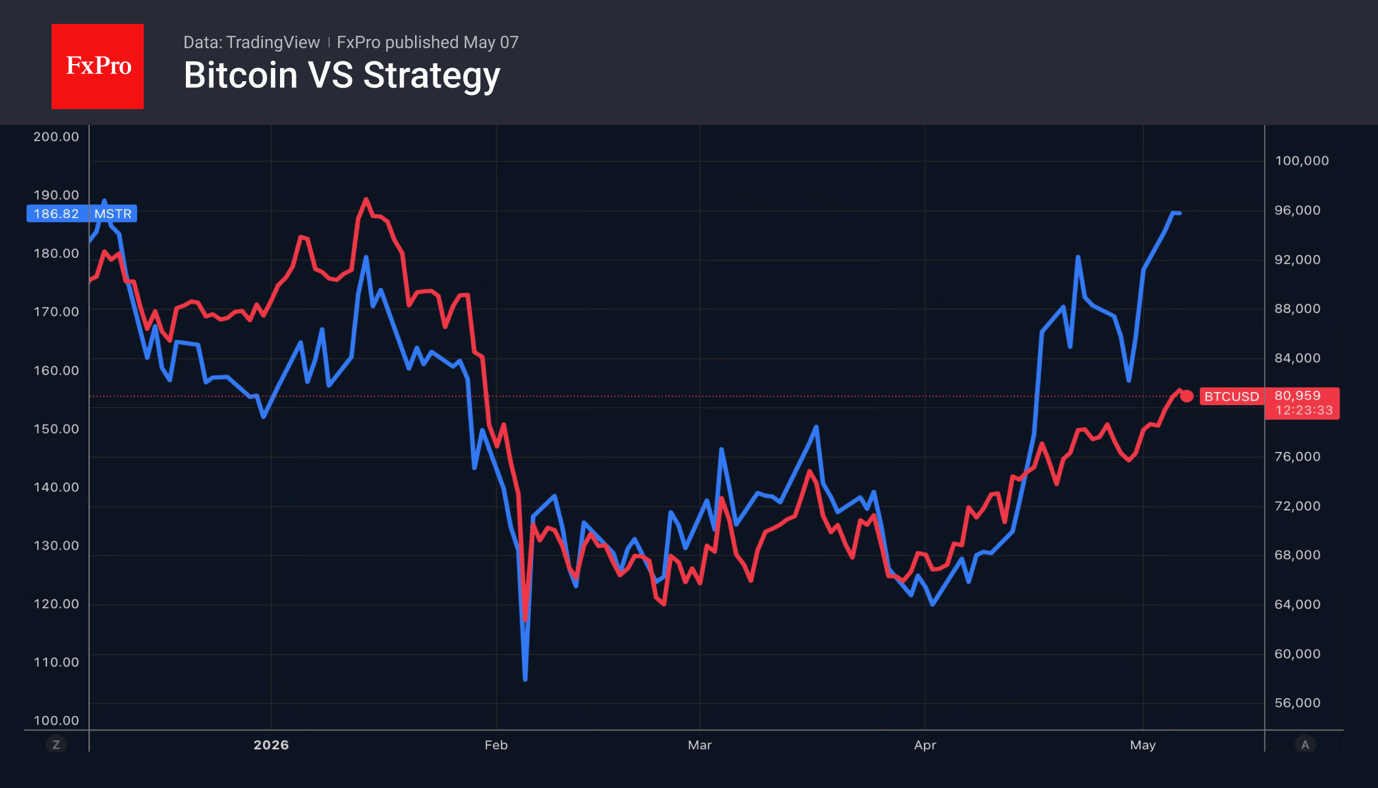

Bitcoin outperformed stock indices and gold at the onset of the armed conflict in the Middle East. However, the de-escalation of geopolitical tensions has revived the lag in cryptocurrency. The S&P 500 and gold are rising faster, prompting discussion about the status of the digital asset. Is it a risky investment or a safe haven?

Investor sentiment is shifting. Almost unbelievably, the Strategy company, which had promised never to sell Bitcoin, is now discussing the circumstances under which it would sell its reserves to pay dividends. The company reported a first-quarter loss of $12.5 billion and claims that the need to improve its capital structure or increase the ‘bitcoin per share’ ratio could be grounds for reducing its token reserves.

Investors have taken Michael Saylor’s company’s losses in stride, as Bitcoin trades above 80,000. In February, the slump in BTC led to a 50% loss in Strategy’s market capitalisation.

What next?

Investors’ attention will remain focused on the Middle East. Until the conflict is resolved, geopolitics and oil prices will continue to drive asset prices in financial markets. Negotiations between the US and Iran, as well as the meeting between Donald Trump and Xi Jinping, are the key events of the second full week of May. Progress in the peace process will boost risk appetite, support risky assets and accelerate the sell-off of the US dollar as a safe-haven asset.

Traders will be keen to see how the US President’s threats to raise tariffs on European cars from 15% to 25% play out. Will the EU swallow the bitter pill, or are the markets facing a new trade war?

On the economic calendar, the focus is on US inflation and retail sales, as well as leading indicators for the eurozone and Germany, and UK GDP figures. The further acceleration in US consumer prices could shift the Fed’s outlook, strengthening the hawks’ position. The futures market will increase the likelihood of the Fed tightening monetary policy, offsetting the negative impact on the US dollar from the de-escalation of the Middle East conflict.

The FxPro Analyst Team