US President Trump tells UK PM May “No Hard Brexit, No Trade Deal”

July 13, 2018 @ 09:52 +03:00

President Trump has spent yesterday in Europe where he attended a NATO meeting before travelling to the UK. He left Brussels with the commitment of NATO members to meet their agreed 2% spending target. Reports from the meeting suggested that he threatened to pull the US out of NATO if this wasn’t agreed which led to a kneejerk selloff in markets at around 08:55 GMT yesterday.

He conducted an interview with the Sun newspaper in the UK where he is reported to have said that May’s plan for a softer Brexit “will probably kill” any future trade seal with the US. He said that PM May ignored his advice for a hard Brexit and that Boris Johnson would make a great PM. GBPUSD has sold off since the comments were reported, falling to a low of 1.31641. The Brexit White Paper released yesterday created little movement in markets. Next week will be important for GBP with economic data being released which will impact the BOE August rate decision, a key driver of direction in the currency.

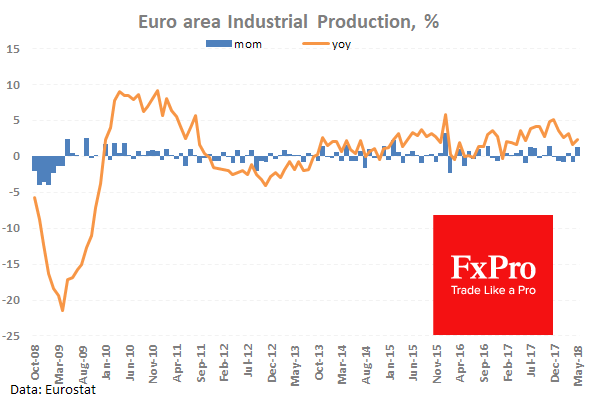

Eurozone Industrial Production w.d.a. (May) was released with the numbers coming in as 1.3% (MoM) and 2.4% (YoY) against the consensus of 1.2% (MoM) and 2.1% (YoY) from a prior reading of -0.9% (MoM) and 1.7% (YoY) with the previous (MoM) reading revised up to -0.8%. This data was expected to increase today and did not disappoint with the monthly figure moving back into positive territory after falling under zero last month. The expected rise in the data is positive after months of sluggish economic data coming out of the Eurozone. EURUSD moved higher from 1.16728 up to 1.16891 where it consolidated for a period of time.

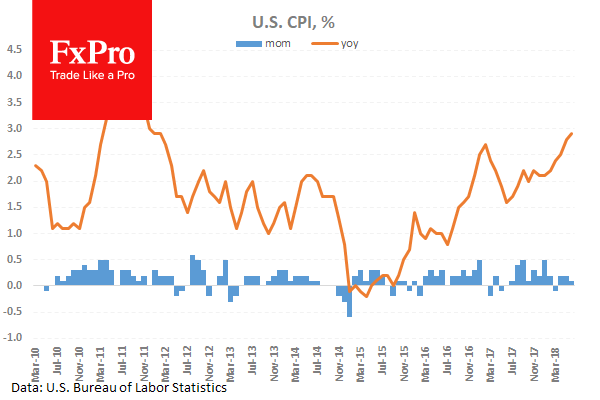

US Consumer Price Index (Jun) data was released coming in at 0.1% (MoM) and 2.9% (YoY) with an expected reading of 0.2% (MoM) and 2.9% (YoY) from 0.2% (MoM) and 2.8% (YoY) previously. Consumer Price Index Ex Food & Energy (Jun) data was released with a reading of 0.2% (MoM) and 2.3% (YoY) against an expected reading of 0.2% (MoM) and 2.3% (YoY) from 0.2% (MoM) and 2.2% (YoY) previously. Consumer Price Index Core s.a. (Jun) data was released with a reading of 257.310 against an expected reading of 257.361 from 256.889 previously. These data points allow for an updated measure of the effect of inflation on consumers. Inflation is one of the main drivers of market sentiment in the US currently. Consumer prices remained generally in line with forecasts.

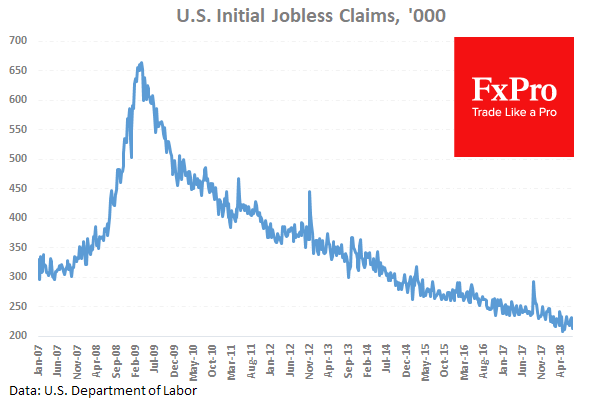

US Initial Jobless Claims (Jul 2) were 214K against an expected 225K from 231K previously which was revised up to 232K. Continuing Jobless Claims (Jun 25) were 1.739M against an expected 1.720M from a prior 1.739M which was revised up to 1.742M. This data shows a drop in continuing claims with a small drop in the number of initial claims expected. GBPUSD moved higher from 1.32019 to a daily high of 1.32445 in reaction to the numbers released.

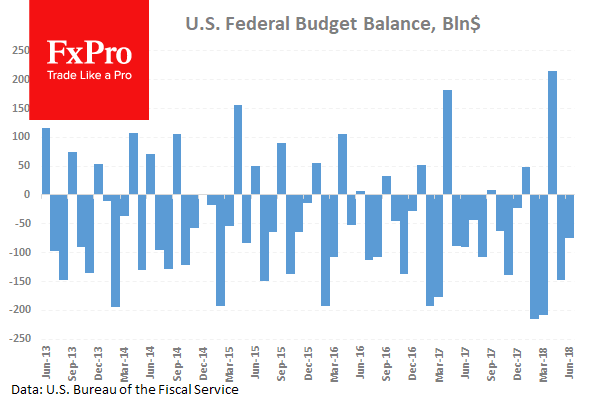

The US Monthly Budget Statement (Jun) was released with a number of $-75.0B against an expected balance of $-98.2B from a previous $-147.0B. This data has remained firmly in negative territory as seasonal factors affect the calculation of this metric. The previous reading dropped from the high in April 2018 of $182.4B. USDJPY moved higher from 112.411 to 112.534 after this data release.

EURUSD is down -0.07% overnight, trading around 1.16621. USDJPY is up 0.04% in the early session, trading at around 112.575 GBPUSD is down -0.20% this morning trading around 1.31776 Gold is down -0.12% in early morning trading at around $1,245.82 WTI is down -0.204% this morning, trading around $69.54