US inflation will put everything into perspective

May 12, 2026 @ 14:15 +03:00

- An acceleration in the US CPI will support the US dollar.

- Currency interventions have provided temporary relief for the yen.

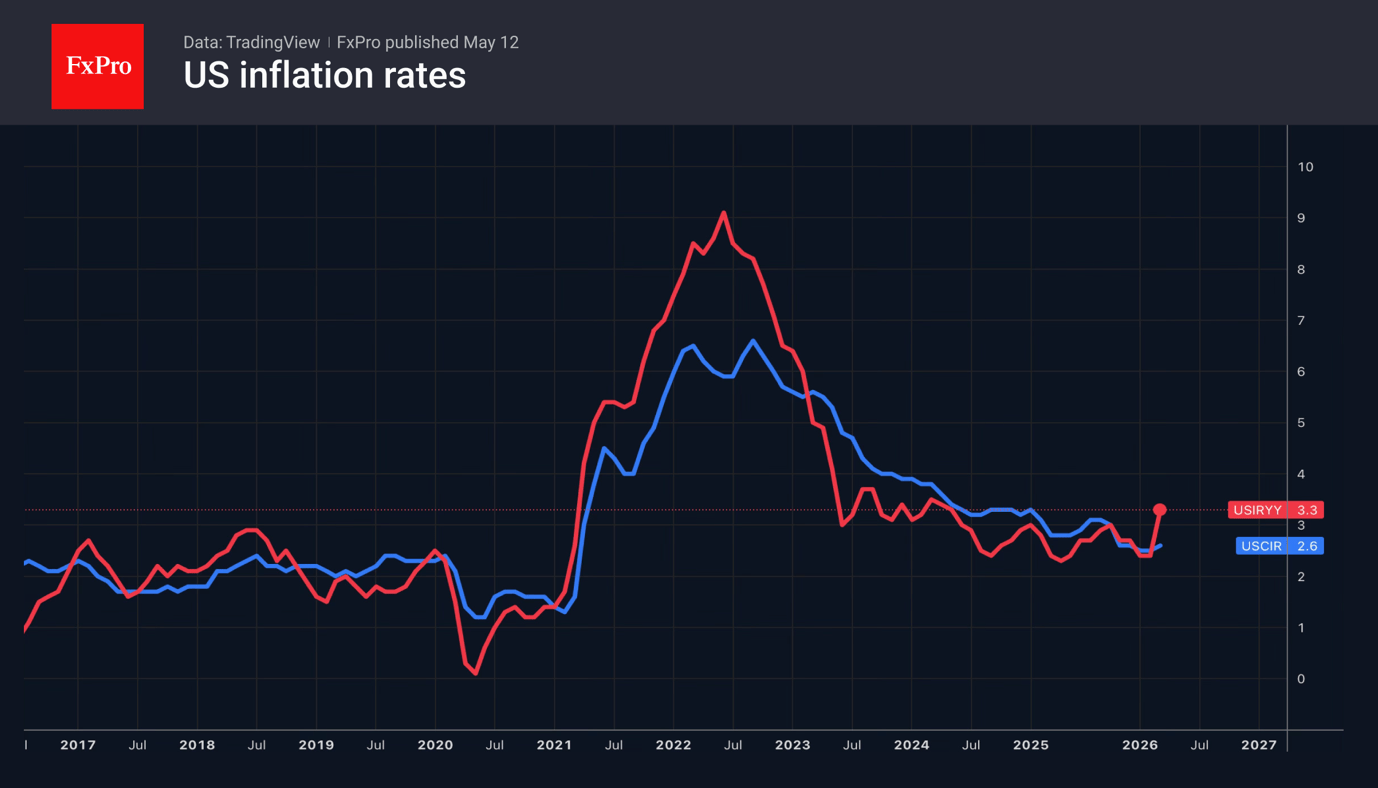

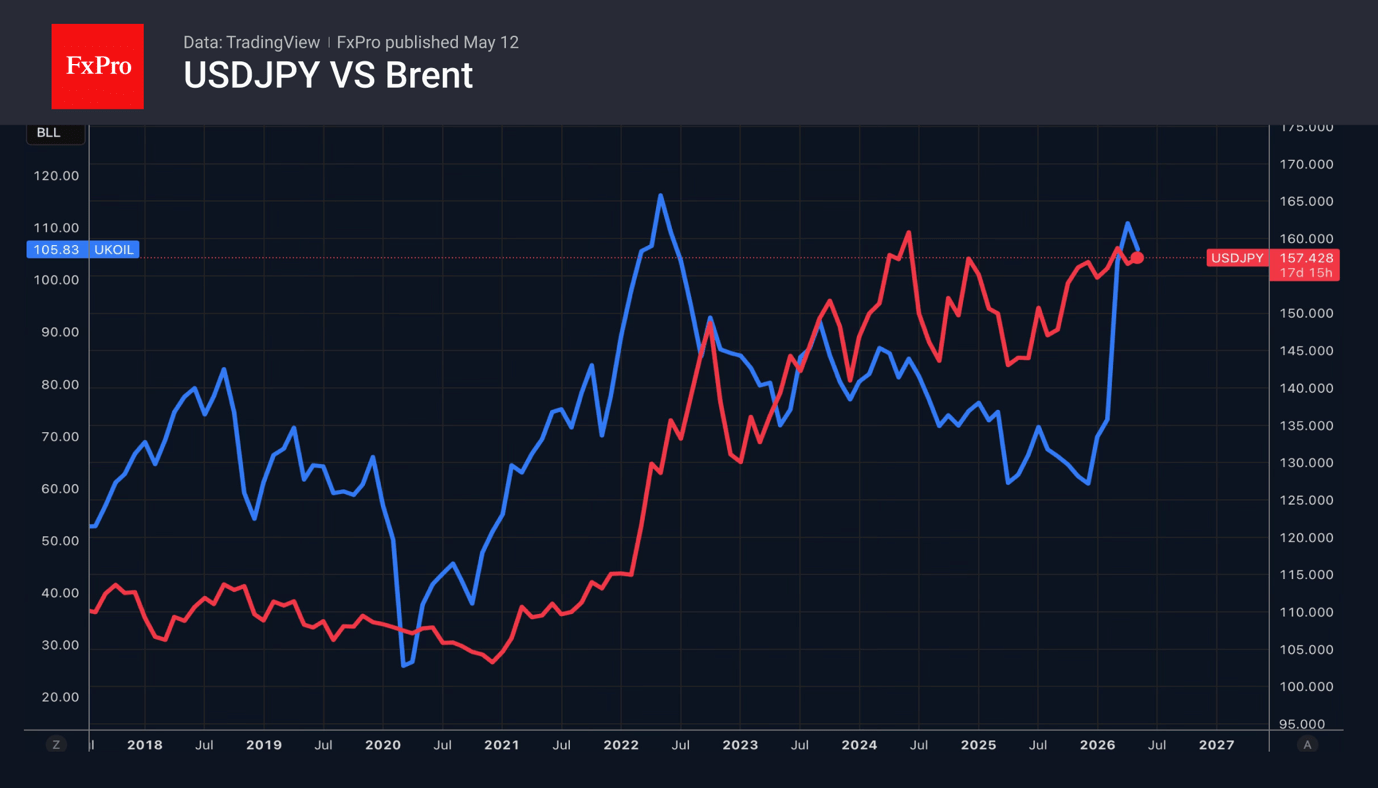

The US dollar has been stuck within a 0.4% range over the past week, amid a stalemate in the Middle East. NACHO or ‘Not a chance Hormuz Opens’ has replaced TACO. Investors are coming to terms with the idea that the blockade of the main oil artery is here to stay. Under such conditions, the chances of a rise in Brent and a strengthening of the USD are increasing, especially as the latter is fuelling expectations of a new batch of US inflation data.

Growing expectations of a key rate hike are supporting the euro. Economists surveyed by Bloomberg expect two rate hikes this year, from 2% to 2.5%, compared to just one in the previous similar survey. Economists expect inflation in the eurozone to accelerate to 2.9% by the end of the year.

CME derivatives suggest the federal funds rate will remain unchanged in 2026 and rise to 4% with a 50-50 probability by April 2027. The timing of monetary policy tightening could be brought forward if inflation accelerates in April, which could put pressure on EURUSD.

According to Bank of America, the data does not justify the Fed resuming its cycle of monetary easing this year. Core inflation is too high, and the strong April jobs report has put an end to the idea of rate cuts. The bank has pushed back its forecast for monetary policy easing from September 2026 to July 2027.

Meanwhile, the USDJPY bulls are regaining their footing. The scale of currency interventions is estimated at ¥8.65–10.08 trillion, comparable to the ¥9.74 trillion recorded in 2024. These interventions have led to a reduction in speculative yen shorts to monthly lows. Nevertheless, given the upward trend in Brent and strong demand for the US dollar as a safe-haven currency, Japan’s funds may not be sufficient to deter hedge funds and asset managers.

The minutes of the latest Governing Board meeting may have supported the yen. One of its members stated that an overnight rate hike could be on the cards, even if the situation in the Middle East remains unclear. The futures market is pricing in a 72% probability of monetary tightening in June. However, the Bank of Japan has repeatedly pushed back the timing of expected monetary tightening, and the wide interest rate differential favours USDJPY.

The FxPro Analyst Team