The economy let the euro down

May 22, 2026 @ 14:42 +03:00

- Business activity in the eurozone is lower.

- The risk of further Japanese interventions has increased.

The dollar swung 0.4% intraday after a surge in the probability of a Fed rate hike to 60%, which subsequently fell back below 50%. By the end of the day on Thursday, Treasury yields had fallen, and US stock indices had risen. However, the medium-term outlook for the dollar remains bullish.

Iran’s firm intention to maintain its uranium reserves and continue to control the Strait of Hormuz runs counter to US plans. Donald Trump has vowed not to let Tehran do so. The gulf between the adversaries remains, heightening the risks of a prolonged closure of the world’s main oil artery. According to Rapidan Energy, the blockade will end in July and push Brent to $130 per barrel.

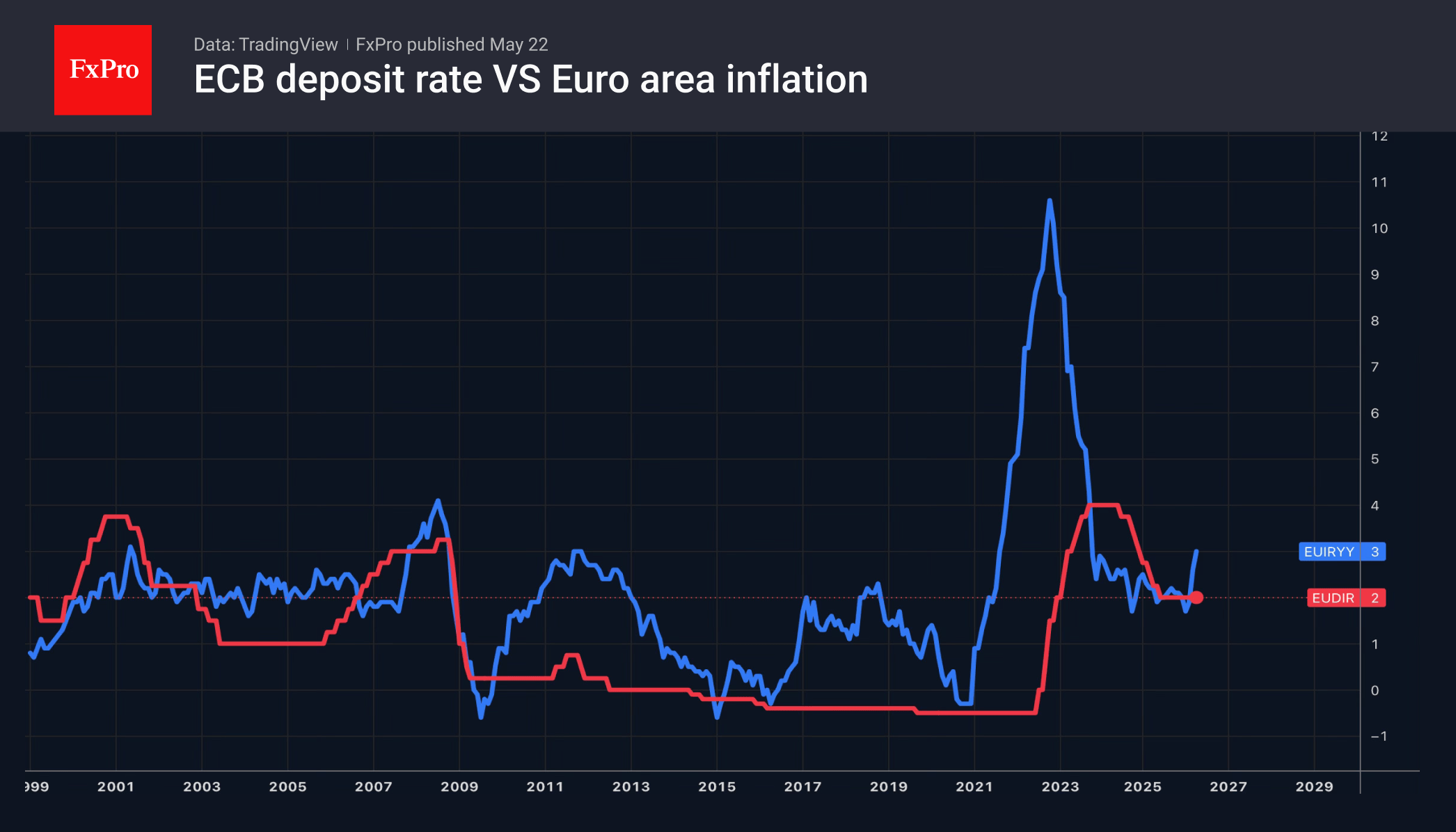

This poses a threat to oil-importing countries. The eurozone economy has already felt the impact. In May, the composite business activity index fell to its lowest level since October 2023. The European Commission has lowered its forecast for eurozone GDP growth from 1.2% to 0.9% and sharply raised its inflation estimate from 1.9% to 3% in 2026.

The worsening economic outlook will make it difficult for the ECB to tighten monetary policy. The futures market, anticipating 2–3 rate hikes this year, appears overly optimistic. The lower expectations fall, the worse it is for the euro.

The picture in the US is different. Business activity in the manufacturing sector has reached a four-year high, whilst Citi’s Economic Surprise Index has risen to its highest level since February. Macroeconomic data is encouraging, and the divergence in economic growth with the eurozone confirms the downward trend in EURUSD.

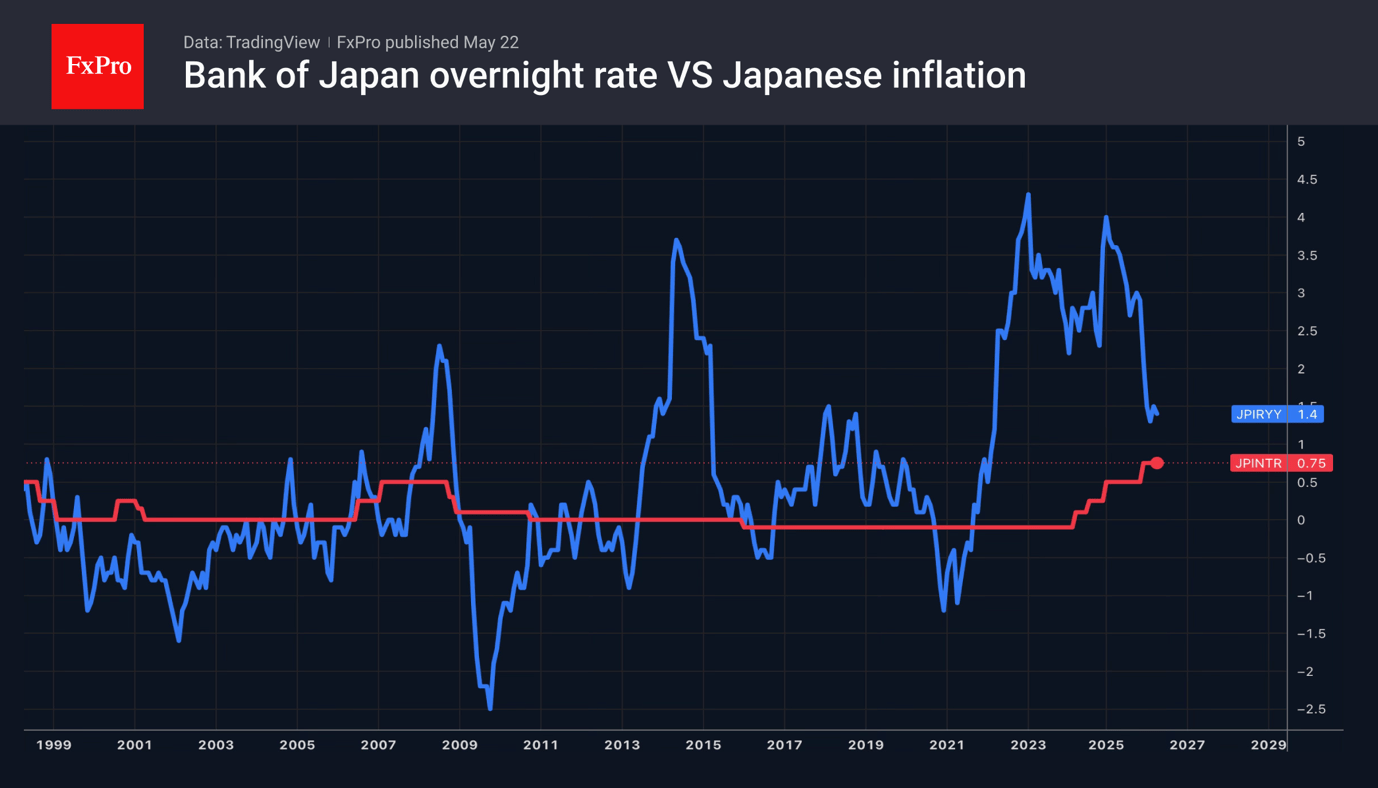

The approach of the holidays is forcing the USDJPY bulls to hit the brakes. The story of currency interventions is still fresh in memory, with Japan estimated to have spent around ¥10 trillion to support the yen. Reduced liquidity increases the risks of further interventions.

Moreover, it is difficult to rely on the bears’ other trump card on USDJPY, namely a rate hike by the Bank of Japan. In April, the consumer price index slowed to 1.4%, the lowest level in four years. This reduces the likelihood of an overnight rate hike in June.