The dollar has retreated in the face of Trump

March 24, 2026 @ 12:44 +03:00

- Rumours of US-Iran talks have sent the EURUSD up 1.2%.

- Oil is unlikely to return to pre-war levels.

The markets risk repeating past mistakes. Barely ten days into the conflict in the Middle East, Donald Trump began talking about negotiations with Iran. At that point, US stock indices rose, the dollar weakened, and oil prices fell. Two weeks later, history repeated itself. We heard the same talk from the president about dialogue with Tehran, just as the markets were plummeting and oil was beginning an uncontrolled surge. It seems that Brent’s and EURUSD’s previous experiences have taught them nothing.

For Donald Trump, the opening of the Strait of Hormuz, a fall in oil prices, and the return to the markets of the idea of a cut in the federal funds rate are of the utmost importance. So far, this view is supported only by Governor Stephen Miran, appointed by the President to the FOMC. In his words, the central bank must not be swayed by short-term headlines. Yes, inflation risks have risen, but so have the risks of a cooling labour market.

By contrast, Ostin Goolsbee, President of the Federal Reserve Bank of Chicago, has not ruled out either a resumption of the monetary easing cycle or a rise in interest rates. The latter aligns with the expectations of the derivatives market. Derivatives markets anticipate one round of monetary tightening from the Bank of England and two from the ECB. The outperformance of British and German bonds over their US counterparts is driving gains in GBPUSD and EURUSD. The rally in the euro and the pound against the US dollar is being fuelled by an improvement in global risk appetite following Trump’s speeches.

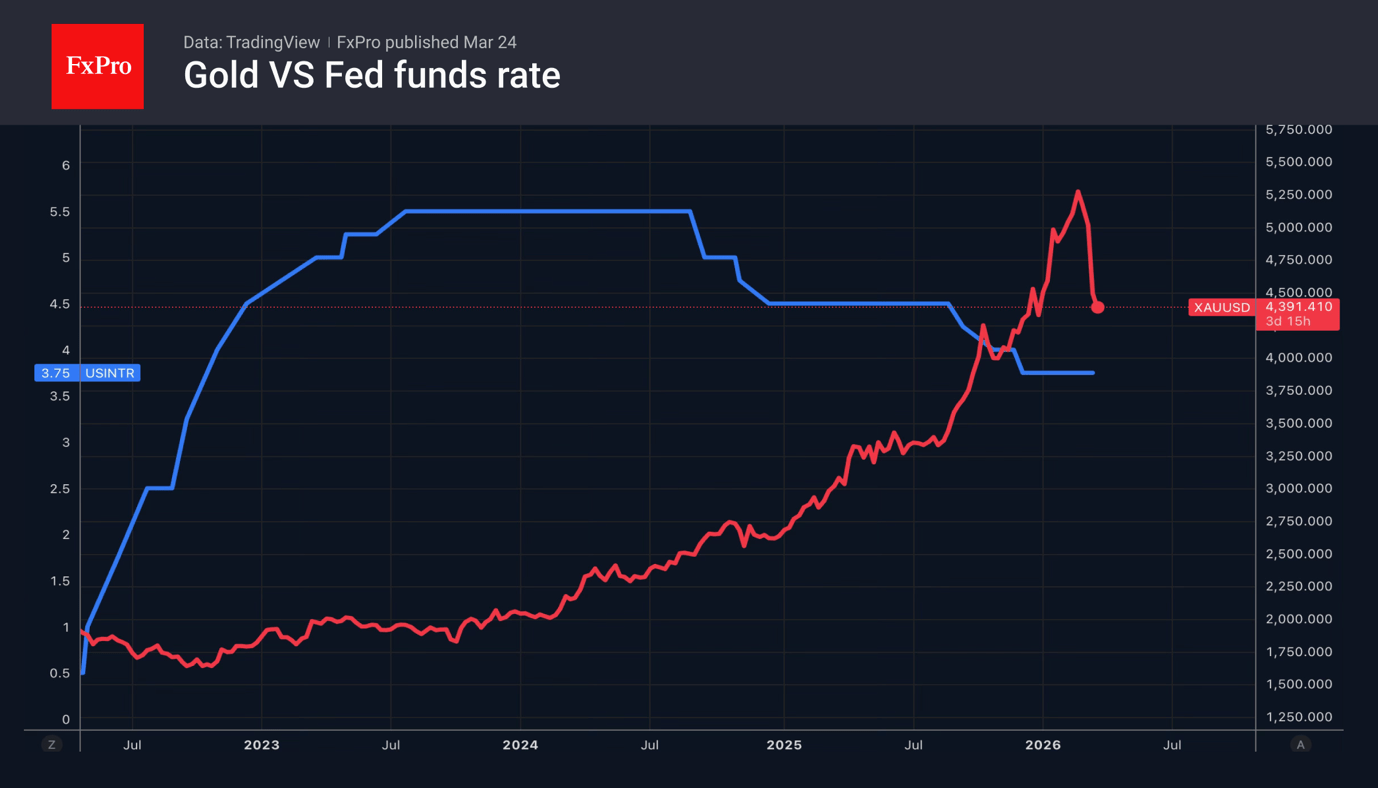

Meanwhile, gold has briefly dipped below $4,100 per ounce. High interest rates and the associated strengthening of fiat currencies are depriving the precious metal of its key trump card – debasement trading. Until signs of a US recession appear on the horizon and the Fed begins to discuss large-scale monetary stimulus, gold is likely to remain under pressure.

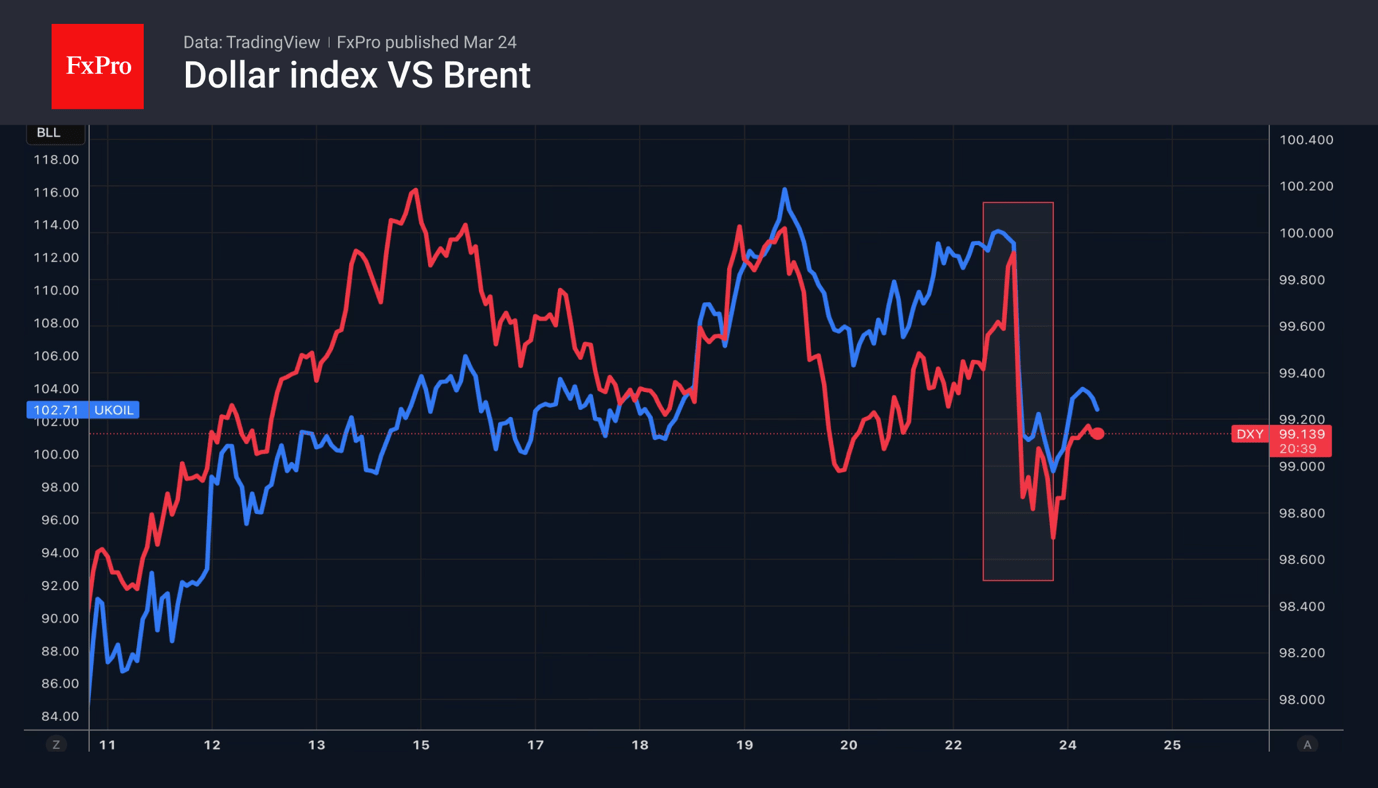

The situation is different with oil, and reopening the Strait of Hormuz is unlikely to help. According to Societe Generale and ANZ Research, Brent is unlikely to return quickly to levels of $65–70 per barrel. The main reason cited is a reduction in output by Gulf producers. In other words, the market has moved from a record surplus to a balanced state. Therefore, Brent crude is likely to remain above $85–90, giving the US dollar an advantage as the currency of a net energy exporter.

The FxPro Analyst Team