The dollar: geopolitics back in the picture

June 29, 2026 @ 10:37 +03:00

• The escalation of the conflict in the Middle East will bolster the greenback as a safe-haven asset.

• Data on European inflation and the US labour market will determine the fate of EURUSD.

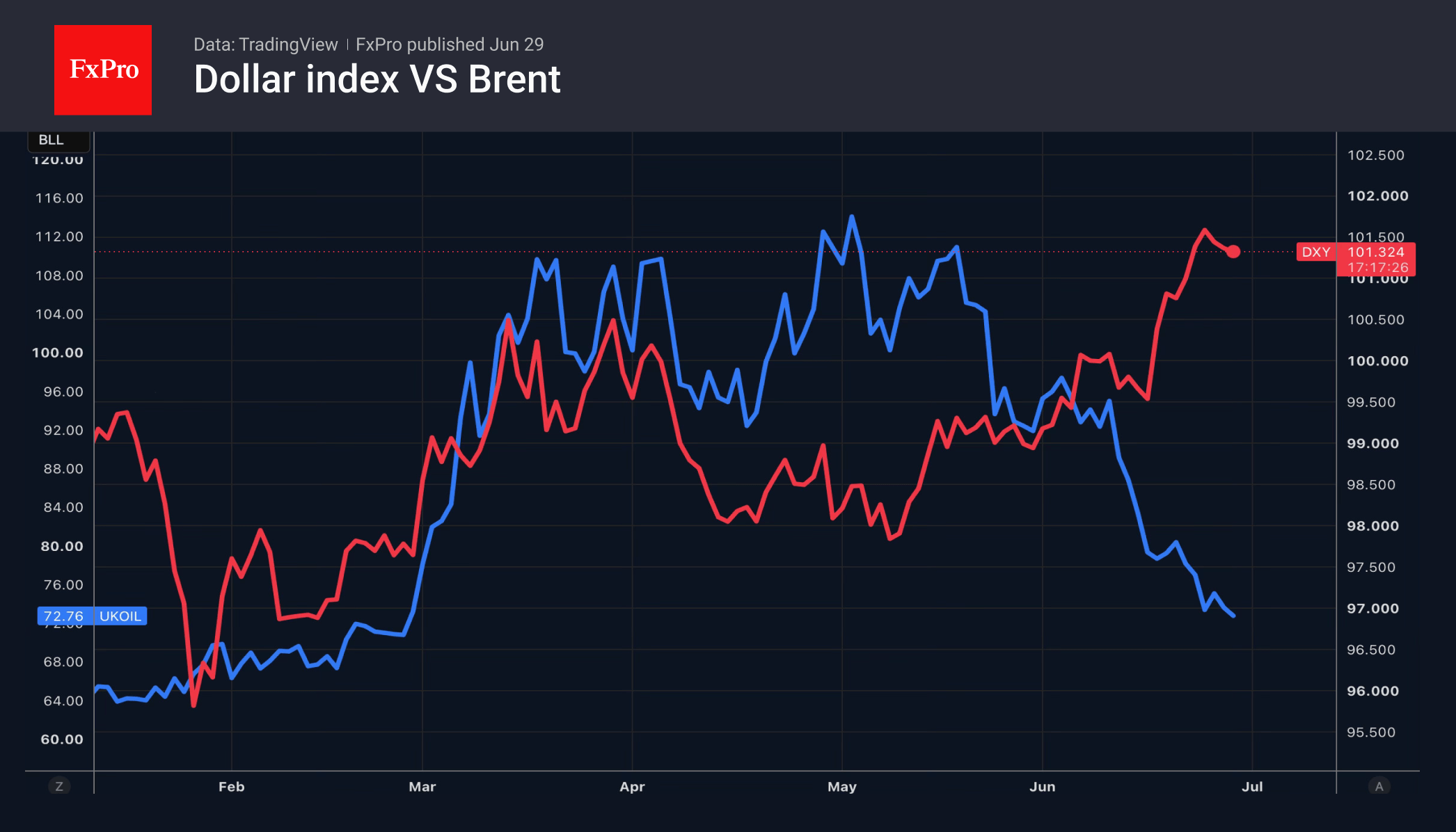

The US dollar quickly recouped its losses after the US resumed bombing Iran in response to its attack on tankers in the Strait of Hormuz. Prior to this, the greenback had been falling amid profit-taking on long positions due to reduced expectations of aggressive monetary tightening by the Fed. The rise in the University of Michigan’s Consumer Sentiment Index in June, coupled with a slowdown in long-term inflation expectations, suggests that two Fed rate rises in 2026 may be avoided.

According to Morgan Stanley, EURUSD could easily reach 1.1, as long-term investors are gradually unwinding their long positions whilst hedge funds are building up short positions. BNY Mellon sees potential for a fall below this level, as the ECB is unlikely to raise rates further due to the negative impact of monetary tightening on the eurozone economy.

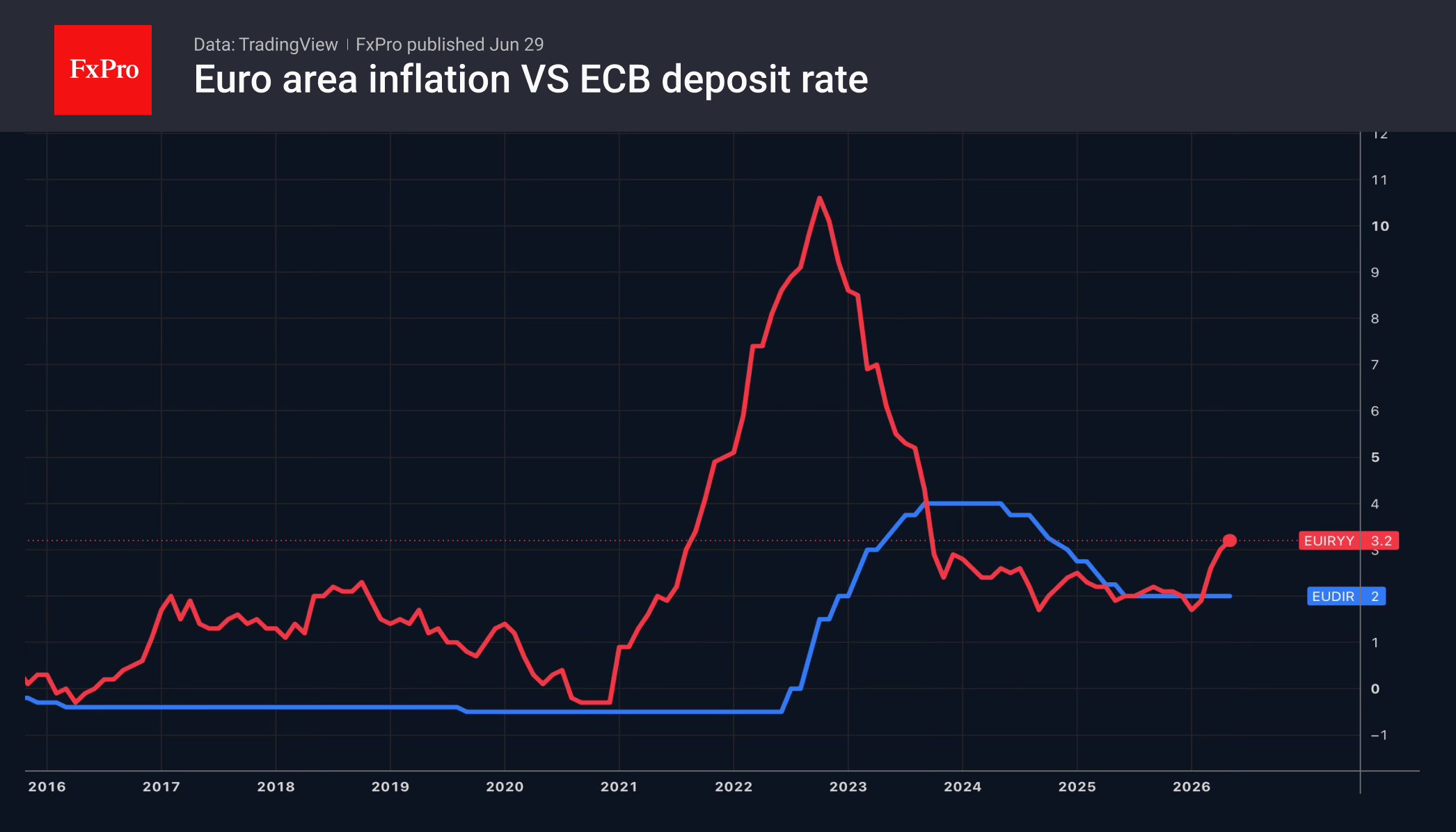

The Fed’s ‘hawkish’ shift and Christine Lagarde’s ‘dovish’ rhetoric have sent EURUSD tumbling to annual lows. Investors will be looking for confirmation of the downtrend in data on European inflation and the US labour market. Bloomberg experts expect consumer prices in the eurozone to slow from 3.2% to 3% in June. If inflation is indeed peaking, there is no need to tighten monetary policy. This is bad news for the euro.

The improvement in employment trends this spring provided a reason to keep the federal funds rate on hold. Further stabilisation of the labour market will allow the Fed to raise it as inflation picks up. Divergence in monetary policy will continue to support the ‘bears’ on EURUSD. If, at the same time, oil prices start to rise due to tensions in the Middle East, the euro risks falling to $1.1.

Brent continues to react to good news and turn a blind eye to the bad. Rumours of a ceasefire and negotiations have had a greater impact on the North Sea crude than the resumption of Tehran’s attacks on tankers and US airstrikes on Iran. However, if fears continue to hamper traffic through the Strait of Hormuz and slow the process of restoring oil production in the Persian Gulf to pre-war levels, prices will soar. This will support the US dollar as the currency of a net exporter of energy commodities.

The FxPro Analyst Team