The Bank of England sank the pound

February 06, 2026 @ 18:51 +03:00

- Markets now price the BoE to cut its rate in March.

- Neither slowing inflation nor the strength of the euro scared the ECB.

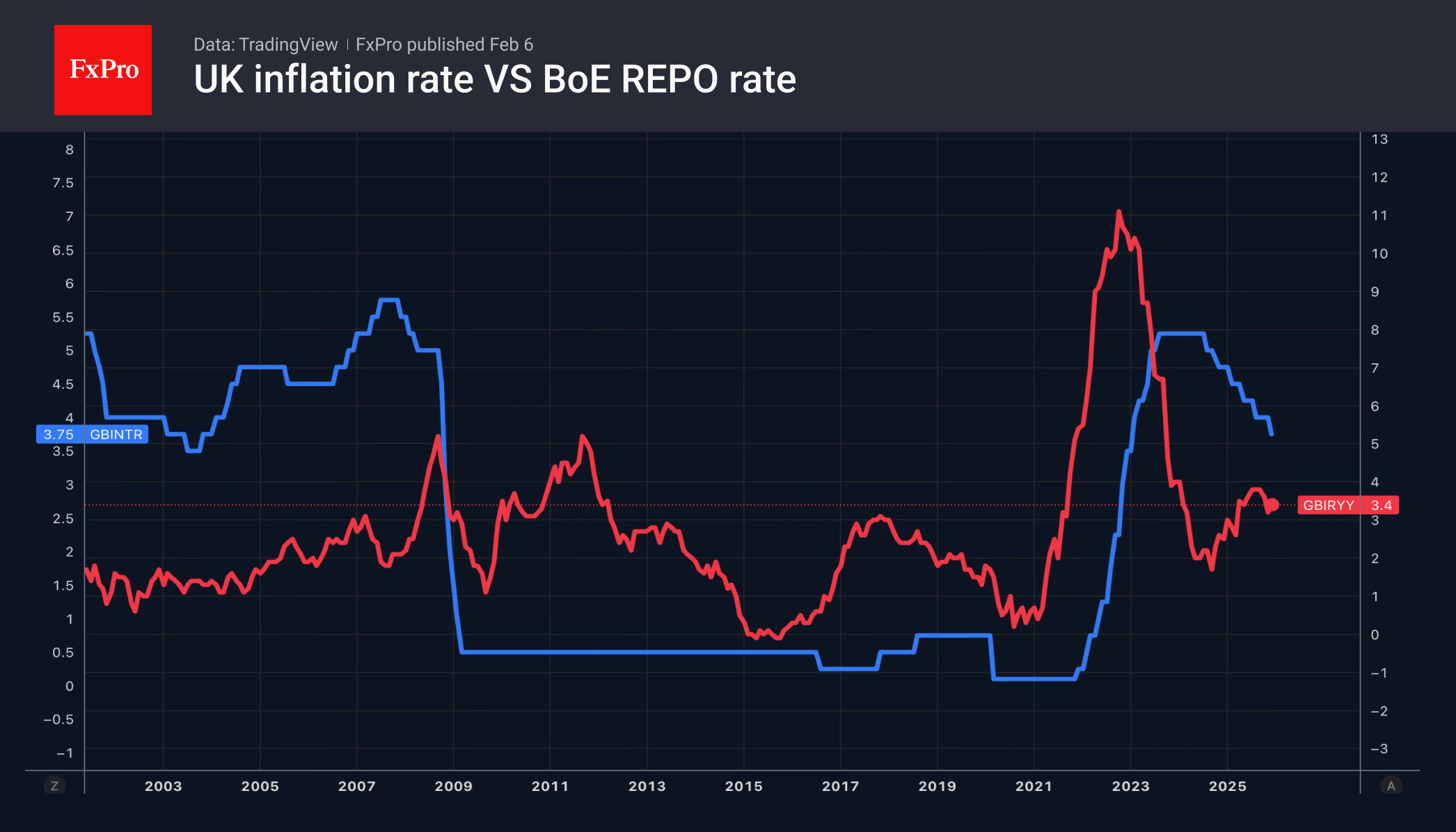

While the ECB decided to support its currency, the Bank of England deliberately sank the pound. Both regulators left rates unchanged, but this is a dovish pause. Four out of nine MPC members voted to cut the repo rate from 3.75% to 3.5%, while markets had expected only two.

Andrew Bailey noted that there is an even chance of the next rate cut next month, as inflation is sure to fall significantly. As a result, the futures market raised the probability of such an outcome from 20% to 60%, pressuring GBPUSD.

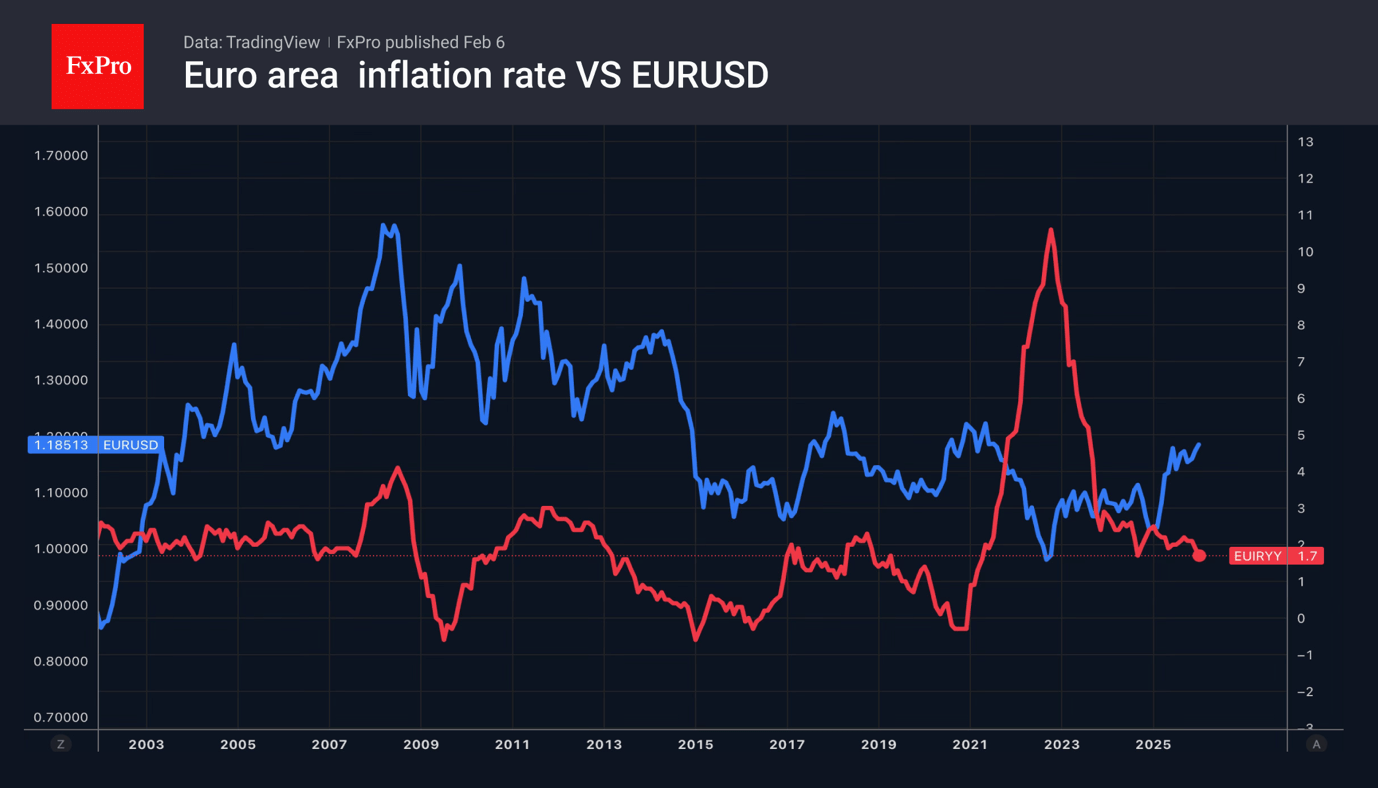

The ECB showed much more mercy to the euro. On the eve of the Governing Council meeting, investors were concerned that the slowdown in inflation in the eurozone to 1.7% in January and the 13% strengthening of the euro against the USD over the past year would provoke ‘dovish’ rhetoric from Christine Lagarde.

But eventually, she noted that the ECB would not make decisions based on a single data point and that the strengthening of the euro was already factored into its forecasts. EURUSD bulls breathed a sigh of relief.

They were helped by disappointing data on the US economy. In 2025, it created 1 million fewer jobs than in 2024. According to Challenger, layoffs are occurring at the fastest pace since the global economic crisis of 2008-2009. ADP is signalling a slowdown in employment, and unemployment claims are exceeding forecasts.

The Fed has already cut rates three times pre-emptively in response to signs of a cooling jobs market. If the negative trends continue, the monetary easing will resume earlier than expected. After a series of disappointing reports, derivatives have raised the odds of an April rate cut to 40%. If the BLS employment statistics bring an unpleasant surprise, they could rise to 50%, which is bearish for the US dollar.

It is hard to say how the greenback will react to the armed conflict in the Middle East. The erosion of confidence in it due to Donald Trump’s policies has led to the loss of its status as the main safe-haven asset. Gold has taken its place. However, the January-February sell-off of the precious metal and rumours of a burst bubble could change everything. Will the US dollar regain its former glory?

The FxPro Analyst Team