Oil retreats within an upward channel

March 25, 2024 @ 14:48 +03:00

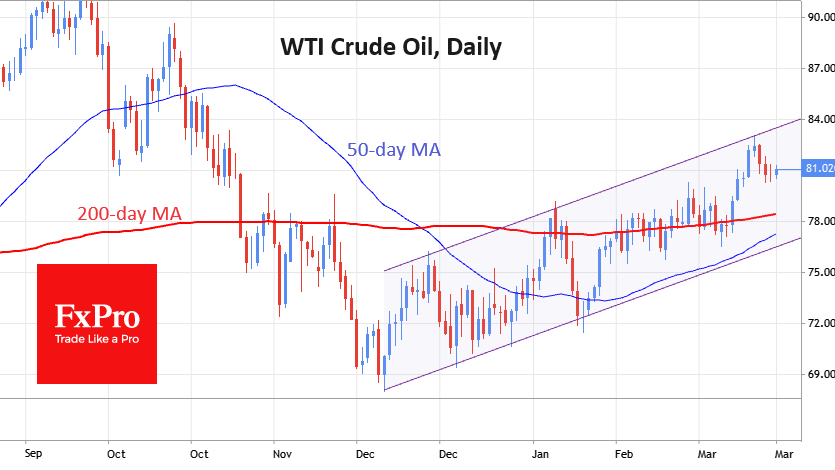

Oil closed last week with minimal gains, settling just above $80 per barrel WTI.

It appears that much of the commodity speculation has moved into cocoa, leaving oil at the mercy of longer trends.

WTI has been trading in a bullish range since mid-December, and since the beginning of last week, a further pullback from the upper boundary has been indicated. The logical course of events is now a correction to the lower boundary of the channel, which is now at $76.4, adding around $0.4 per day.

On the way down, the oil will encounter two important support levels. The first is the 200-day moving average (now at $78.4) and the 50-day average ($77.2). Both lines are pointing up, and there is a “golden cross” formation, which adds to the speculative interest.

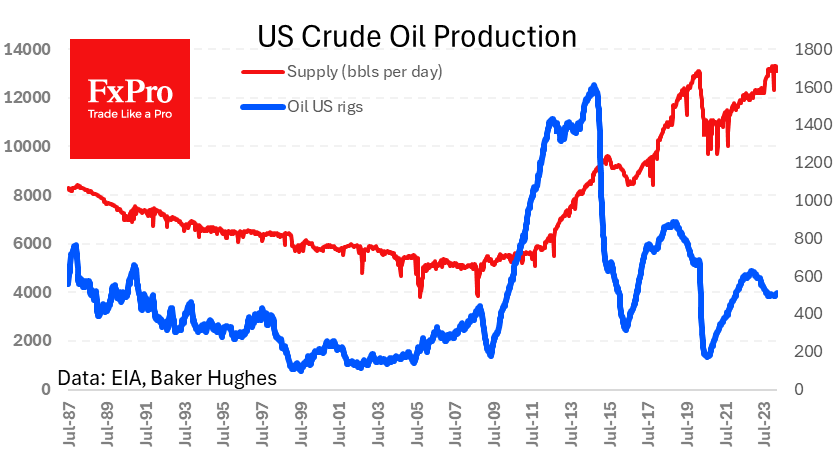

Friday’s data showed a decline in the total number of active drilling rigs to 624. This figure has been relatively stable since last November, after falling since the beginning of 2023.

There is also no upward trend in oil production, which has fallen back to 13.1 million bpd in recent weeks after hitting a record 13.3 million in February.

This passivity on the part of producers is a bullish sign for oil, as China’s economic stimulus and India’s excellent health are the two countries with the greatest potential to boost demand. Meanwhile, supply remains constrained by OPEC+ quotas.

However, it may well be that oil’s rise will be smooth and largely out of sight of active speculators until it passes $90. Out of the trading range from August 2022. Oil’s ability to go higher promises to attract the attention of speculators and central bankers alike, with implications for monetary policy via consumer prices.

The FxPro Analyst Team