Oil is in no hurry to reverse course

April 01, 2026 @ 15:40 +03:00

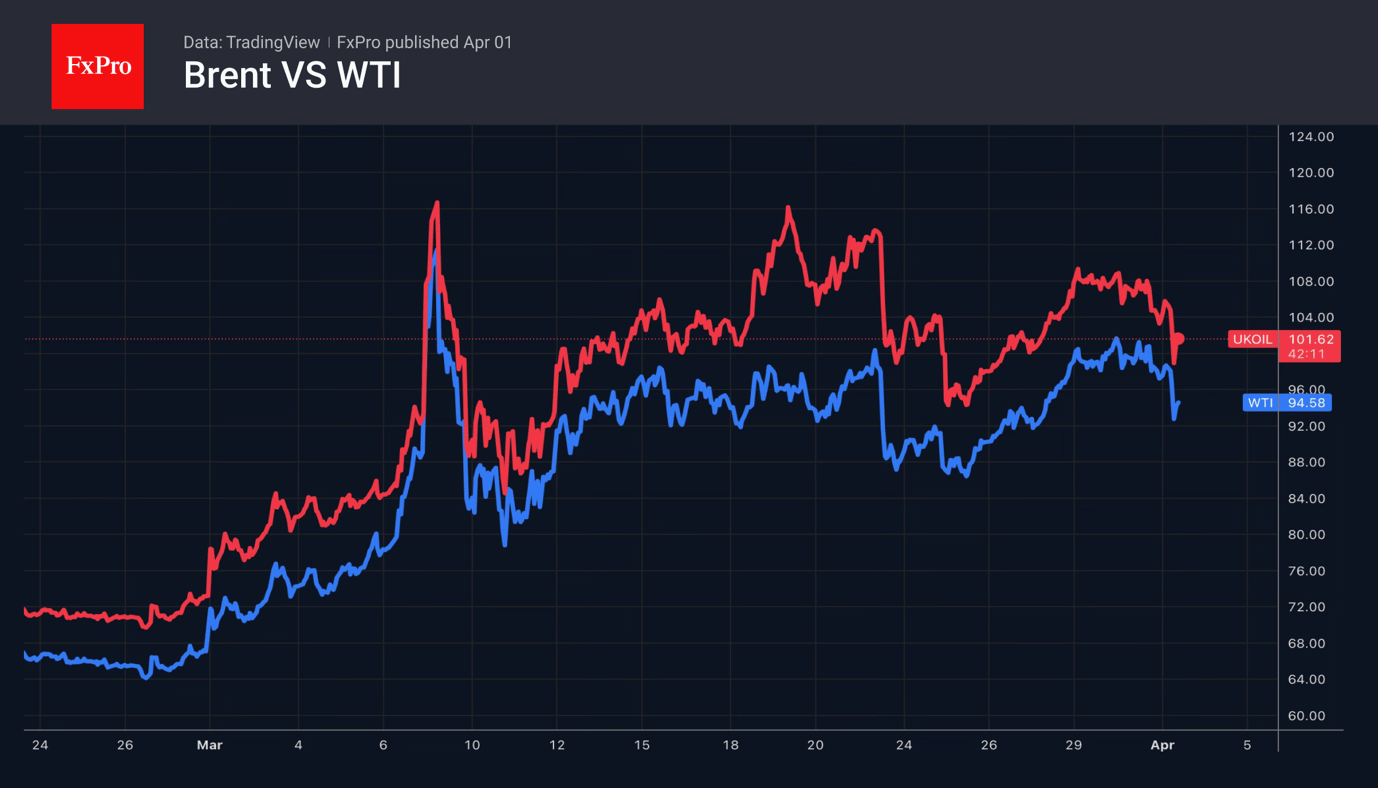

- March was a record-breaking month for Brent.

- Rumours of peace are easing tensions but have not yet reversed the trend.

The oil market was swept up in euphoria following Donald Trump’s comments that the conflict in the Middle East would end within 2–3 weeks. After a record 63% rally in March, Brent took a step back. Investors are ready to use TACO and sell what they bought earlier. However, complacency is the main risk for black gold.

Firstly, the US continues to deploy troops to the region, and the past year has taught investors to watch the actions, rather than the rhetoric, of top American politicians following the dashed hopes surrounding the Iran–US negotiations. But even if this is true, the Americans’ withdrawal from the Middle East does not mean the end of the conflict. The US President is calling on countries in the region to learn to defend themselves and on importers to come and take the oil they need by force. As a result, the UAE is prepared to get drawn into the conflict.

According to estimates by FGE NexantECA, a closure of the Strait of Hormuz would result in losses of 100 million barrels per week and 400 million barrels per month. If it lasts another 6–8 weeks, Brent could reach the $150–200 range. This forecast is in line with Sociénéété Generale’s estimate of $150 per barrel and Macquarie Group’s estimate of $200. The Iranians are also warning the world of a rise to the upper end of this range, while the US presidential administration calls $100 the ‘base’ price and does not rule out $200.

Even if the Strait of Hormuz is reopened, it will take considerable time to restore pre-war infrastructure. The flow of tankers will not return immediately; supply issues will ease but will not disappear. It is unlikely that Brent will return to levels near $60 by the end of the year, as seen at the end of last year.

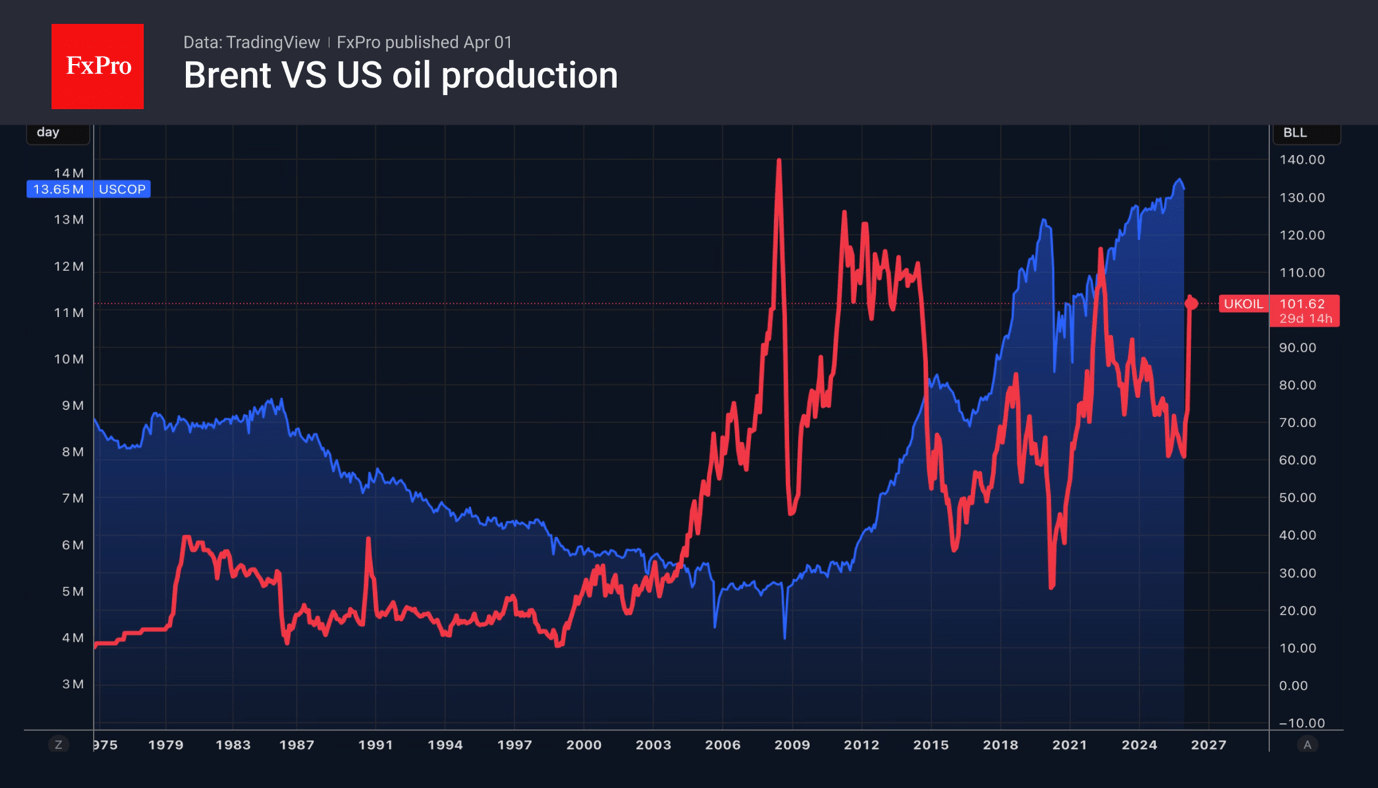

Unlike in 2022, US drillers are in no hurry to come to consumers’ aid, producing an average of 13.2 million bpd in January, down from 13.9 million bpd in October. The decline in production over the last three months is one of the largest in the last ten years.

The US oil industry prefers paying dividends to shareholders rather than developing new fields and increasing production, despite Donald Trump’s “drill, baby, drill” call. Consequently, without an end to the conflict in the Middle East and the reopening of the Strait of Hormuz, it is premature to expect prices to return to February levels.

The FxPro Analyst Team