Markets have resumed declining on strengthened international disputes

October 15, 2018 @ 11:43 +03:00

Asian markets start the week with a decline, failing to develop its Friday rebound. MSCI Asia ex Japan loses 1%, China A50 index, the largest 50 blue chips of the Shanghai exchange, loses 1.3%. The head of the People’s Bank of China noted at the weekend that there is a significant potential to reduce reserve requirement rate further.

However, the markets look at this as a sign of uncertainty in the economic growth of the country in the short term after the most severe decline in car sales in the last 7 years. Internal statistics from China will be in the spotlight ahead of external trade, as the markets try to assess the extent of the U.S. tariffs impact on China. The surge in foreign trade is seen as a temporary factor, risking to turn into an impressive collapse.

In addition, it is feared that a new portion of the wrath and sanctions of Washington will now turn to Saudi Arabia. The disappearance of a journalist criticizing the kingdom provoked a sharp reaction from the business community and political circles. Impulsively it caused the growth of oil at the opening of markets to $81.40. But the weakening of the demand for risky assets has returned oil quotations below $80.90 at the time of writing.

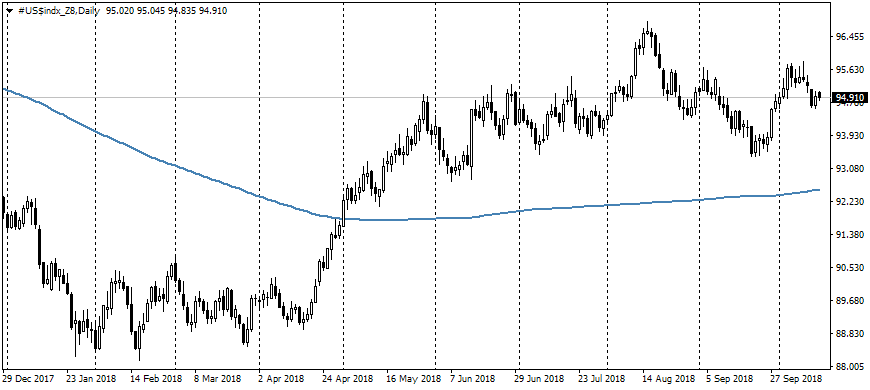

A similar story happened with the American dollar. It started trading the week with a gap of 0.2%, briefly reaching the 95.0 mark. However, as liquidity returns to markets, the demand for the dollar as a defensive asset is somewhat declining, returning the trend of the previous week: the simultaneous decline of the dollar and the markets.

The simultaneous movement of the dollar and stock markets is rare and lasts for very limited time. At the moment, this trend is driven by the speculation that the U.S. economy may lose its growth momentum as a result of the already-raised stakes, forcing the Fed to act more carefully in the upcoming quarters. For example, the Fed expects to raise the stake three times in 2019, while the markets are uncertain even in two increments.

However, to our mind, the chances are higher that the Fed will be right again, forcing the markets to bring its estimates closer to the forecasts of the central bank. This shift is potentially favorable for the dollar, but it is able to restrain the growth of the stock markets, making investments in shares less attractive in comparison to the growing yield of government bonds.