Markets Are Celebrating… Right Before a Shock?

April 20, 2026 @ 09:09 +03:00

US Dollar

Over the past two weeks, the US dollar has fallen to its lowest level since early March, giving back almost all the gains made since the start of the armed conflict in the Middle East. Talks with Iran are set to resume in the coming days. Donald Trump continues to insist that the war will end soon and that an extension of the ceasefire will not be necessary. Coupled with record highs in US stock indices, this is contributing to the continued rally in EURUSD, as geopolitics has ceased to support the greenback, bringing macroeconomics back into focus.

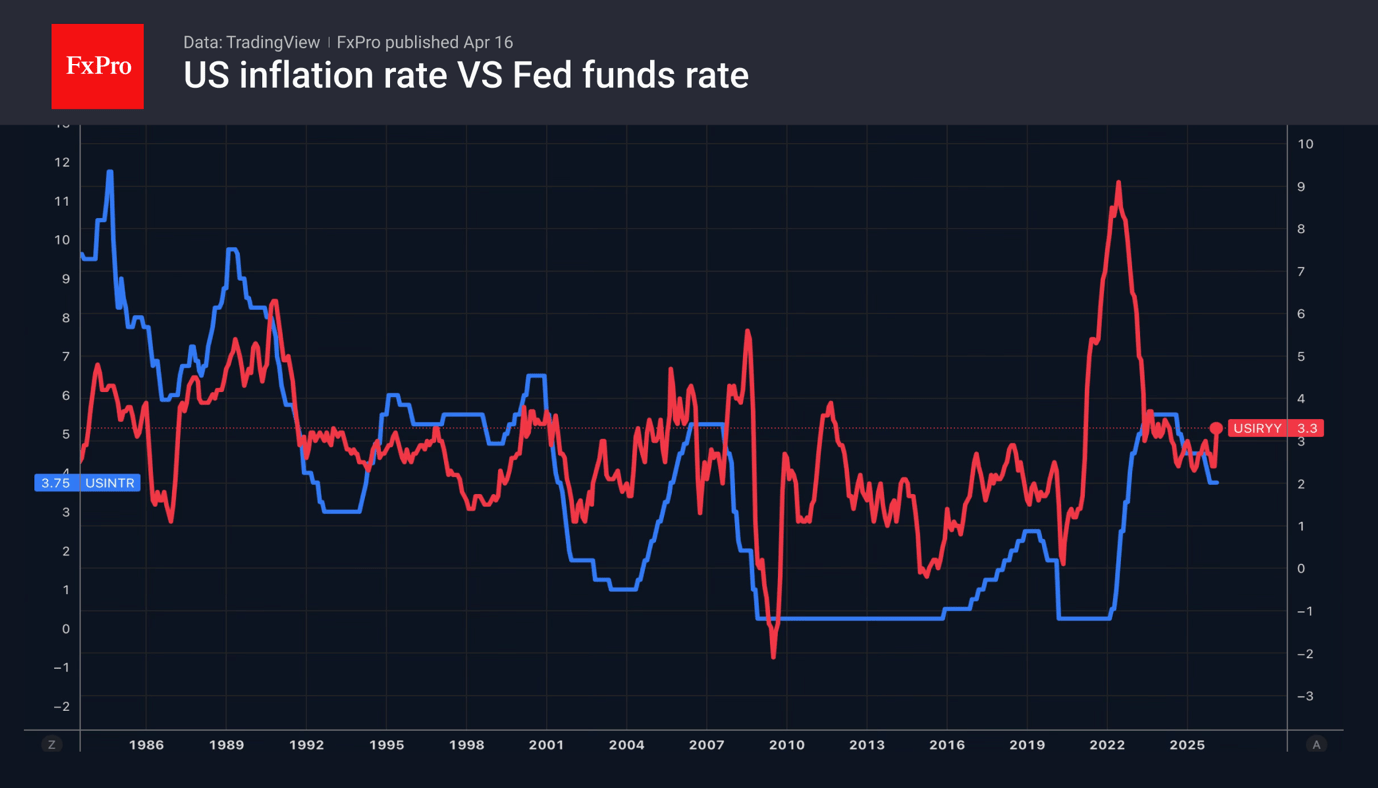

Investors’ attention has also shifted to corporate earnings reports and Congress’s deliberations on Kevin Warsh’s nomination for the post of Fed Chair. Contrary to Trump’s promises, the replacement of the Fed Chair may coincide with accelerating inflation driven by rising oil prices, requiring a tightening of monetary policy. What will Warsh choose? To justify the president’s trust or to demonstrate the central bank’s independence and stick to its principles?

Investors are drawing parallels with the 1970s, when an inflationary shock amid the oil crisis saw the Fed chair, who was loyal to the White House, ease monetary policy. The rate cuts resulted in an even sharper rise in consumer prices and reinforced high inflation expectations. At that time, the US dollar collapsed. It was only after a change in central bank leadership and aggressive monetary tightening, despite the recession, that the dollar began a steady rise from the summer of 1980.

Stock indices

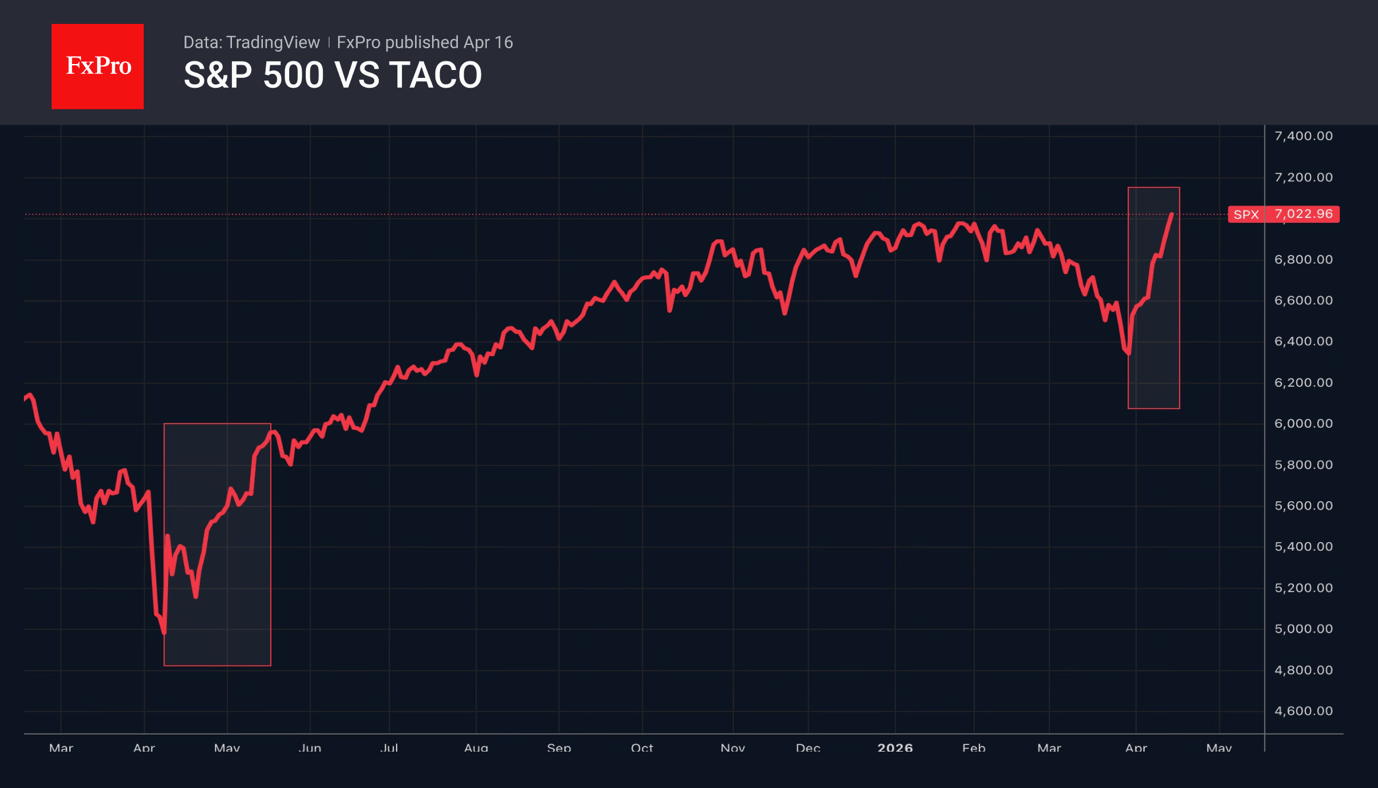

Confidence in an approaching end to the war in the Middle East, the resilience of the US economy to geopolitical shocks, and expectations of a strong first-quarter earnings season enabled the S&P 500 to surpass the January record highs.

About a year ago, after the White House introduced tariffs, the broad stock index first fell and then surged as Trump Chickens Out. Nowadays, since late March, the fear of missing out on TACO has been driving strong volumes, as investors who missed last year’s rally rush to catch up.

Usually, such sharp surges occur from the very bottom of a bear market. This time, the S&P 500 has lost less than 10% from its January highs. So, it has not even been officially called a correction. Something similar occurred only in March 2000, on the eve of the dot-com bubble bursting. For history to repeat itself, an escalation of the conflict in the Middle East would be required, which seems unlikely.

Gold

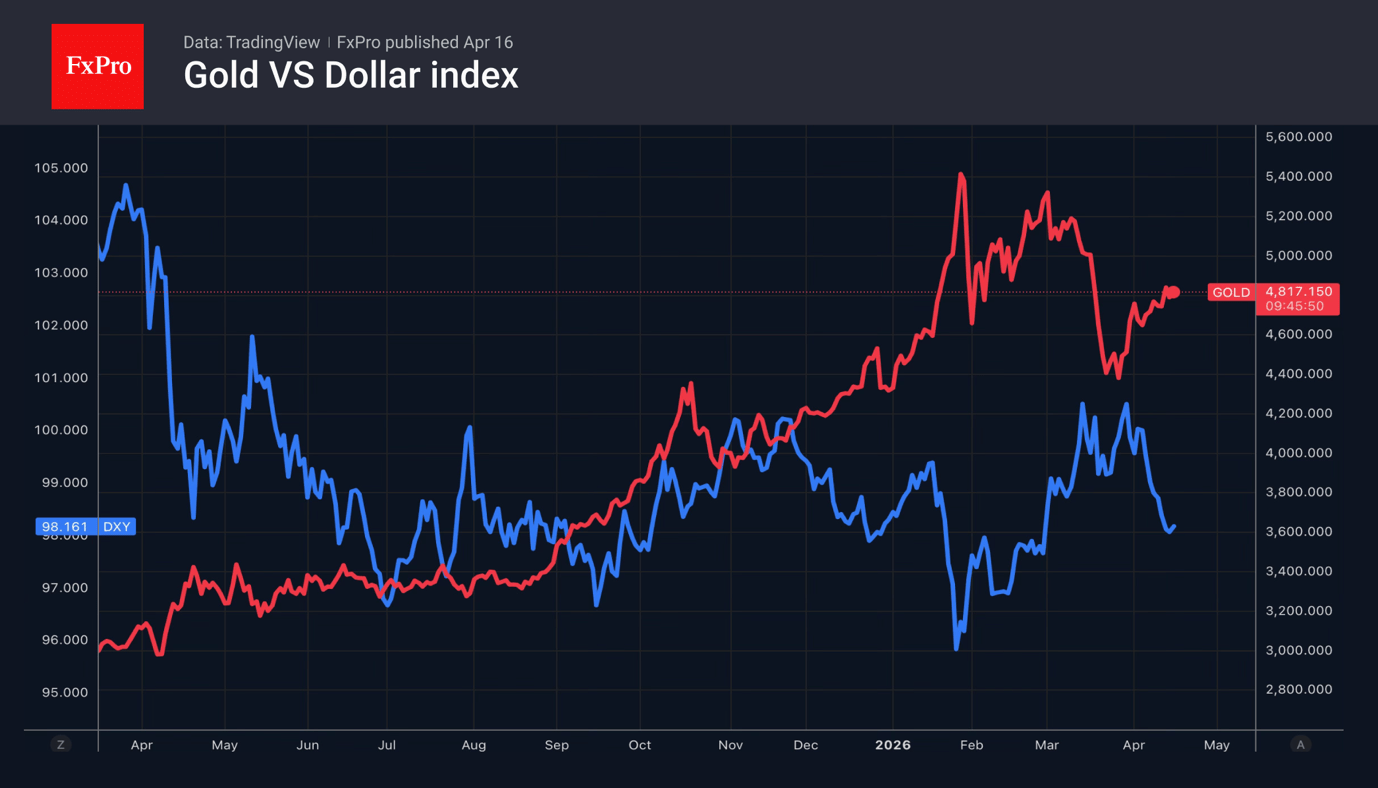

Gold is slowly but surely recouping its losses on expectations that a peace deal between the US and Iran will bring down oil prices. This will curb inflation and dampen central banks’ appetite for tightening monetary policy. Fears on this front led to a decline in gold prices during the Middle East conflict. Now that Bloomberg has reported that the parties are ready to extend the ceasefire agreement, the situation has done a complete U-turn.

The precious metal will be supported by uncertainty over White House policy and the associated decline in confidence in the US dollar. Donald Trump has resumed his attacks on Jerome Powell. The US president intends to sack the Fed chair if he remains on the FOMC after his term ends. The Republican claims that interest rates will start to fall as soon as Kevin Warsh takes the helm of the central bank. He will have to face a confirmation hearing in Congress.

The revival of the idea of easing the Fed’s monetary policy, driven by the weakness of the US economy or the new Fed Chair, will act as a tailwind for gold.

Crypto

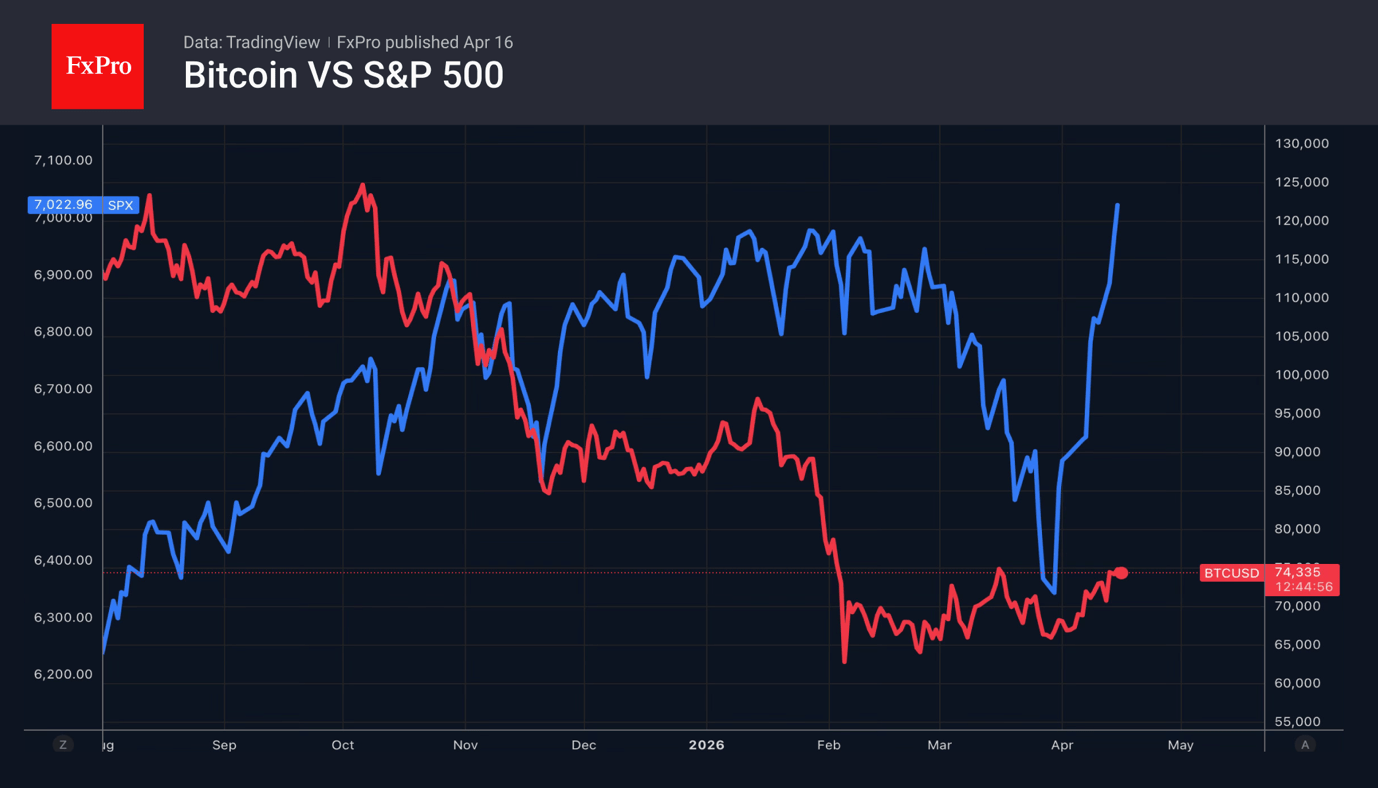

The de-escalation of the conflict has triggered a rally in Bitcoin. However, Bitcoin is not rising as quickly as the US stock indices. There is a view that the factor holding back the upward movement is Congress’s consideration of the Clarity Act, which would regulate the circulation of cryptocurrencies. As soon as lawmakers approve it, enthusiasts expect a rally in digital assets.

However, the market situation has actually changed significantly. Over the last couple of years, its structure has shifted. Whereas crypto-whales previously dominated, their share is now declining. The proportion of institutional investors is growing, leading to lower volatility and limiting the potential for a Bitcoin rally.

Miners’ approach to the business is also changing. The cost of electricity for Bitcoin mining is higher than for artificial intelligence data centres. CoinShares forecasts that data centres’ profitability will rise from 30% to 70% by the end of the year. This increases the likelihood that crypto miners will sell their tokens, thereby holding back BTC.

What next?

The ceasefire in the Middle East expires on the 21st of April. Investors will be watching closely for its extension, with a view to peace negotiations between the US and Iran. De-escalation of the conflict is the base-case scenario. In the event of an escalation, demand for the US dollar will surge.

Congress’s consideration of Kevin Warsh’s nomination for the post of Fed Chair could turn into a real thriller. Not all Republicans are prepared to support Donald Trump’s choice.

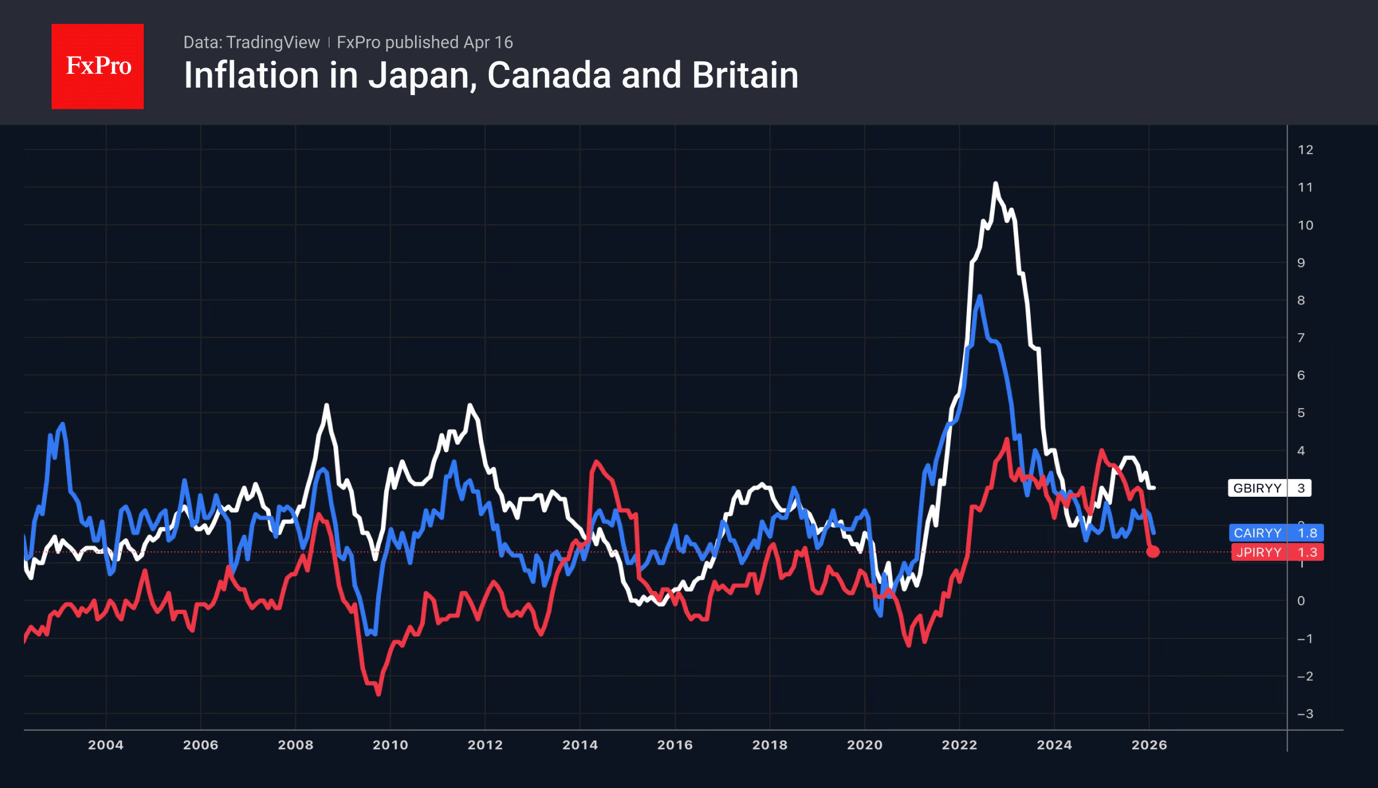

Investors will be keeping a close eye on the corporate earnings season and the economic calendar. Inflation data from Canada, the UK and Japan will help gauge the impact of high oil prices on the CPI and offer clues about central banks’ next steps on monetary policy. It will be quite interesting to observe the Forex market’s reaction to reports on business activity in European countries and the US, as well as to the release of US retail sales data for March.