Crypto Long & Short: Is ETH Coming to Corporate Balance Sheets?

March 08, 2021 @ 13:31 +03:00

MicroStrategy, Tesla and Square have done it. So have many others, although more quietly. I’m talking about holding corporate treasury reserves in bitcoin. This trend is attracting attention even from trade press. Consultancies and crypto companies are scrambling to launch services to help businesses navigate the process. “Mad Money” host Jim Cramer thinks it’s “almost irresponsible” for companies to not do so. This week, sponsored content from Deloitte explaining the benefits and risks appeared in the Wall Street Journal.

Whether it’s a good idea or not – that’s up to each corporate treasurer to decide – one question we’re starting to hear is: “What about ether?” Would the native token of the Ethereum blockchain make a good corporate reserve asset?

Bitcoin on balance sheets

The main arguments for bitcoin as a corporate reserve asset are:

The asymmetric risk return

As part of a future-first strategy

In preparation for accepting bitcoin as payment

It is more likely to hold its value going forward than the dollar

This last point is key, as the main role of the corporate treasury function is the preservation of capital. Here bitcoin’s leading value proposition – as a store of value – comes into play.

Critics will point out that bitcoin is way too volatile to be a store of value. That’s a short-term view of the concept, however. Over the next week, month, perhaps even year, bitcoin’s price may fall relative to fiat currencies. Longer term, however, in an environment of money supply increasing much faster than demand, a fixed-supply bearer asset such as bitcoin is likely to appreciate in value relative to assets without a fixed supply, such as the U.S. dollar. As investor Paul Tudor Jones pointed out, even at only the 2% inflation target, cash is a “wasting asset.”

Do these arguments hold for ether? Not so much, no. But that doesn’t mean ether won’t end up on corporate balance sheets.

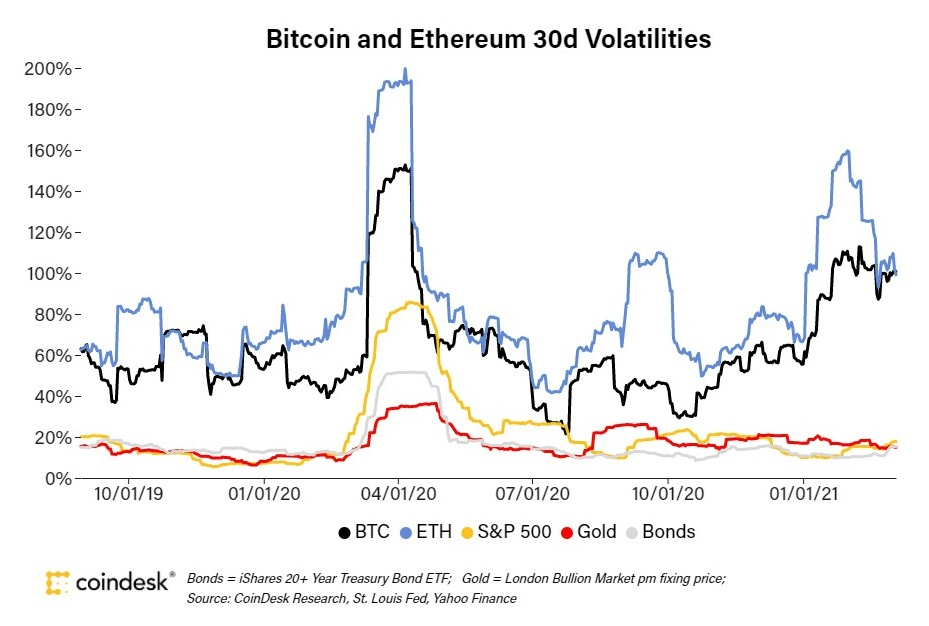

Ether’s supply has no limit. It is still considered a store of value, however, as its supply growth is modest (currently around 4%, expected to decrease over time) and likely to remain well below growth in demand. Yet the store of value narrative is not – at this stage – the main driver behind ETH’s investment case, especially in the eyes of institutional investors.

Ethereum is seen more as a technology play. More than that, it’s one of the more liquid, experimental technology plays accessible to investors today. It’s not just trying to build a faster rocket or streamline dentistry. It’s aiming to reinvent the way automated applications of any type are run. Its goal is to build the ultimate base layer of a global digital economy. As well-known macro analyst Jim Bianco said earlier this week, decentralized finance is “recreating the entire financial system.” Ethereum-based applications are also likely to impact markets, governance, energy, public services, perhaps even how identity is managed.

The accumulation of ether as working capital may have already started. This week, Meitu – a software and social media app company listed on the Hong Kong Stock Exchange – disclosed purchases in bitcoin and ether of approximately $18 million and $22 million respectively.

Crypto Long & Short: Is ETH Coming to Corporate Balance Sheets?, CoinDesk, Mar 8