China’s coming recession has pushed oil below $60

November 14, 2018 @ 08:01 +03:00

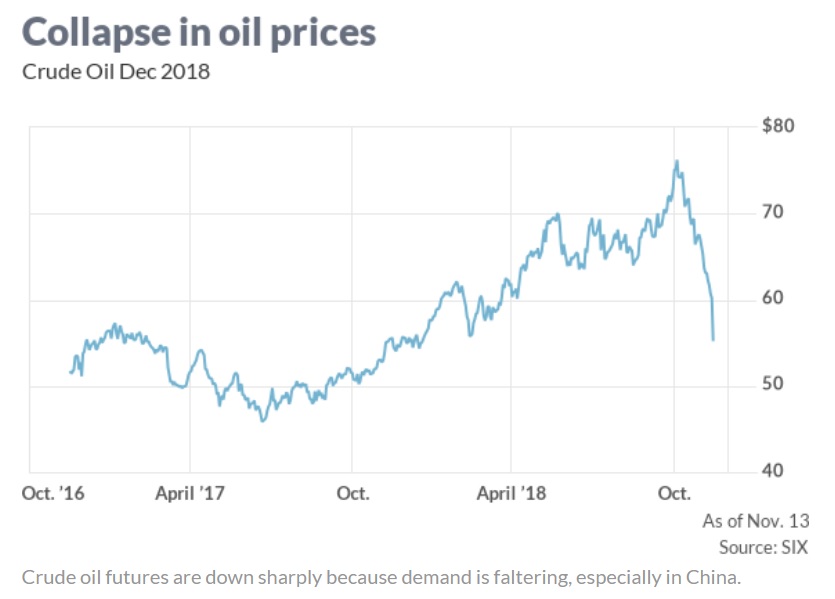

Most market participants are having a hard time explaining why the price of crude oil CLZ8, -0.48% dropped like a rock during a time when the United States began to enforce sanctions on Iranian exports on Nov. 4 — sanctions centered on the extraordinary demand that the world stop buying Iranian oil (with generous exemptions). I’d say that a 20% decline in the price of oil in about a month falls into the category of rare events and may not have anything to do with supply, but rather that other driver of prices called demand.

Which country is the largest importer of oil, and therefore the largest driver of crude oil prices on global markets? China. In 2017, China overtook the U.S. as the largest importer of oil, so economic developments in China should be closely monitored by oil traders, as the Chinese economy is likely headed into a massive recession, and not due to the present trade frictions with the Trump administration.

The previous time we had such a sharp drop was in 2014-15, and that was clearly due to Chinese economic deceleration coupled with surging U.S. shale production. In 2018, we again have surging U.S. oil production, which surged past 11 million barrels per day, and we also have a decelerating Chinese economy driven by the belated actions of the Chinese government to deleverage its financial system. It is true that in prior years we have had bigger declines that were not primarily driven by China, the most notable of which was 2008, but China was not the dominant force in the crude oil market then. Today it is.

The Chinese “economic miracle” is built on a mountain of debt. As Chinese GDP grew over 12-fold in 20 years to $12.24 trillion at the end of 2017, credit in the Chinese financial system grew over 40-fold, taking the debt-to-GDP ratio from 100% to 400%, if one counts the shadow banking system. Shadow banking credit aggregates are omitted from official statistics, but they add at a minimum 100% to the total debt to GDP ratio for China.

The fact that such centralized macroeconomic management has worked for 25 years does not mean that it will keep working forever. I do not believe the Chinese can eliminate the economic cycle. Instead, the credit bubble that they have engineered will cause the coming recession to be a lot worse than it otherwise would have been, drawing parallels to the 1930s Great Depression in the U.S.

I think that what we will see in China, soon, will be the equivalent of what we saw in 2008. The final outcome will depend entirely on the policy response of the Chinese authorities. The American authorities made a lot of mistakes in 1929 and following years, resulting in the Great Depression. In 2008, the American authorities did not repeat those mistakes. I think we will find out soon enough what outcome the Chinese authorities will end up creating.