Central banks are trying to get back into the spotlight

March 16, 2026 @ 13:27 +03:00

- A flurry of central bank meetings is coming up this week.

- Gold is under pressure amid a shift in the outlook for Fed rates.

Confidence in the Fed is growing, but this is not saving the central banks. The conflict in the Middle East has pulled the blanket over itself. It has become the main driver of pricing in the financial markets. The federal judge’s ruling that the Justice Department’s subpoenas to Jerome Powell were unlawful has provided yet another reason to buy the US dollar. If the Fed is under protection, it is not possible to put pressure on it to cut rates.

The US President has come up against a brick wall with the Supreme Court and the Federal Court in cases concerning tariffs, as well as against Jerome Powell. The chances of him succeeding in dismissing FOMC Governor Lisa Cook are also slim. A blitzkrieg against Iran is not working out either. Tehran has no intention of surrendering, however much Trump tries to convince the markets otherwise.

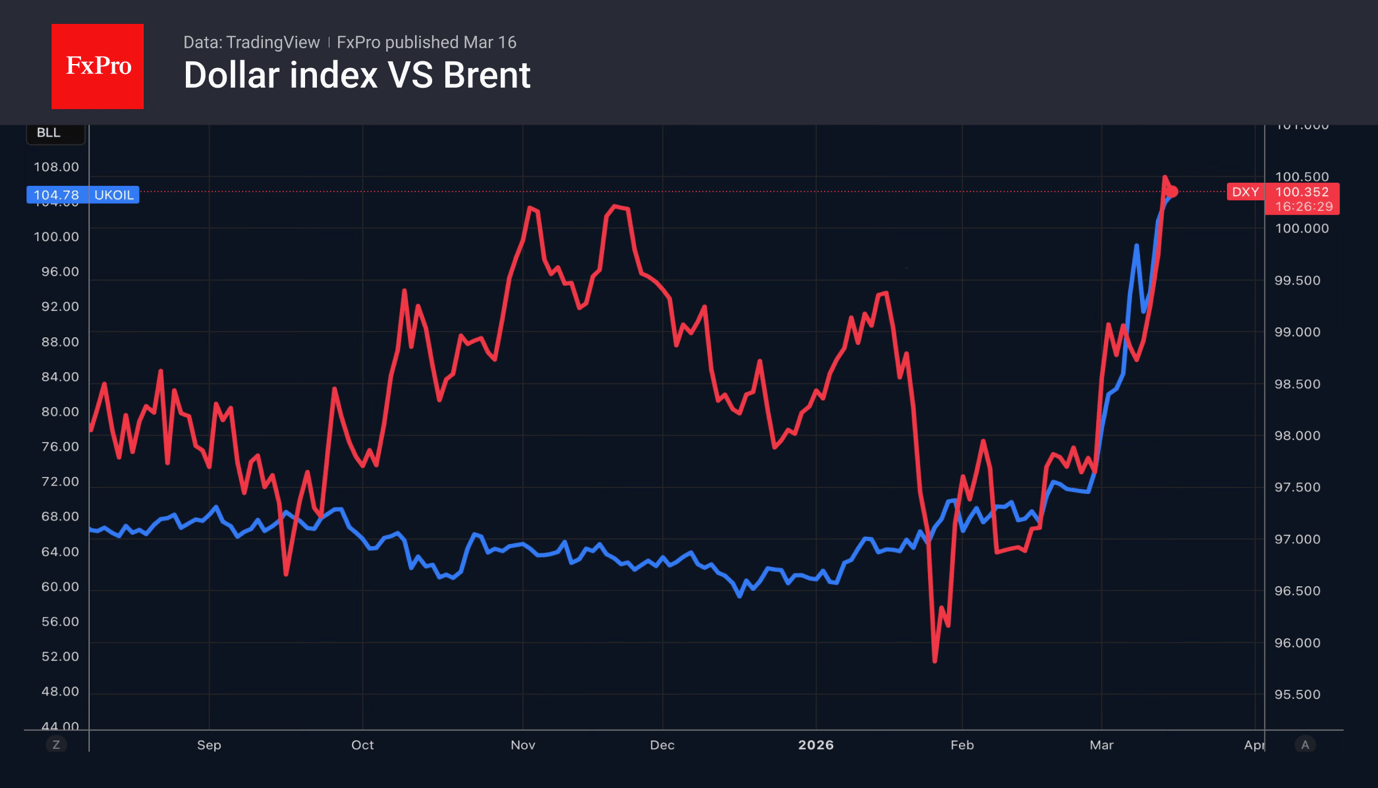

The plan to release 400 million barrels from strategic reserves is failing. It will take time to implement. The maximum that IEA members can put on the market is 3 million bpd. Even by the most optimistic estimates, the loss of global supply due to the closure of the Strait of Hormuz amounts to 10 million bpd. Oil prices continue to rise, and as Brent rallies, central banks’ hopes of regaining their role as the main newsmakers in the Forex market are fading.

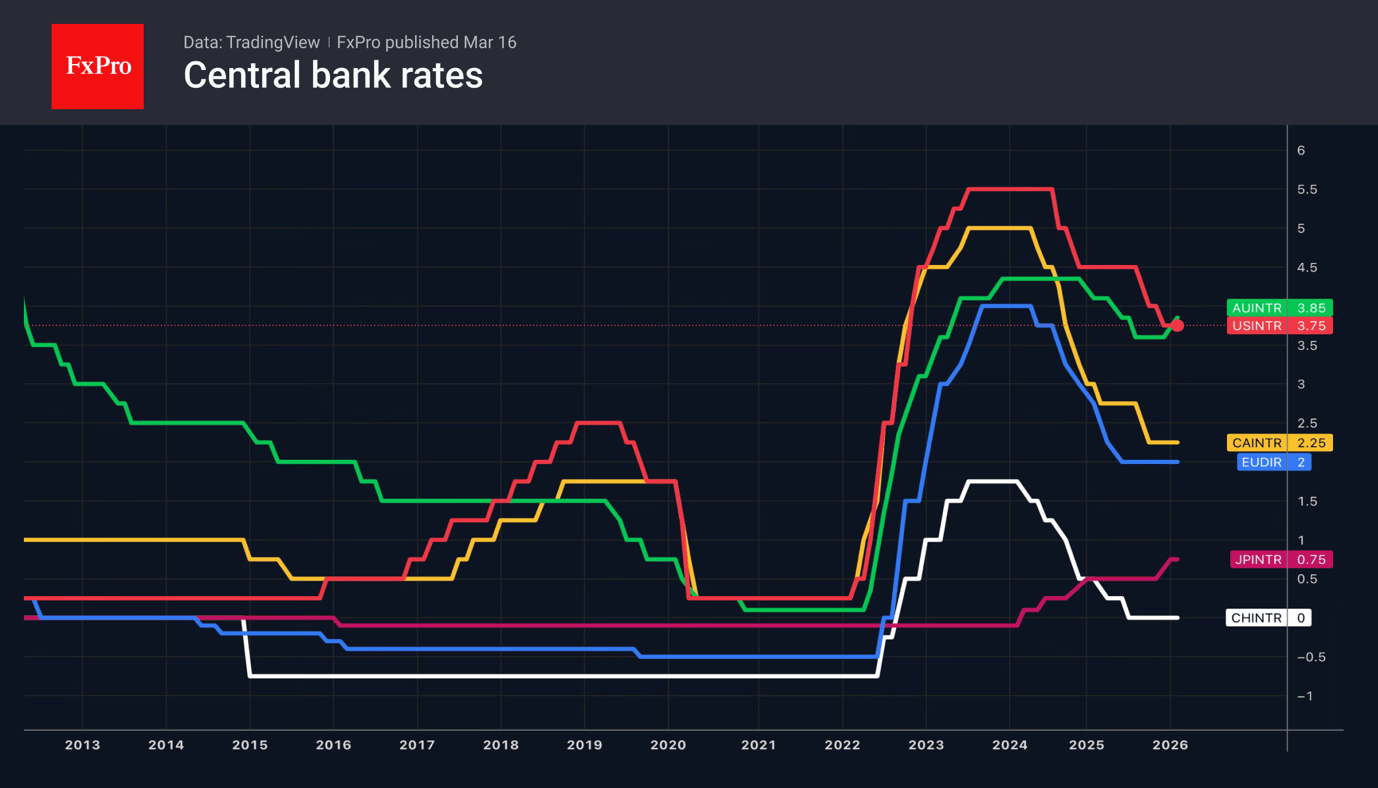

It has been a while since we’ve seen such a packed five-day schedule of central bank meetings. Whilst the Fed is certain to discuss the two-way risks posed by the conflict in the Middle East to the US economy, the ECB and the Bank of Japan are likely to hint at near-term rate rises. The RBA is even ready to raise the cash rate to 4.15%, which provides a tailwind for the Australian dollar.

The Federal Reserve, the Bank of England, the Swiss National Bank, and the Bank of Canada intend to extend the pause in their policy-easing cycles until the end of the year. The higher the rates, the greater the appeal of currencies and bonds denominated in them. Gold must now forget about debasement trading, which served it faithfully in 2025 and early 2026.

The precious metal feels out of its depth against the backdrop of the Fed’s rate cut prospects being pushed back from June to September and derivatives losing their illusions of two federal funds rate cuts in 2026.

The FxPro Analyst Team