Brent is heading towards de-escalation

May 06, 2026 @ 15:43 +03:00

- The markets are betting on a swift resolution to the US-Iran conflict.

- The fall in Brent and WTI prices is likely to be sharp but short-lived.

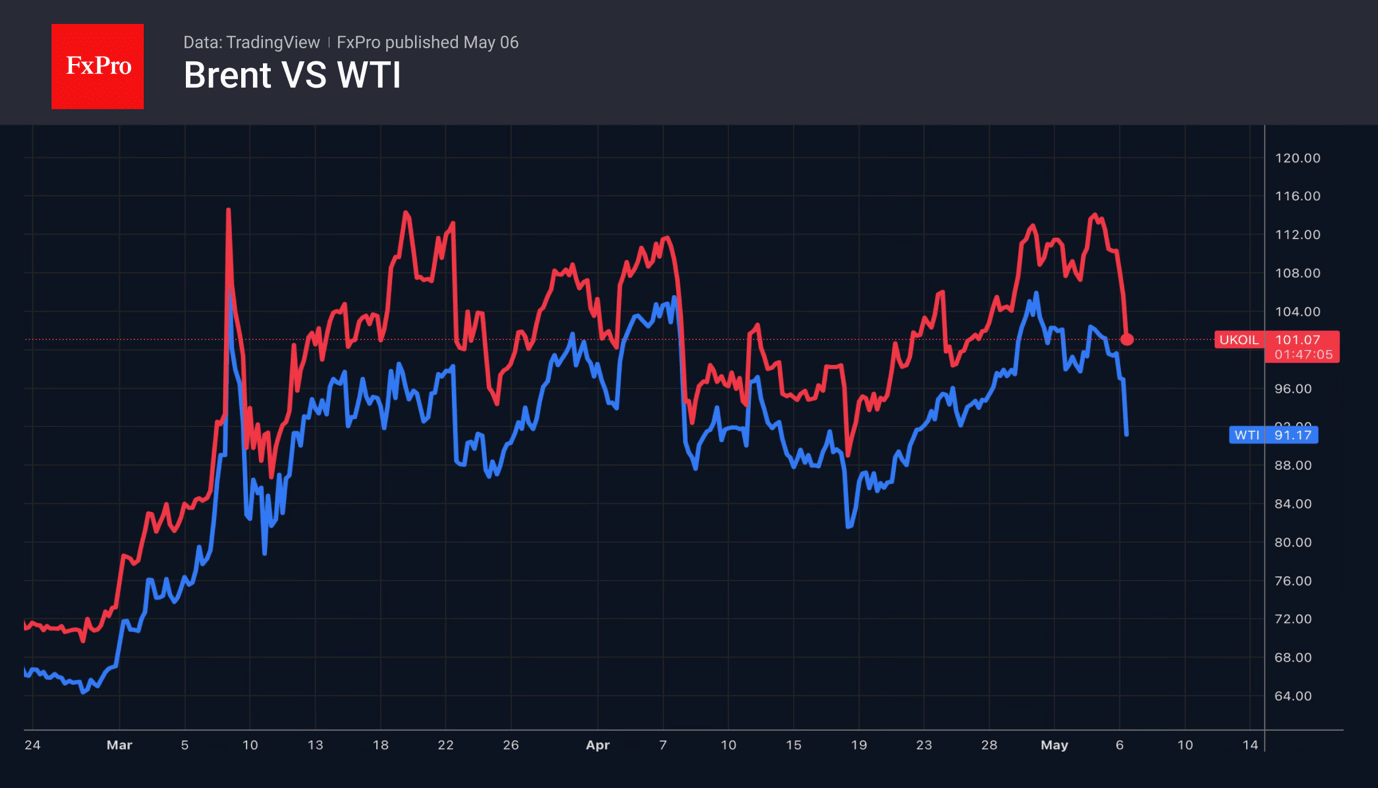

At the start of the week, the nearest Brent futures contract once again exceeded $113, hitting the ceiling formed since the start of the armed conflict in the Middle East following news that Iran had resumed attacks on the UAE’s energy infrastructure. However, on Wednesday, Brent crude fell by more than 10% intraday to $97, as the US announced the maintenance of the ceasefire and the conclusion of Operation Epic Fury. Donald Trump announced progress in negotiations with Tehran, and the latter noted that it was ready to strike a deal. This is a rather unusual turn of events, as we have almost become accustomed to a stream of contradictory statements.

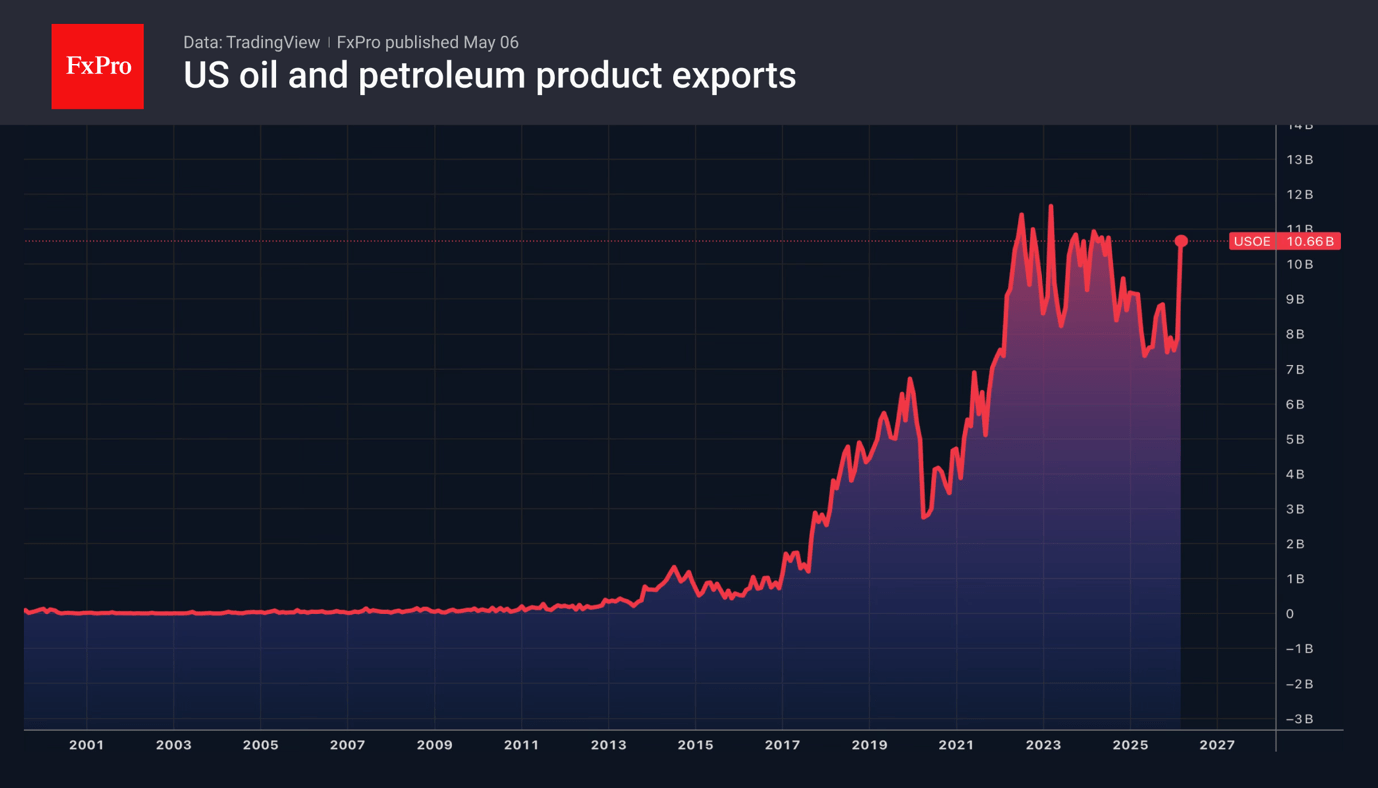

Looking to the future, markets are taking the words at face value, viewing the figures as a snapshot of the past. But in any case, Iran’s attacks on Fujairah have sparked fires and threaten to reduce global supply by a further 1.9 million bpd. Global oil reserves are rapidly dwindling. And the US has found itself in a better position to catch a tailwind, having become the world’s largest oil exporter, with around 6 million bpd, surpassing Saudi Arabia. In theory, the figure could reach 10 million bpd, but in practice, the ceiling is much lower, around 6–7 million bpd.

Russia has also benefited from the crisis in the Middle East. Its average crude oil flows over the past four weeks have jumped to their highest levels since December. Export revenue reached $2.42 billion for the week ending 3 May, the highest since February 2022.

Washington’s optimistic rhetoric and its reluctance to escalate tensions are allowing markets to view a peace agreement between the US and Iran as the base case scenario. A rapid resumption of shipping will lead to a short-term surge in supply from tankers stranded in the Strait of Hormuz, pushing down the price of Brent and WTI.

However, the depletion of global stocks and the time required to repair the damaged infrastructure in the Gulf states suggest that oil is unlikely to fall back to the levels seen at the end of February – below $72 for Brent and $67 for WTI – by the end of the year. Under this scenario, international trade risks losing more than 0.5 percentage points of growth. The World Trade Organisation’s March forecasts suggest a slowdown in growth from 4.6% in 2025 to 1.9% in 2026, with a partial recovery to 2.6% in 2027.

The FxPro Analyst Team