After a 7.5% overnight fall, Oil still looks vulnerable

March 19, 2021 @ 11:09 +03:00

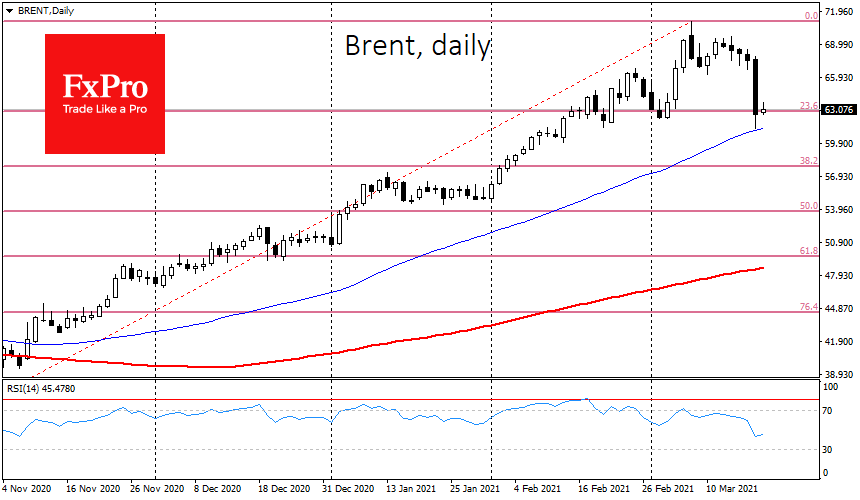

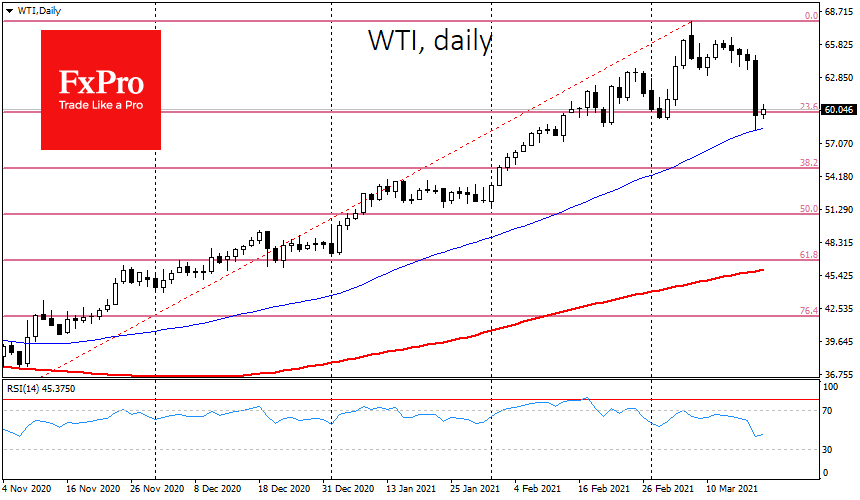

Oil took a steep fall yesterday, showing an almost 10% intraday trading range and a 7.5% drop for the day. Brent on the spot market moved down to $61.27 at one point, while WTI fell to $58.27.

Both had a very muted rebound on Friday morning, at risk of coming under renewed pressure with the start of active trading in Europe.

Crude Oil has been severely overheated after a rally since the beginning of November, almost doubling its price. Last month, the RSI indicator on the daily charts rose to its highest levels in at least ten years, indicating the most turbulent rally over that period.

In March, despite a brief moment of Brent being above $71 and WTI above $67.50, the RSI index pointed to the rally’s exhaustion. There were other signs, such as when Oil ignored positive news and slowly but surely diminished for five trading sessions in a row.

The pressure exacerbated the sell-off in equity markets, and the short-term bulls capitulated, explaining the decline’s amplitude on Thursday.

Locally, 50-day moving averages and the first Fibonacci retracement at 23.6% of the November-March rally provided Oil support.

Moving on, traders should consider two scenarios. The first, more likely one, is a deepening correction, as, despite the drop, prices still pretty overheated. Often support for the buyers in rising markets comes only after the 38.2% pullback. For Brent, that level is at $57.8. However, buyers might not come until the dip to $55, the consolidation area of the second half of January. In WTI, the downside targets are $55 and $52.

The second, ultra bullish and much less likely scenario, suggests that Oil buyers will use yesterday’s drawdown to ramp up purchases, quickly moving prices up $7 from current levels, updating local highs and targets higher to $85 for Brent and $76 for WTI.

The FxPro Analyst Team