A $66 slump could follow oil’s ironic rebound

August 12, 2022 @ 12:51 +03:00

WTI crude has gained more than 6.5% this week, and this strengthening has a pinch of irony.

Stock indices managed to surpass the highs of the previous week’s pullback and the weak inflation report’s main driver of increased risk appetite.

A sharp slowdown in price growth and a reduction in the fuel component fuelled speculation that the Fed would slow policy tightening. But oil is a risky asset, so the rest of the market enjoyed a rise. The implication is that oil rose this week because the economy showed the effects of its decline in the previous two months.

It is also interesting that the reversal of stock indices from decline to rising was only a few days after oil reached its peak.

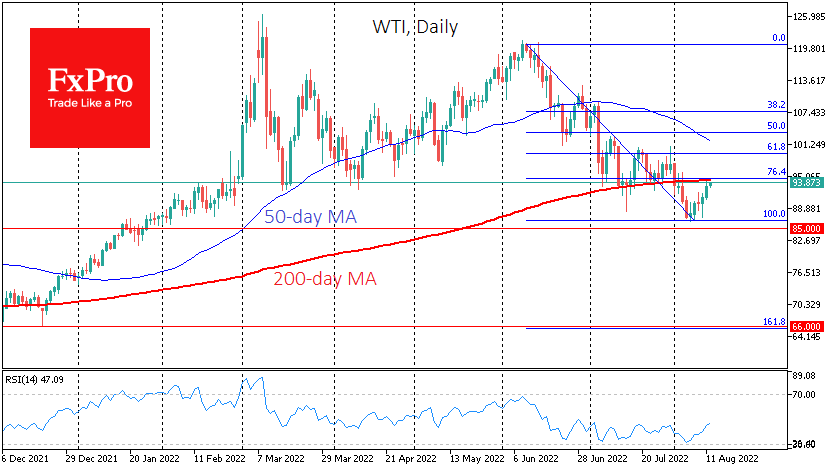

WTI crude oil took the initial setback at the beginning of August and is now testing its 200-day MA, a significant long-term trend line, from the downside. We considered the dip below it on the first day of August as an additional confirmation of the trend reversal to bearish.

However, we would venture to guess that under macroeconomic pressure, the current rebound in oil is a short-term correction after oversold conditions and that the primary trend of the last two months will remain predominant.

The latest weekly estimates have marked a rise in US oil production to 12.2 million BPD – a new high since April 2020 and a return to a rising trend. Besides, recently, the IEA and OPEC revised their forecasts to a less profound fall in Russian crude production, with cartel output rising. A small production surplus over consumption is forecast, adding pressure on prices.

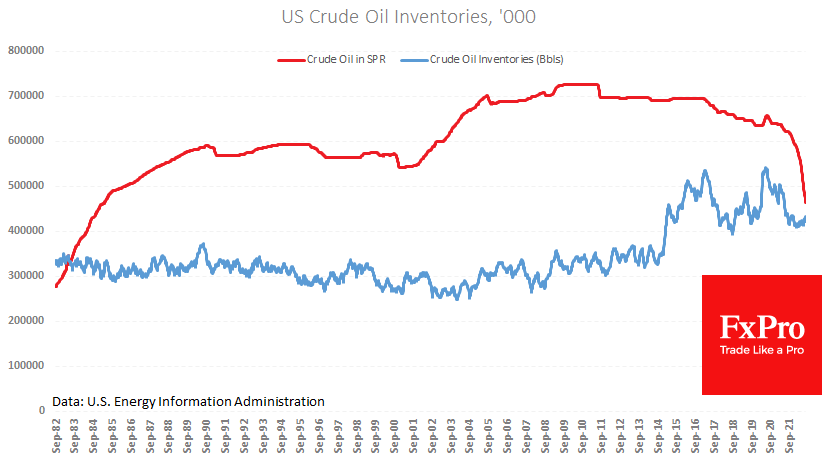

Meanwhile, the US continues to sell off strategic stocks, despite stabilisation and a moderate increase in commercial inventories. US policymakers are now focused on bringing the price of oil down as much as possible and are not prepared to stop. The intention to return to restocking only in 2023 works to encourage US companies to invest in production, as the government will have an increased demand for their raw materials in the future.

In addition, we note that the monetary policy tightening that has taken place over the past few months around the world is only beginning to work to slow demand.

The world could find itself in a stagnant or falling demand situation with continued production growth in addition to the surplus production already in the market and the sell-off from reserves.

The price rally of the past week fits into a corrective rebound picture. If the bulls do not find a new fundamental reason to buy at current levels near $94 for WTI in the next few days, we should expect a bear market recovery.

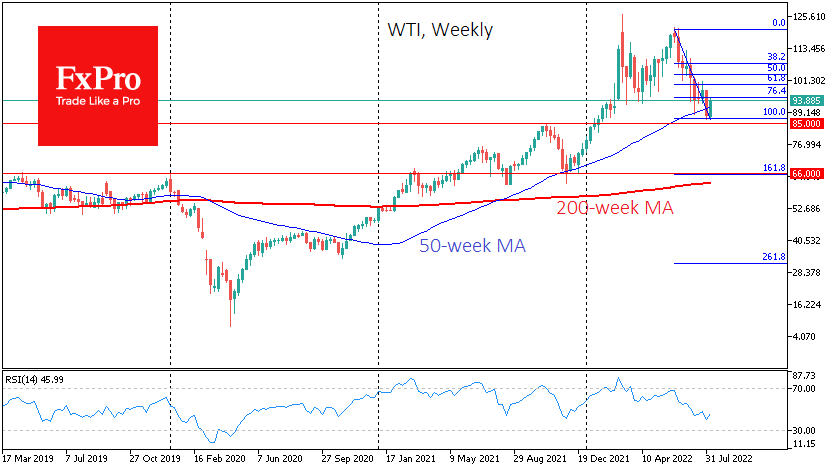

Short-term downside targets include the October 2021 highs near $85, which the price almost missed last week. A decisive move below that level would make the $66 target relevant. It includes 161.8% of the anti-rally of the past two months, the November and August retracement lows of last year, and the 2019-2020 highs.

The FxPro Analyst Team