August 15, 2018 @ 12:42 +03:00

The strengthening of financial markets on Tuesday has not been unsustainable and prolonged. Recent shots in the U.S. trade conflicts are: a China’s claim to the WTO about US tariffs on renewable energy imports and subsidies to their own producers; Turkey has put obstruction duties on a number of goods from the United States, including passenger cars, and has announced a boycott of American electronics.

On Wednesday morning, the markets are again under pressure on new episodes of U.S. trade conflicts. Again, at the epicentre of the fall are the Asian exchanges as MSCI lost 0.8% and Hong Kong’s Hang Seng fell by 1%.

At the same time, we saw almost an uninterrupted demand for dollars in the currency market. Despite yesterday’s rollback at the stock exchanges, the U.S. currency continued to strengthen its main competitors. The dollar index added 0.4% on Tuesday, and continues strengthening on Wednesday morning adding another 0.1% and trading at the level of 14-month highs.

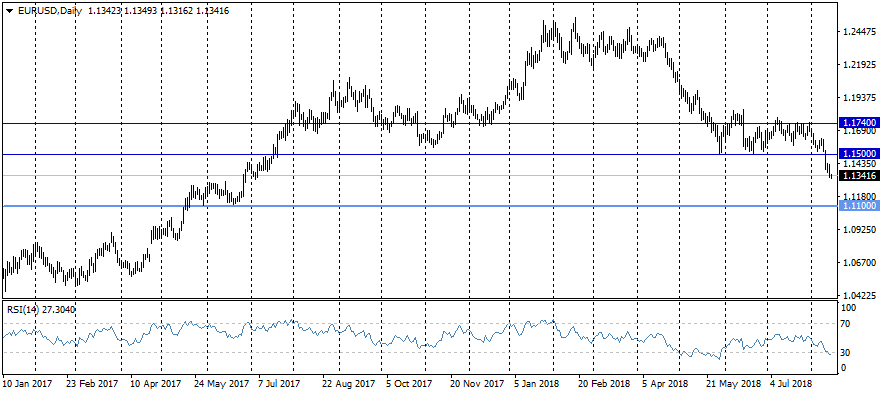

EURUSD sank to 1.1320 in the morning, having lost more than 2.5% over the past week when the pair traded above 1.1600. The sales in pairs intensified after the exit from the trading range since May on fears around the stability of the eurozone banking sector against the backdrop of Turkey’s problems. Cravings in dollars can be saved for the next few days against the wave of stop-orders. The goals of bears in EURUSD pair in the course of the current impulse decline may become 1.1150, the levels of previous local lows. The longer-term targets for the next months could become the levels around 1.04, at which the pair had traded in early 2017.

Sterling also continues its falling, dropping to 1.2700 on Wednesday morning. Here the nearest local lows are the levels of 1.2630, the capture of which opens the way to 1.21 – to the global lows after Brexit.

The gold is keeping its way down. In the morning, it rewrote the lows of January 2017, dropping to $1186 per ounce. Amid the growth of the dollar and the fears of problems in key consumer markets for this metal (China, Turkey), the gold has yet sought support unsuccessfully.

Since the situation with trade and diplomatic conflicts between the United States and other countries is far from being resolved and is only gaining momentum, the craving for dollars can also be intensified. Perhaps, the most significant risk for the dollar may be another verbal intervention of Trump against the strengthening of the dollar. It is impossible to exclude changes in the rhetoric of the Fed policymakers. In previous years, weakening in the foreign markets forced FOMC under chair Yellen to review its plans for the tightening the policy. We have to see if the Fed’s views would be reconsidered under Powell’s administration.