BankPro Weekly: It’s not so scary anymore

April 13, 2026 @ 16:36 +03:00

Week in review

The Middle East conflict remains the main driver of the market, forcing traders and investors to focus on headlines rather than macroeconomic factors.

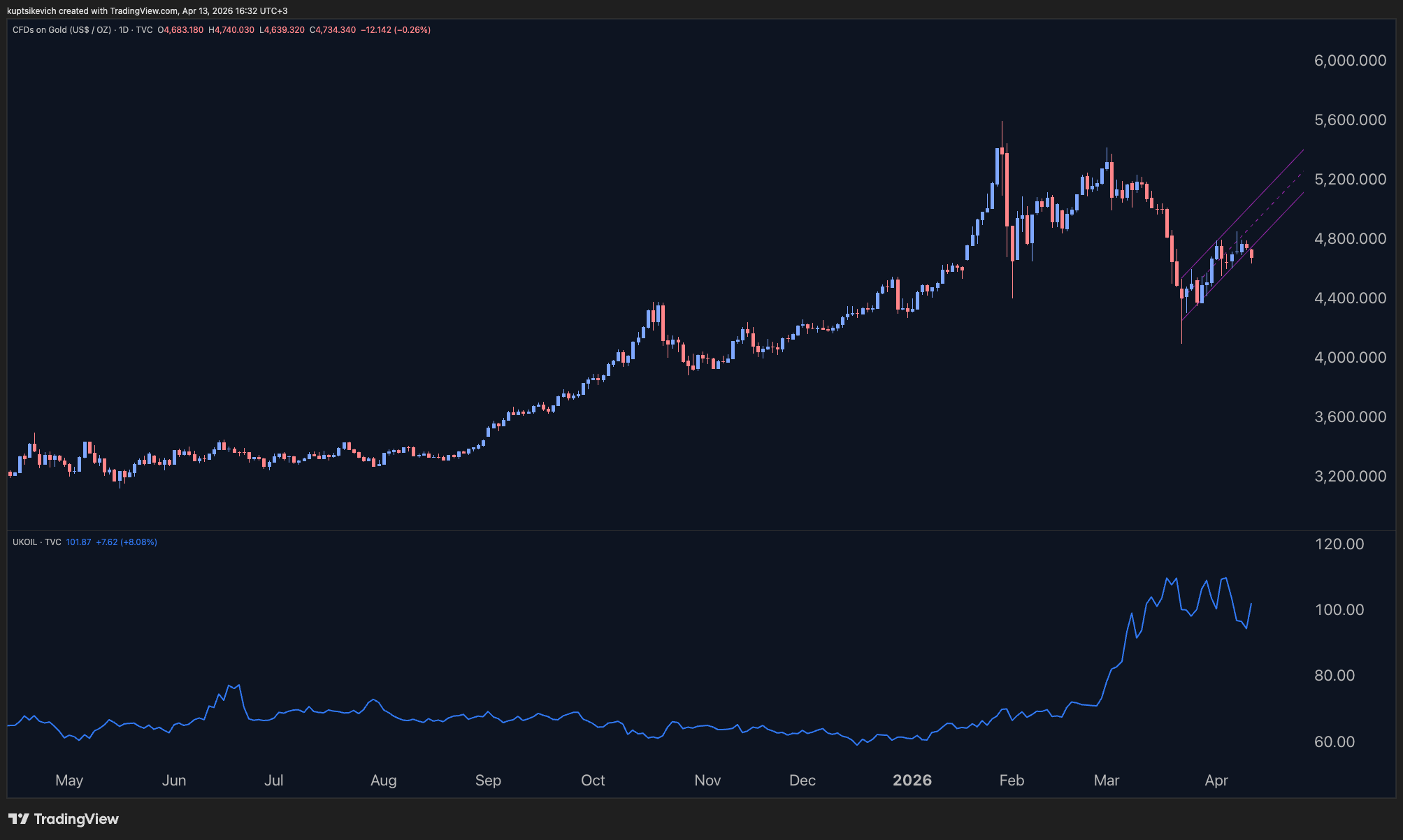

Trump’s promised blockade of Iranian ships in the Strait of Hormuz pushed oil up by around 7% at the start of trading on Monday, but this recouped only half of the previous week’s losses, leaving Brent below $100. Blocking the Strait, or (more likely) Iranian ports, looks like a step towards de-escalation after the peak of threats to destroy the nation. This shift towards a more protracted conflict, though, may conceal regrouping and preparation for a new wave.

Gold is slowing its rise, threatening the recovery trend of the last three weeks, after falling to $4,635 early on Monday. We continue to see a bearish outlook for the metal whilst the price remains below $4,900.

Geopolitically driven corrections in US indices tend to be short-lived – lasting just 15 trading sessions. This time, the decline lasted longer – 21 sessions – but a reversal was already evident by the end of March.

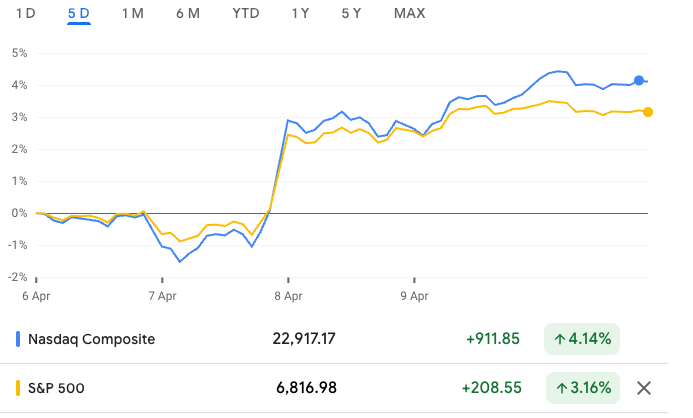

The S&P 500 gained over 3.1% last week and has risen by more than 8.5% from its lows on 31 March. The Nasdaq 100 added 4.1% over the past week and has risen by more than 10% from its recent lows.

Sentiment

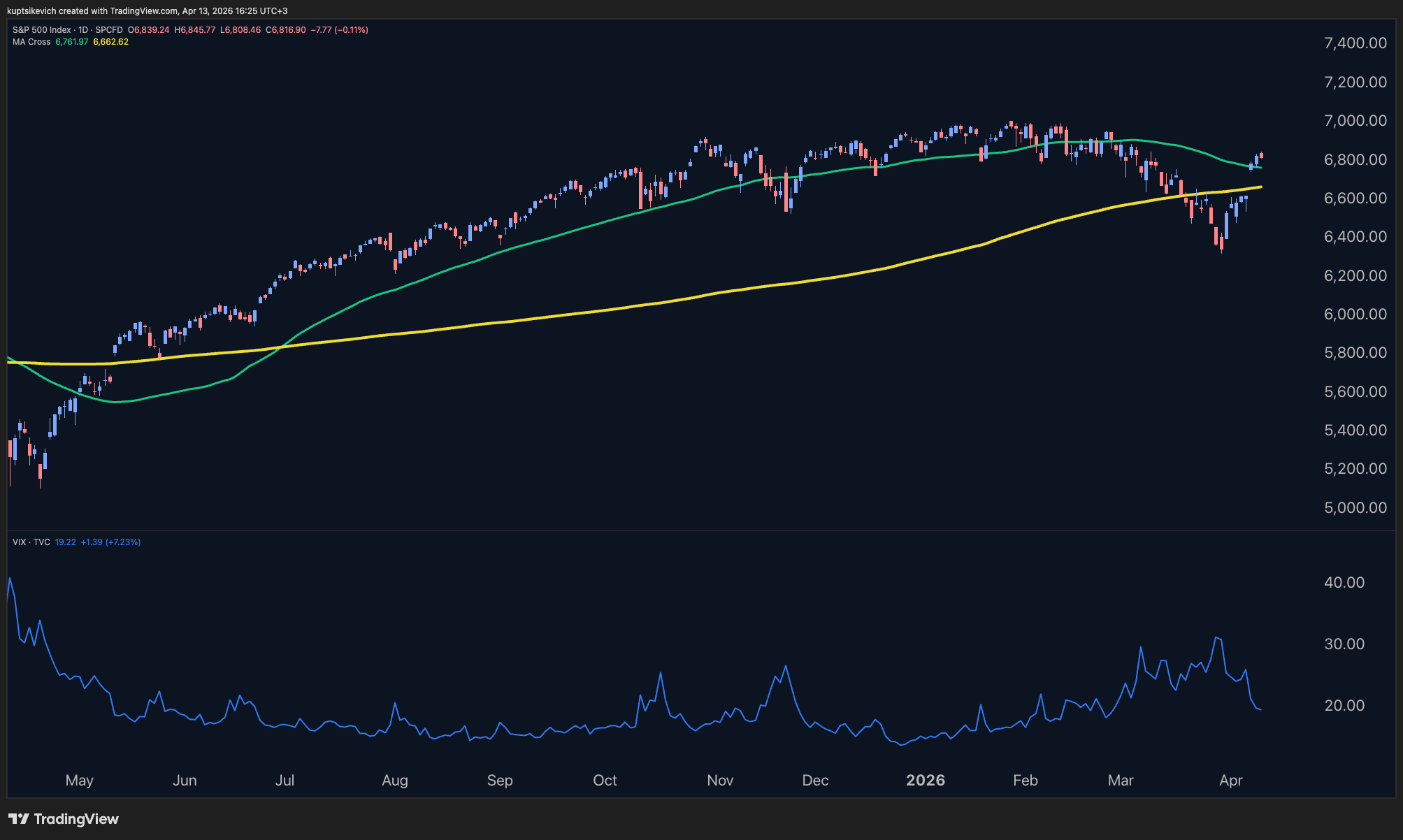

The volatility index – the VIX – fell from 25.15 to 21.4, though it remains above the historical average of 19.5. The Composite Fear and Greed Index rose from 22 (extreme fear) to 38 (fear) – a highly symbolic high since 27 February.

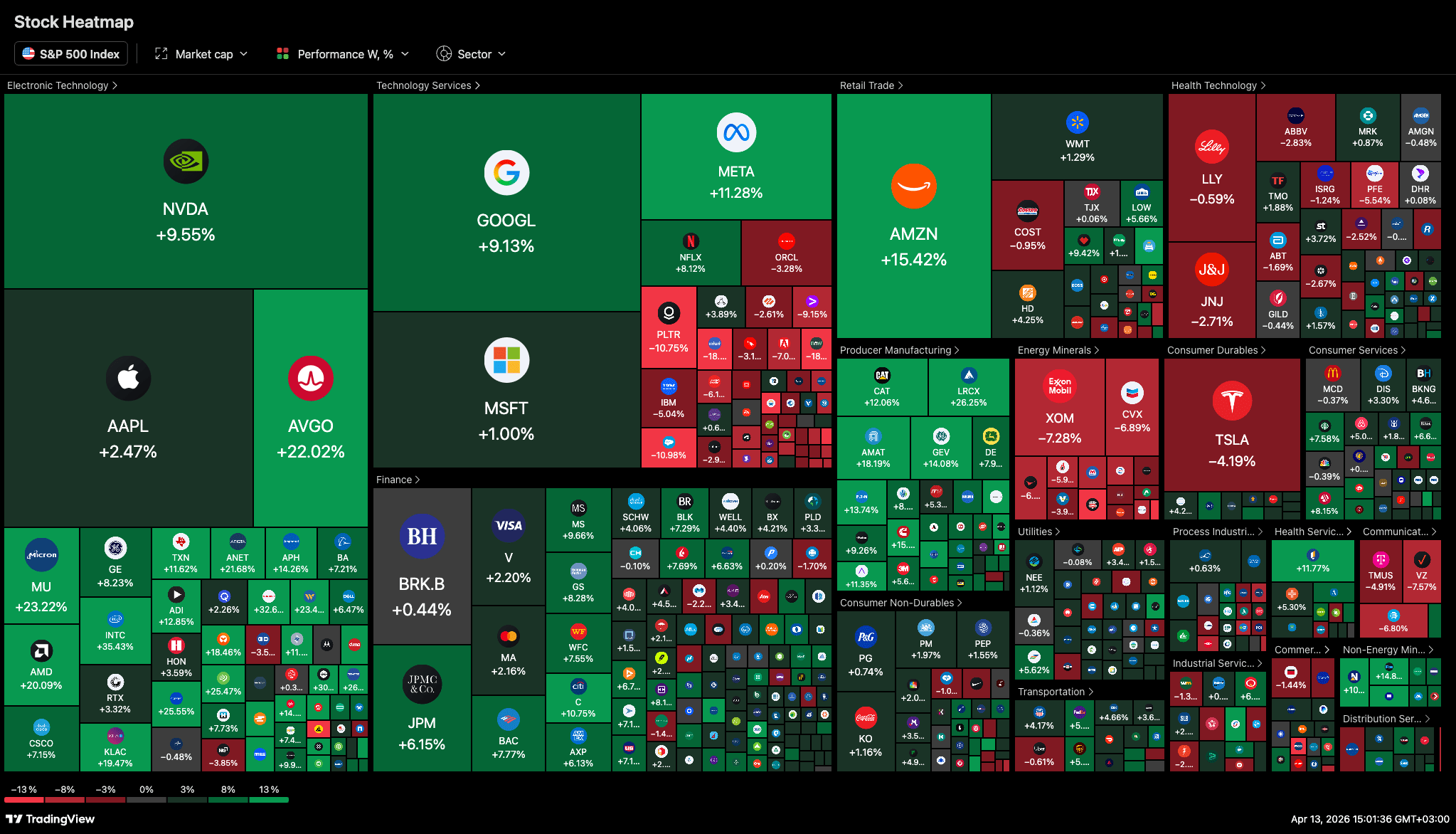

The most significant move came on 8 April, when the index gained 2.3%, closing above the 200- and 50-day moving averages, further confirming a return to a growth phase, with big tech stocks acting as key drivers. Maintaining this pace suggests new highs could be reached as early as this week, with the index consolidating above the psychologically important 7,000 level.

This week, the major banks and financial firms are kicking off the latest earnings season. The market’s reaction to the news will help gauge global risk appetite: will investors ignore the negative implications, or will they pay closer attention to them? Separately, energy exporters may once again attract buyers on news of tankers heading towards the US to purchase oil. America has plenty to sell, given the rise in crude oil stocks over the last seven weeks, and there are buyers, given the blockage of the Strait of Hormuz.

Key figures

The US Consumer Price Index rose 0.9% m/m and 3.3% y/y overall, and 0.2% m/m and 2.6% y/y for the core index – slightly below average forecasts. US oil inventories rose by 3 million barrels over the past week and by 44.9 million barrels over seven weeks of growth. In China, consumer inflation slowed to 1.0% y/y in March, while producer prices rose 0.5% after a 0.9% decline. This marks the first increase after 40 months of deflation.

The most influential upcoming economic indicators include US producer prices (expected to rise 1.2% m/m and 4.7% y/y), China’s quarterly GDP growth (expected at 4.8% y/y), and the UK’s monthly GDP (forecast at +0.1% m/m).