BankPro Weekly: It’s harder to grow at that altitude

April 24, 2026 @ 19:03 +03:00

Week in review

The Middle East conflict is far from over, but it has been overshadowed by a flood of contradictory statements and signals, leading traders to rely on the more solid ground of fundamental data and corporate earnings reports. The main traditional risk barometers, Brent crude and gold, are moving in opposite directions. Gold has lost its recovery momentum since the end of March, falling by 2.5% over the past week. At the same time, a broad downward trend is taking shape as signals from major central banks become increasingly hawkish. Oil prices are hovering around $100. This is a painful level for the global economy, but positive signals from policymakers are preventing equities from focusing on the negative.

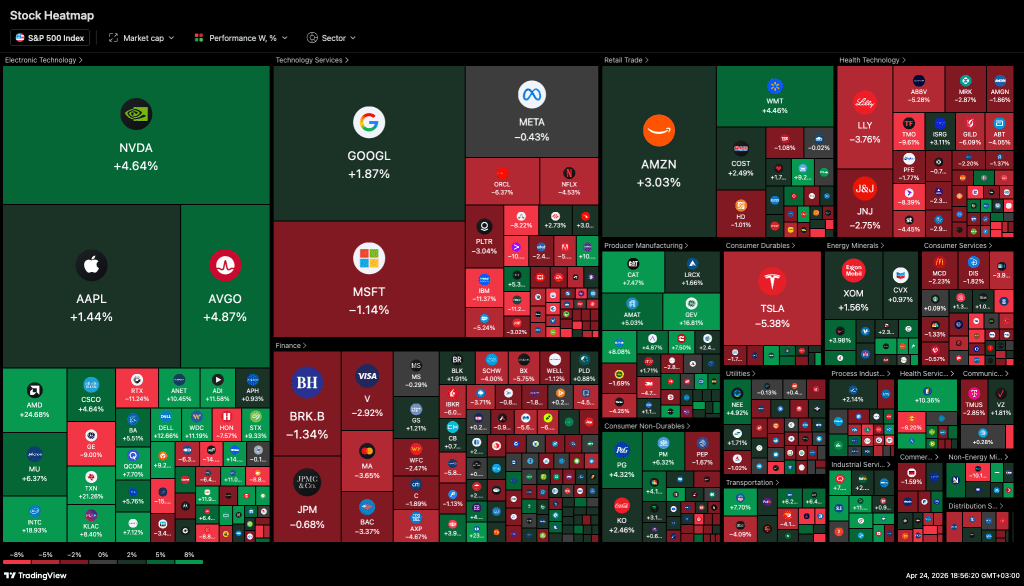

The three-week rally that began in early April lost momentum sharply immediately after the S&P 500 and Nasdaq 100 reached record highs in the middle of the month. The S&P 500 has barely managed to end the week in positive territory, gaining 0.2%, whilst the tech-heavy Nasdaq has extended its lead, rising by 1.8%. Despite the recent slowdown, the strong growth momentum of the past three weeks – during which the indices gained more than 3% each – points to a very bullish outlook for the year ahead. By and large, the March slump in equities has increased their appeal, and the geopolitical nature of the sell-off has not undermined companies’ fundamentals. All this is reflected in investors’ reaction to corporate earnings reports, which have shown a predominantly positive trend.

Sentiment

The volatility index, currently at 18.6, has declined gradually over the course of the week but remains above the 17.5 level seen a week earlier, when optimism regarding Iran reached its local peak. Since then, uncertainty has increased, but the markets seem to be learning to live with it. Moreover, although fear index readings are relatively high, they have settled below the informal signal line of 20. The Fear and Greed Index has predictably shifted into greed territory, reaching 67 by the end of the week, after previously peaking at 70. Among the components, only one calls for caution: price strength, with a rather tentative lead in the number of shares setting new yearly highs.

Key Figures

Retail sales in the US jumped by 1.7% in March as consumers sought to keep pace with inflation. Business activity is also picking up, as is the index of pending home sales. In these circumstances, it is difficult to bet against the stock market in the coming days. A hangover and the realisation of an economic slowdown may well be just around the corner. But for now, this is only an issue for Europe, which is scaling back activity in the face of high fuel prices, whilst the US is trying to make the most of the situation before the real hit to spending. Which, incidentally, may not even happen.

Watch This Week

Interest rate decisions in Japan, Canada, the US, the UK, and the eurozone – only a shift in the tone of the statements is expected, not a change in the actual rates. A synchronised shift could prove a major event for markets for many weeks to come.

US GDP 1Q26 Advance estimate – the release with the greatest potential for volatility in equity indices.