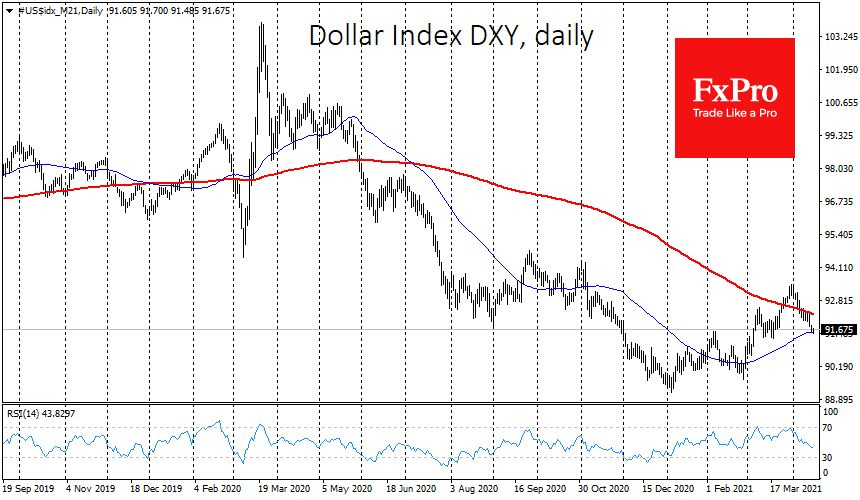

The Dollar has fallen to a 4-week low, settling at the 50-day moving average. The US currency pressure remains intact mainly due to the soft tone of the Fed’s Powell comments.

The Fed chief tried to reassure the markets that monetary tightening will not occur until much later, but investors have already factored this into the current price levels. Powell noted that the Fed is unlikely to start raising rates before 2023. These comments almost nullified expectations of a rate hike before the end of the year. However, the chances of a rate hike had previously exceeded 10% last week.

That said, fuelled by colossal stimulus, the US economy is on course for the sharpest growth in modern history. No doubt, it now looks like a V-shaped recovery. Powell says that the states are entering a period of accelerated growth.

It costs America a record budget deficit with a debt-to-GDP ratio of more than 100%. However, Powell urges the public not to worry about that now. Coming from the head of the most stable purchaser of US government debt over the past year, this sounds like a hint of QE.

The Fed notes that it has no plans to sell its Treasuries on the market, which shifts the balance of power in favour of debt buyers. Therefore it is not surprising that long-term bond yields continue to retreat from their late March peaks.

The Fed is also calling for less worry about inflation, nodding that the average growth rate over the last 25 years has been below the 2% target. It may be the intention to bring the value up to 2% in the longer term. This suggests a tolerance for very high inflation for years to come, not just for the coming months when the numbers will rise due to the low base of last year.

In a nutshell, the Fed’s comments provided simultaneous support for debt and equity markets and outlined an outstanding growth outlook for the US economy. The price to pay for this seems to be a weakening of the Dollar.

Abundant liquidity and an accelerating economy will lead to goods and services being bought with dollars, and value will decline. This is already evident in the booming stock markets and record trade deficits.

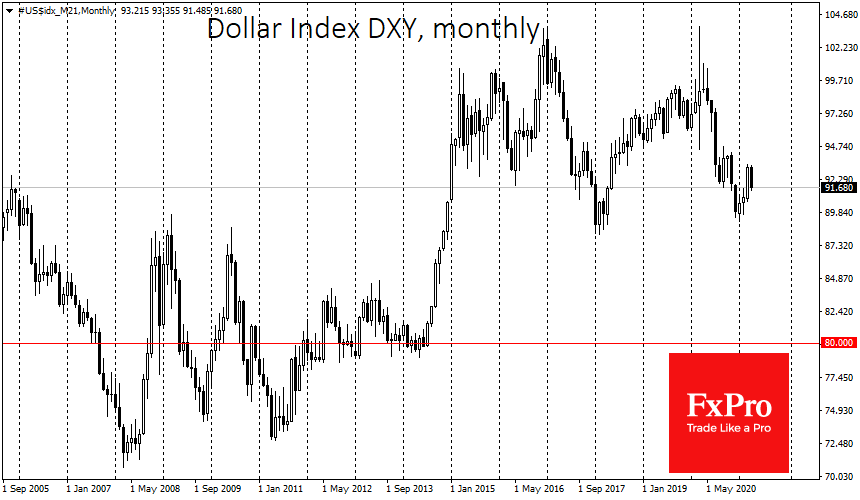

From a historical perspective, there is considerable room for a decline under the Dollar. Almost a year ago, the DXY began its descent from the peaks from 2003. A fall of 10% would take the index back to average levels from 2005 to 2014. Nevertheless, this fall is unlikely to threaten the Dollar’s reputation as a reserve currency. This seems like a small price to pay for the chance to regain the glories of the world’s leading economy. A nice bonus is the increased competitiveness of US exports.

The FxPro Analyst Team