The markets managed to return to growth thanks to the Fed’s announcement to start buying corporate bonds (previously, only ETFs). At the beginning of the program, the central bank made deals on higher volumes, and then gradually reduced them. Thus, the first phase of the new programs supported the growth of markets to the greatest extent and then its influence gradually weakened. Probably, for this reason, yesterday the American market managed to make a U-turn, not only offset 2% of losses during the day but also ending the session with a growth of 0.8% on the S&P 500.

These trends affected the demand for the dollar. The American currency returned to decline on Monday after two days of rebound. At the same time, investors cannot stop wondering what will happen next with the dollar and the U.S. economy, which is overloaded with debt.

First of all, it comes to mind that the U.S. will release the “genie” of inflation from the bottle. The Fed will deliberately lag behind the normalisation of policy, even if the target price growth rate is restored. It is assumed that accelerated growth will reduce debt in real terms. The main thing is to achieve stability in the bond market to prevent uncontrolled growth in the cost of servicing government debt.

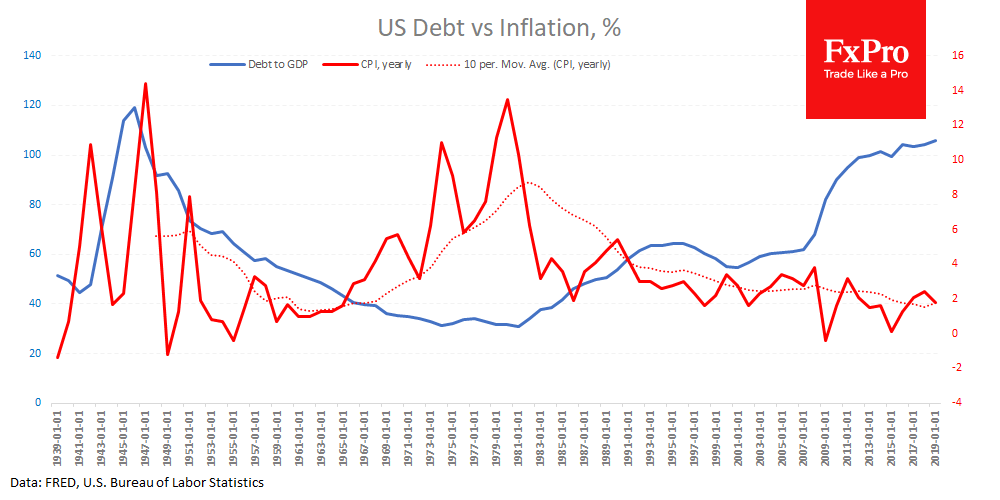

However, it’s not all as easy as it sounds. It is enough to look at available data on the level of government debt to GDP since 1939. These figures show that inflation hikes subsequently increase the debt burden. Worse, prices get out of control during periods of relatively low debt pressure, and not vice versa. For more than 80 years, the correlation between inflation and government debt to GDP is -0.29%. This reflects a weak negative correlation between indicators. That is, there is no sense for investors in the coming quarters to fear that politicians will activate the inflationary spiral. On the contrary, a high debt burden will suppress price growth, which can be seen both by the U.S.A. itself in the early postwar years and by the example of Japan.

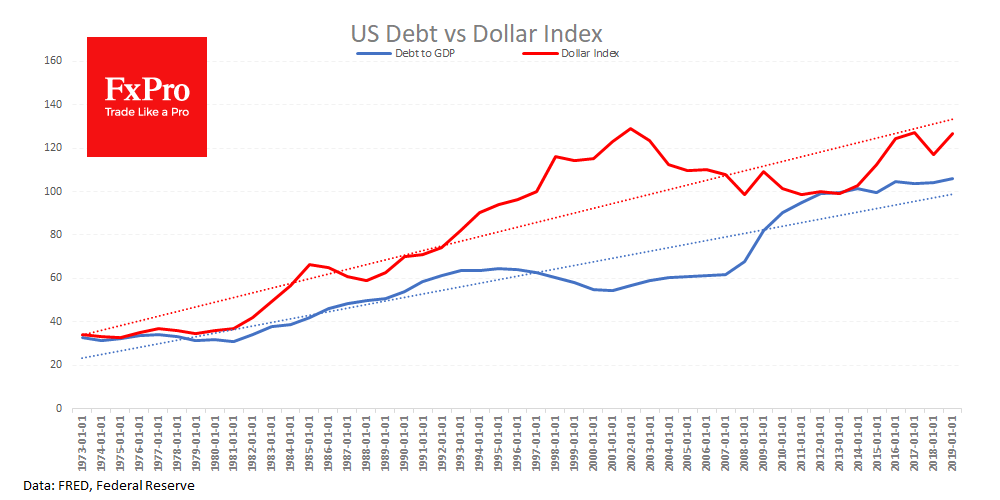

No less impressive is another correlation between the level of public debt and the dollar index. For the whole period of calculation, from the 1970s to the end of 2019, the dollar index, compared with a broad basket of currencies tends to grow, as well as the level of public debt to GDP. The exception was observed only from 1996 to 2007. However, this did not affect the overall apparent trend. Despite the growth of American external debt, the dollar index tends to strengthen against a basket of world currencies, in which one currency or another is regularly devalued.

The FxPro Analyst Team