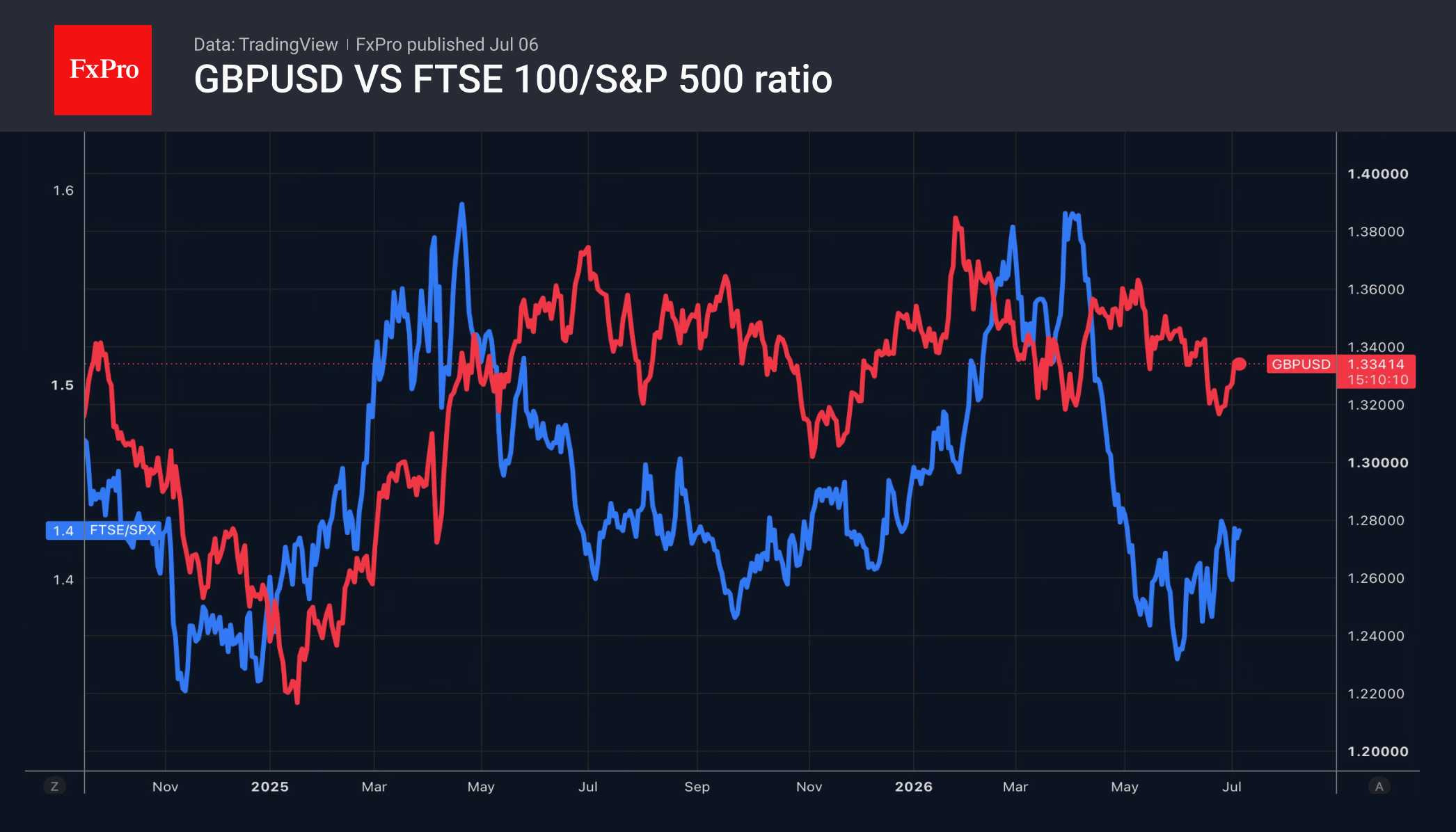

- The stabilisation of the political situation in Britain is driving the GBPUSD rally.

- Traders are wondering: Were there currency interventions in Japan? Or is fear to blame?

The US dollar managed to recover towards the end of its worst week since April, as US equity markets closed ahead of Independence Day. Investors continue to reassess the likelihood of the Fed tightening monetary policy and are preparing to analyse the minutes of the June FOMC meeting. It will be more difficult to identify divisions within the Committee this time round due to the document’s reduced length. Concision is Kevin Warsh’s hallmark.

The greenback’s retreat has given other currencies a chance to shine. The pound has posted its best performance in the last 12 weeks against the backdrop of a stabilising political situation in Britain. In the run-up to his appointment, the incoming Prime Minister, Andy Burnham, is set to adhere to existing fiscal requirements, which reduces the risk premium demanded by investors and boosts demand for domestic assets.

The yen has strengthened at its fastest pace since the currency interventions at the turn of April and May. This has led traders to wonder whether Japan intervened or if speculators were so frightened that they began unwinding their long positions in USDJPY themselves. These positions had reached their highest level since 2017. In such conditions, the triggering of stop-loss orders turns the pair’s decline into an avalanche.

Goldman Sachs has raised its USDJPY forecast from 155 to 165 by mid-2027. The bank believes that the Bank of Japan’s reluctance to tighten monetary policy, high Fed rates and Treasury yields, and the active use of the yen in carry trades will contribute to further weakness in the yen. The 3-month and 6-month forecasts stand at 162 and 163, respectively. US interest rate markets are pricing in a 72% chance that the US dollar will trade at ¥165 by mid next year.

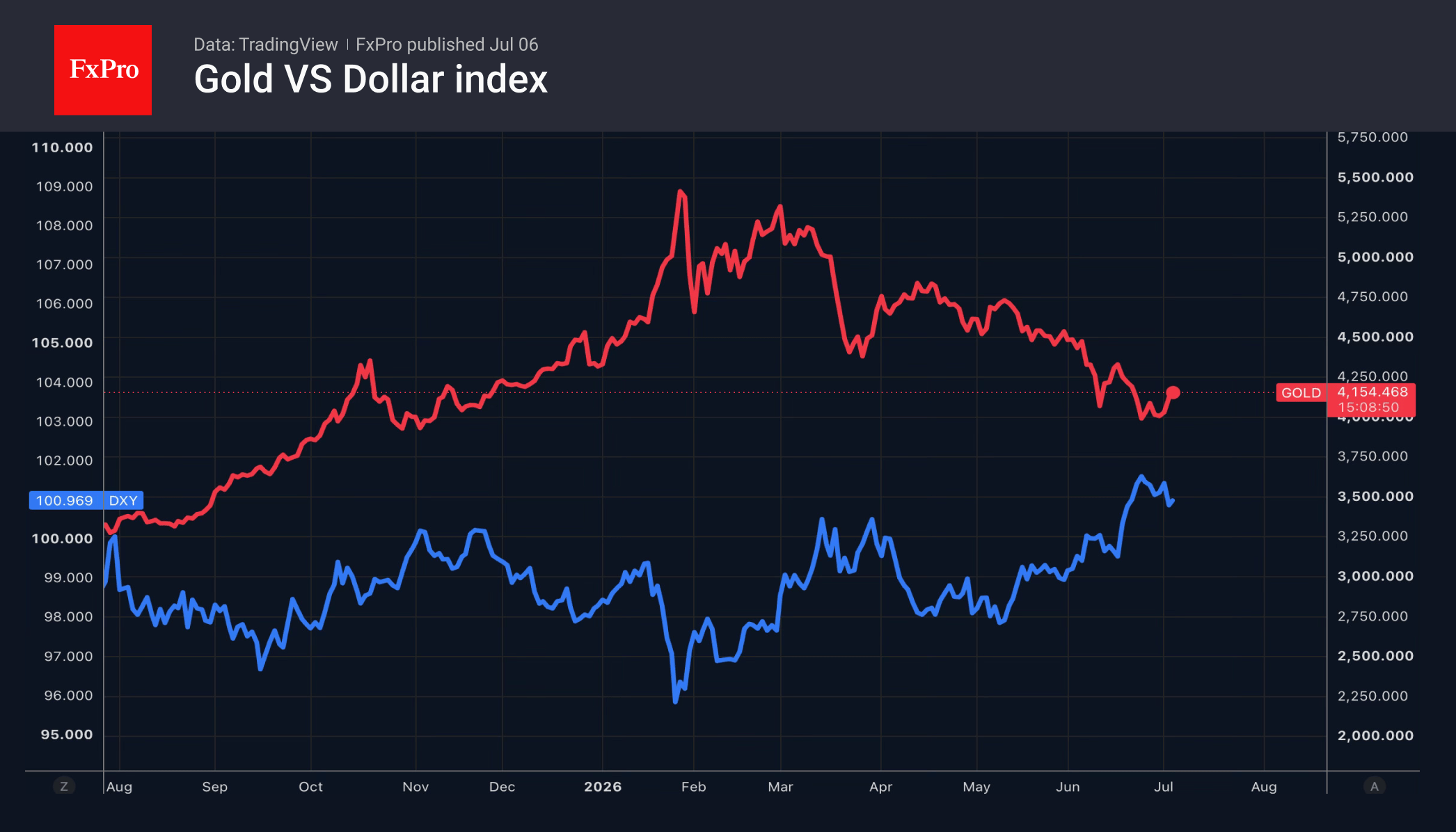

The fall in the USD index and Treasury yields has shifted the balance of power in the gold market. The precious metal briefly returned above $4,200 per ounce but was unable to hold. Bloomberg’s updated forecast suggests that central banks will keep interest rates at high levels for longer than expected due to the delayed impact of the conflict in the Middle East on inflation. Under these circumstances, it will be difficult for Gold to return to the record highs seen at the start of the year.

The FxPro Analyst Team