- Iran insists on control of the Strait of Hormuz and is demanding compensation.

- The US withdrawal from the Middle East could mark the beginning of the end of the petrodollar era.

Rising oil prices, triggered by Iran’s rejection of Donald Trump’s 15-point plan, have sent the EURUSD lower. Tehran does not consider itself to have lost the war and is putting forward its own demands. This does not look like a capitulation by Iran, which means the armed conflict is likely to continue, a development that is positive for the US dollar in the near term.

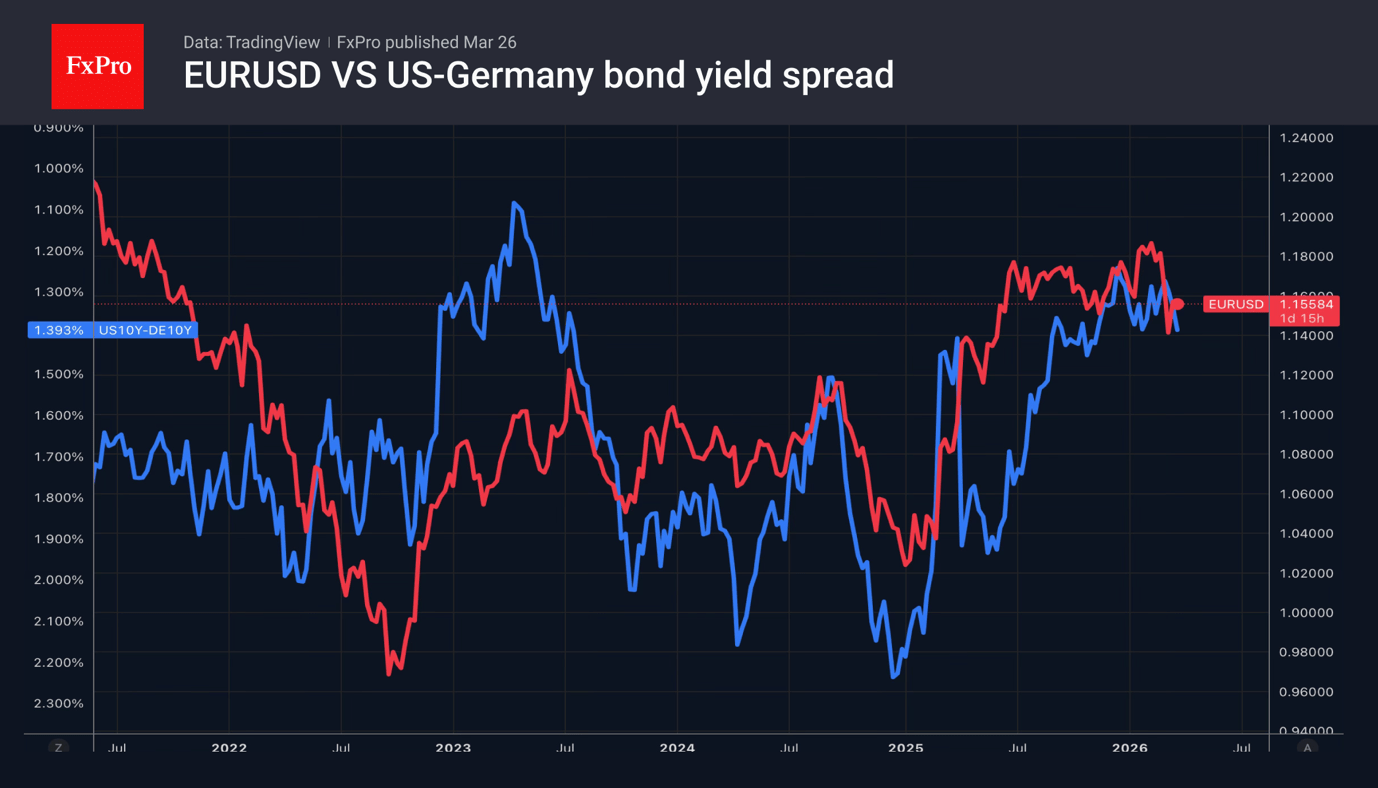

Morgan Stanley describes the USD rally as a bull trap, pointing out that the oil crisis is a temporary phenomenon, whilst divergence in monetary policy always works. The futures market indicates a 64% probability of rates remaining unchanged until the end of the year and a 32% chance of a hike. This is a dramatic shift from the start of the year, when speculators were betting on 2–3 rate cuts by year-end. Nevertheless, the ECB is expected to deliver up to three rate hikes by the end of the year, which should favour the euro against the dollar.

However, it must be understood that without a resolution to the fuel crisis caused by the armed conflict in the Middle East, there is no point in discussing monetary policy divergence. It is by no means certain that the ECB will raise rates, no matter how much Christine Lagarde speaks of determination in the fight against inflation and bringing it back to the 2% target.

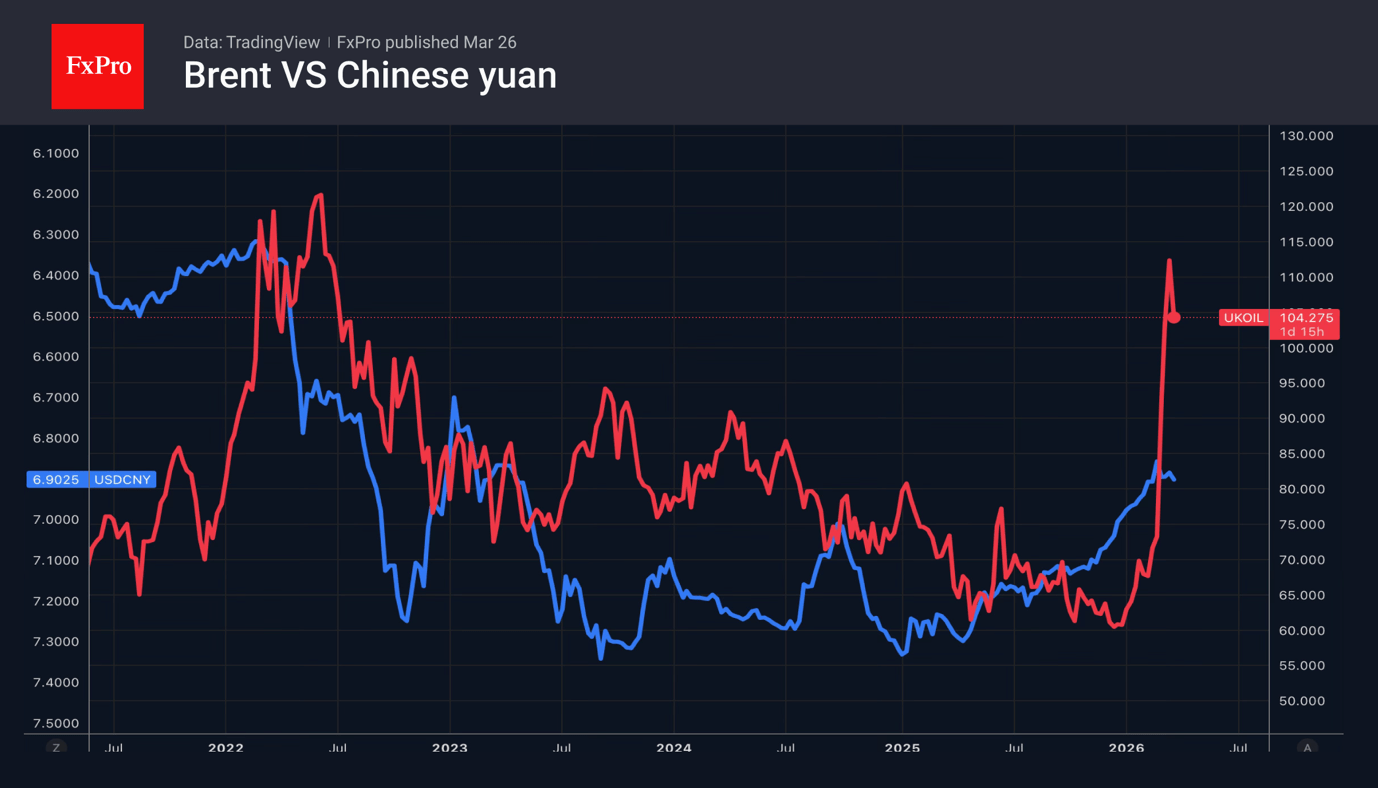

Far from everyone is convinced that the continuation of the conflict will, in the medium to long term, lead to a depreciation of the euro against the dollar. Deutsche Bank believes that a protracted conflict in the Middle East carries the risk of a shift from the petrodollar to the petro-yuan. The concept first emerged in 1974, when Saudi Arabia agreed to sell oil for US dollars and channel its foreign trade surplus into dollar-denominated assets in exchange for US security guarantees. Riyadh now sells four times as many barrels to China as it does to the United States.

Tehran’s continued control of the Strait of Hormuz and the fact that most of Iran’s oil is supplied to China suggest that the transition to the petro-yuan is a matter for the foreseeable future. At the same time, the dollar’s loss of its role as the settlement currency for black gold could undermine its other privileges, particularly its status as the primary reserve asset.

The FxPro Analyst Team