- The global economy is heading towards 1970s-style stagflation.

- EURUSD depends on US-Iran talks.

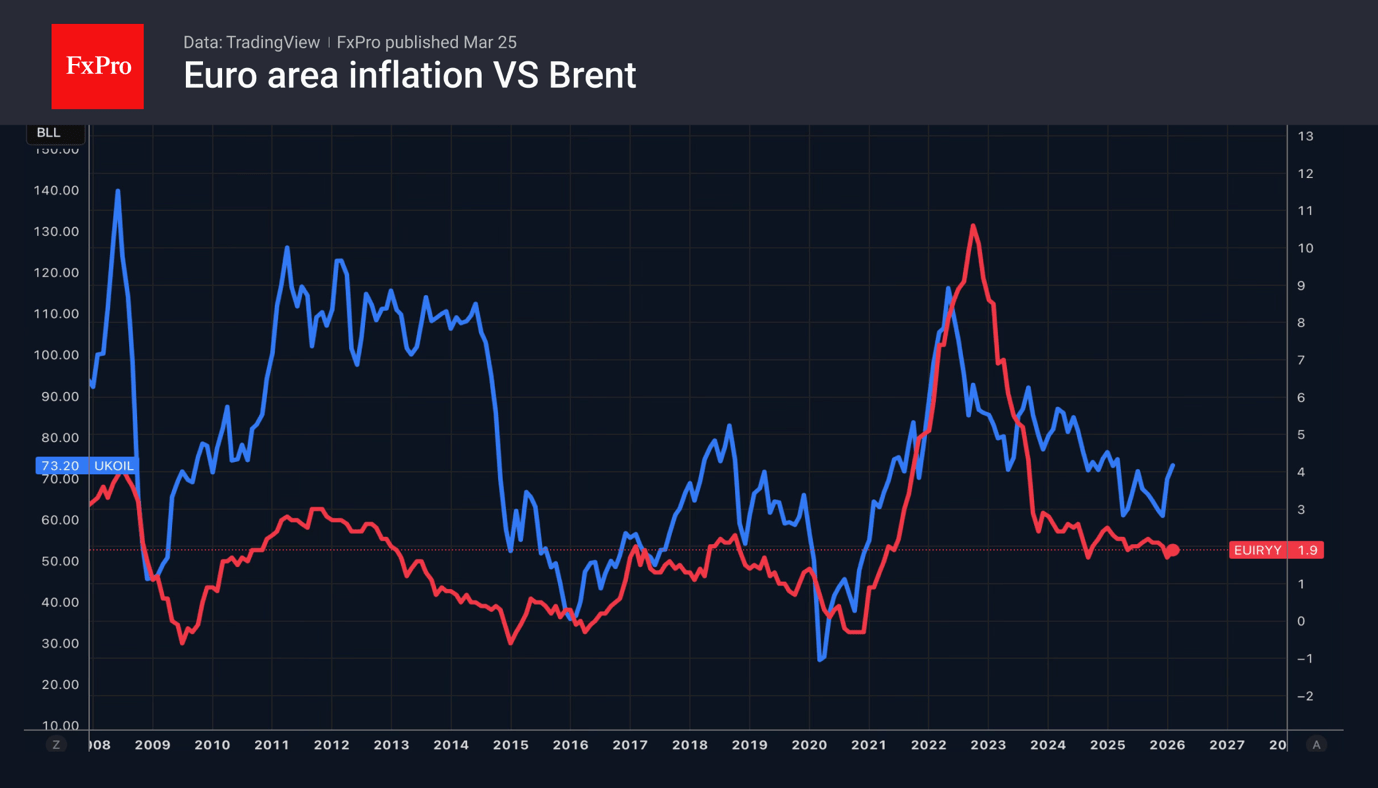

The world is moving towards stagflation, and the currency market risks repeating the experience of the 1970s. Back then, the oil crisis led to soaring prices and a slowdown in economic growth. The Fed yielded to pressure from the White House and started cutting rates. The result was runaway inflation and a double-dip recession. With Kevin Warsh at the helm of the central bank, this remains a possibility. However, for now, the USD continues to respond to news from the Middle East.

The increase in prices tied to the armed conflict is slowing European and American business activity to its lowest levels since April–May 2025. Purchasing Managers’ Indexes, by contrast, are rising swiftly. These indicate a stagflationary scenario, which is purportedly supporting the US dollar. Goldman Sachs believes the greenback will weaken if investors fear not stagflation but recession, causing capital to flow into the Swiss franc and the Japanese yen.

New talks are fuelling rumours of US-Iran negotiations. Washington has provided Tehran with a list of 15 demands, and Tehran is preparing its own list in reply. Brent is falling, stripping the dollar of the advantage that has propelled its rise in recent weeks, driven by a flight to safe-haven assets and a reassessment of the trade balances of the world’s largest economies.

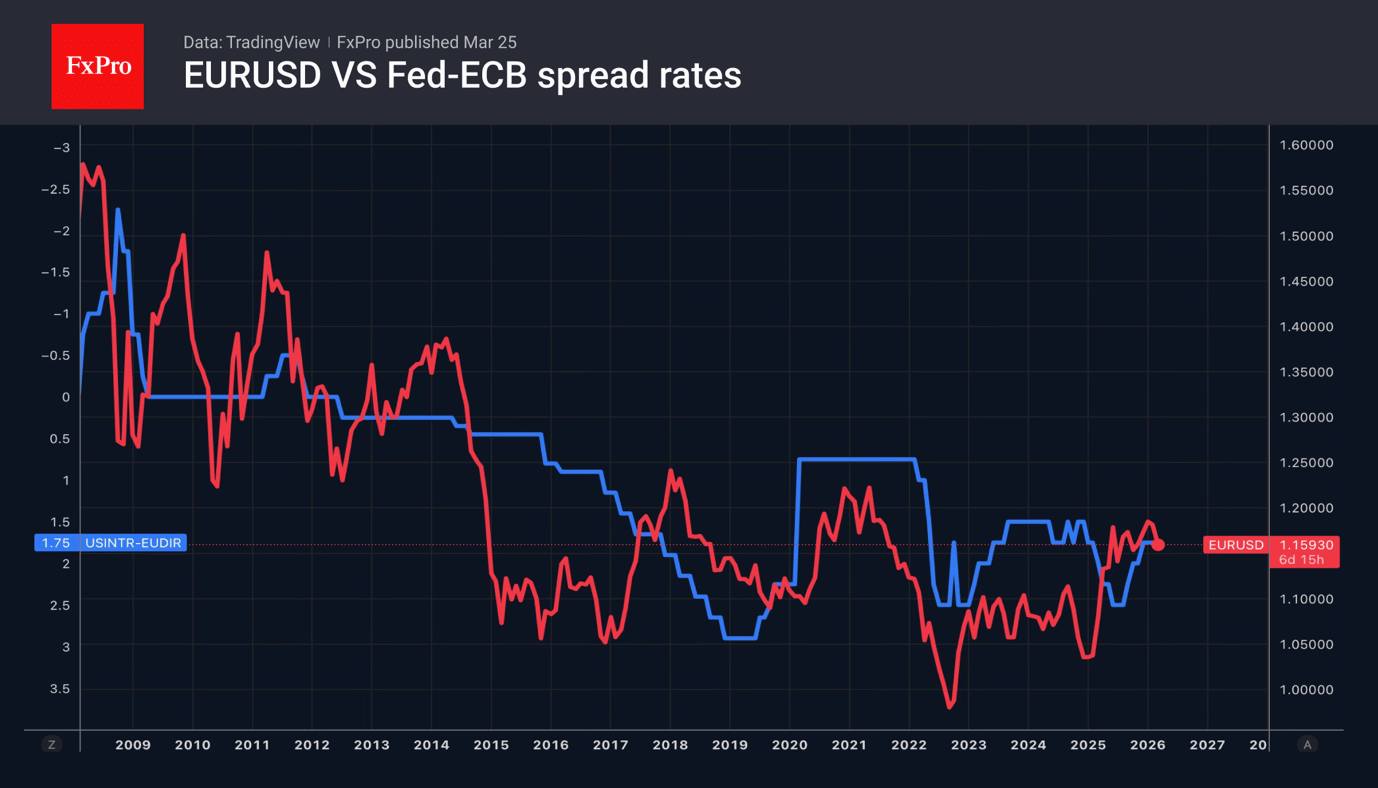

If the talks do indeed take place and are constructive, EURUSD will revert to its main drivers. Primarily, monetary policy. Divergence in this area favours the euro. The futures market anticipates the Fed will keep the federal funds rate on hold until the end of the year, with some chance of a hike. Meanwhile, the ECB can tighten monetary policy two or three times. However, this may not be necessary. If oil prices drop, the inflation spike will be brief.

It is by no means certain that progress will be made in the US-Iran talks, especially in the initial phase, given the parties’ significant differences. Bad news will put pressure on EURUSD, though a collapse is unlikely. Similarly, one should not harbour hopes that Brent prices will return to pre-war levels, regardless of how quickly the Strait of Hormuz is reopened.

The FxPro Analyst Team