Optimism, bordering on jubilation, prevailed in stock markets yesterday, although traders in FX and gold, for the most part, stood aloof from the move.

A sigh of relief washed over in US stocks, causing sharp buying on news that the US government debt ceiling had been raised by 480bn until December, removing the threat of a default by the world’s largest economy. However, by the end of the day, the effect of this news reversed the initial jump. The markets are likely to spend most of today in very tight ranges and low volumes, waiting for US labour market figures for September.

The Chinese bourses, which opened after a week-long holiday, are enjoying an influx of buyers on reduced fears of a domino effect from the Evergrande default.

In addition, Chinese business activity data were also bullish, marking a return to expansion in services and manufacturing last month after a dip in August. Chinese indexes are gaining about 1% today despite the liquidity squeeze from the PBC – a sign that the market is already seeing an indiscriminate sell-off in Chinese assets as it has been witnessing in previous weeks.

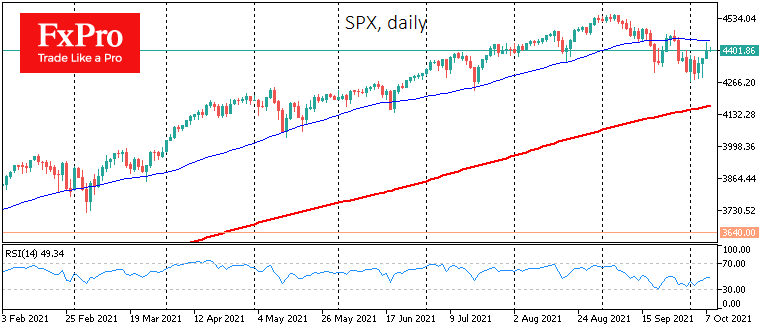

The cautious sentiment in US equity markets, where selling prevailed towards the end of the day, could reflect that the funds prefer the sell-the-growth tactic. The pressure on the S&P500 intensified on the return of the index to its 50-day average. But interestingly, earlier, the European indices (DAX40, FTSE100, and several others) and the Dow Jones found strong buying when they touched the 200-day average. The tug-of-war between bulls and bears is concentrated between these technical levels. Going beyond them could trigger the surrender of one of the sides, causing the start of a powerful trend.

Today’s labour market data has the potential to create such momentum. The US economy is expected to create 490K new jobs in September. If the actual data comes out significantly better than this expectation, it will sharply increase the chances of a QE rollback from the Fed as early as next month.

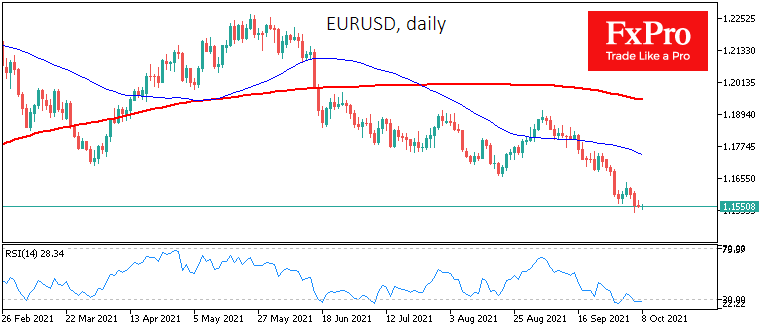

Positive news from the labour market has the potential to give a boost to the dollar, pushing it to renew its one-year highs on the DXY. Despite the notable oversold conditions in EURUSD, in the case of strong NFP, the pressure on the pair could gain new momentum, making a decline to 1.1400 possible as early as next week.

Separately, increasing the government debt ceiling would allow the US Treasury to sharply increase bond auctions, sucking liquidity from the market to normalise its cash reserves, which is positive for the dollar. But together with a reduction in balance sheet purchases from the Fed, this could create a wave of pressure in equity markets.

Thus, strong employment data promises to support dollar buying. The pressure in equities is supported by the failure to rise above the 50-day average in the S&P500.

A weak NFP, on the other hand, could bring pressure on the dollar and support buying shares. In this case, the dollar could quickly reverse to a decline, recapturing the local overbought conditions created by sustained buying since the beginning of September.

The FxPro Analyst Team