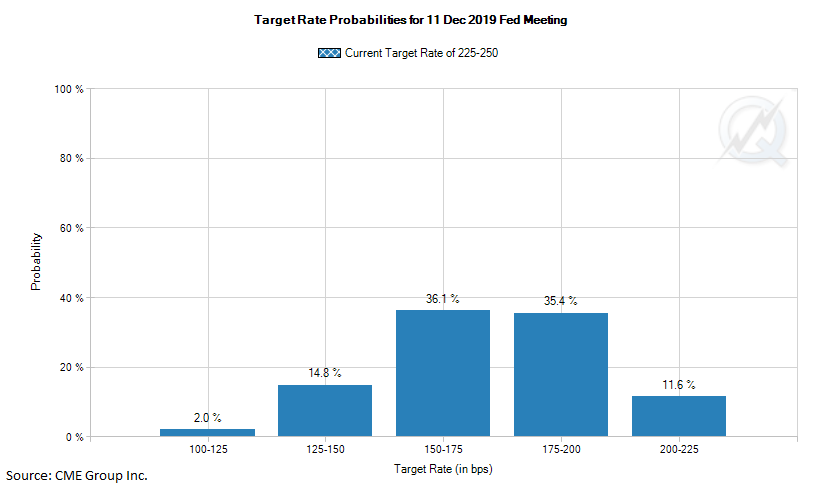

Market attention is focused on the upcoming Fed interest rate decision. A decrease of 25 points is priced in for today’s meeting as well as for the next meeting in September. Few people doubt the rate cut today, so the main attention of the markets will be focused on the comments – whether the Fed is ready to do a further cut as early as at the next meeting. Meanwhile, the most difficult task for the Fed during today’s press conference will be to manage market expectations.

In recent years, there has been a noticeable gap between market expectations and the Fed’s forecasts: the markets are waiting for a much softer policy, while the Fed is setting out a slightly tighter course. The convergence of these polar points of view is the most significant market driver since October last year. The last evidence of this was dynamic over the past week and a half, where the dollar rose on the market’s reassessment of the chances of a 50-points rate cut from a 60% probability to the current 20%.

Consider the possible three options for the Fed and their impact on the markets.

Option 1. Softness If the Fed makes it clear that they are just as cautious about the future as the debt market (rate futures), then this can inspire stock markets to continue to grow, as low rates have a beneficial effect on business activity, fuelling demand. Since such an outcome means a decrease in bond yields, the hunt for yield may begin again in the markets. Such a shift in rhetoric can be bad news for the dollar and could potentially trigger a trend of dollar weakness for many months. This outcome would be a victory for President Trump, but the risk of criticising the Fed’s actions would question its independence. Potentially, this could open the way to a 9% decline in the dollar index to the area of 89 for USDX and 1.23 for EURUSD.

Option 2. More fog The second option (the most likely). Powell may try to leave all the doors open without giving clear signals about the prospects for interest rates, saying that the future interest rate is not predetermined and depends on the state of the global and American economies. In this case, stock markets will remain close to the highs of 98 at USDX and will look for signals from labour market data and trade negotiations process. In this case, for the EURUSD pair, the struggle for 1.10 will remain relevant. The reaction of the foreign exchange market, although it may be harsh in the first minutes after the announcement, is unlikely to contribute to a radical change in the trend for the dollar, leaving it hanging in near two-year highs.

Option 3. Hard approach The Fed could decide to make it clear that a rate cut is a one-time measure, and further easing is not guaranteed. This may be a big surprise for the markets, which will launch a strong wave of dollar growth. In this case, the dollar growth trend may accelerate and send USDX to 103 by the end of the year, and EURUSD to 1.04-1.05. Even more extreme will hint that – in the coming months – the rate may even be raised if the trade negotiations succeed, and in case the latest data does not confirm any cautious policy approaches at the moment.

The FxPro Analyst Team