The Fed has a difficult balancing act. On the one hand, the market should not be allowed to dictate its terms, because low rates are in the interests of the stock market and generally increase economic growth. On the other hand, the reserve system for many years was predictable for markets with its rate policy and QE decisions: only the tone of comments causes volatility. Usually Fed leads markets expectations by its forward guidance but sometimes it seems that markets are trying to wag the dog.

Several times after the global financial crisis, markets went to a steep descent on fears of stimulus winding down. As a result, the Fed gradually adjusted its position, which was very much like blackmail.

Something similar we saw at the end of last year.

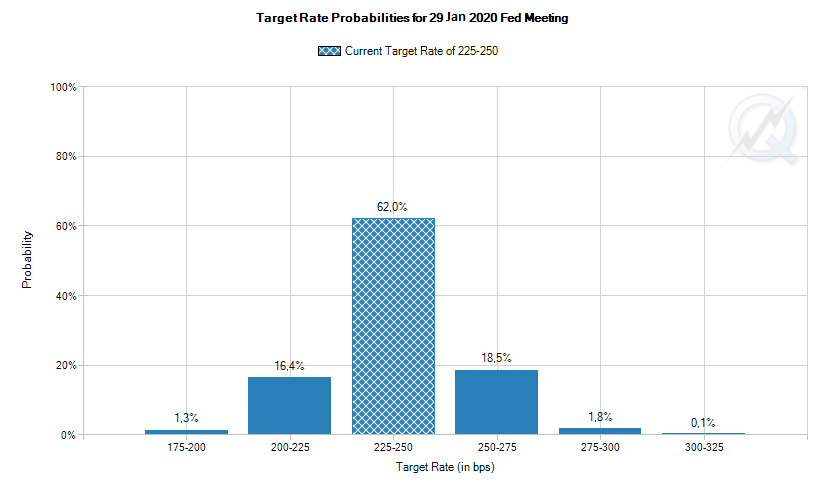

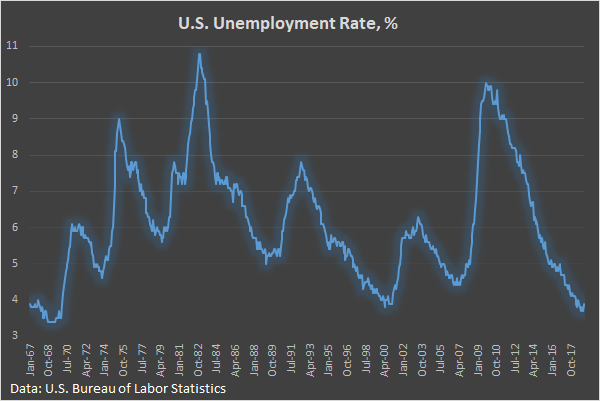

From an economic point of view, it is impossible to believe in the decline in key interest rates this year, although the markets were once priced more than 40% chances of such scenario. Now it is decreased somewhat to 19%. All this against the backdrop of bright national statistics: unemployment rate is at multi-decade lows, wages and spending are growing at a rate that has not been observed for many years. Manufacturing and service sectors has recently registered the perennial growth rates.

It is quite natural, that now we see some slowdown from this side. There is also some impact from intensified fall in prices for raw materials. However, these slowing only return the growth rates to the trend levels, nothing more. We can’t seriously talk about looming recession or even stagnation. Accordingly, there are no objective reasons to cut the Fed’s rates.

The dynamics of the debt market (it indicates the rates decline) should be explained not by forecasts of market participants, but by short-term positioning: at the end of the year, investors were actively withdrawing money from emerging markets, buying short-term papers as “cash”. Due to such high demand, the price rises, i.e. the yield declines.

Right now, the behavior of investors is somewhat discouraging. A year ago, debt markets expected 2-3 increases, and the Fed confidently adhered to a plan for 4 rate hikes. We saw that the economy was strong enough to keep growth above average, despite the tightens.

Again, it is hard to believe that the market forecasts are closer to reality than the expectations of the Fed. Therefore, in near future it is necessary to expect revaluation of expectations, and also some rebound of short-term U.S. bonds yield and, as a result, strengthening of the American currency.

Among the important levels worth paying attention to the area 1.15, which the pair EURUSD cannot pass during the last two months, as the markets pick up the dollar on the dips. If our assumptions are correct, from these marks the dollar is fully able to develop its growth.

Alexander Kuptsikevich, the FxPro analyst