The Fed continued to surprise markets at the start of the year with hawkish rhetoric by unexpectedly raising discussions on balance sheet shrinking. Investors are noticing that the issue has been on the table much earlier than it was before.

In the last episode of QE, it took almost two years from the start of tapering and allowing it to shrink. The pauses between regime switches gave time for the markets and the economy to adjust, and for the Central Bank to evaluate the results of the policy, because the lag between the change in policy and the peak of its impact on the economy often exceeds six months.

In our view, there is a real risk that the markets and the Fed are being too hawkish in their forecasts, moving abruptly from denial of inflation to a willingness to use their entire arsenal at once to beat it.

But such activity to rein in inflation could easily prove excessive. As Friday’s labour market data showed, job growth in the U.S. continues to slow, at only 199K, an 11-month low and half of what was expected. The drop in the unemployment rate to 3.9%, the lowest since the pandemic began, reflects a decline in the number of people looking for work. But it hardly allows us to expect consumer spending to rise, depriving the economy of a crucial pro-inflationary factor.

In addition, fertilizer prices fell at a multi-year record pace last week, container prices have retreated from their peaks, and logistical problems are slowly fading from the agenda.

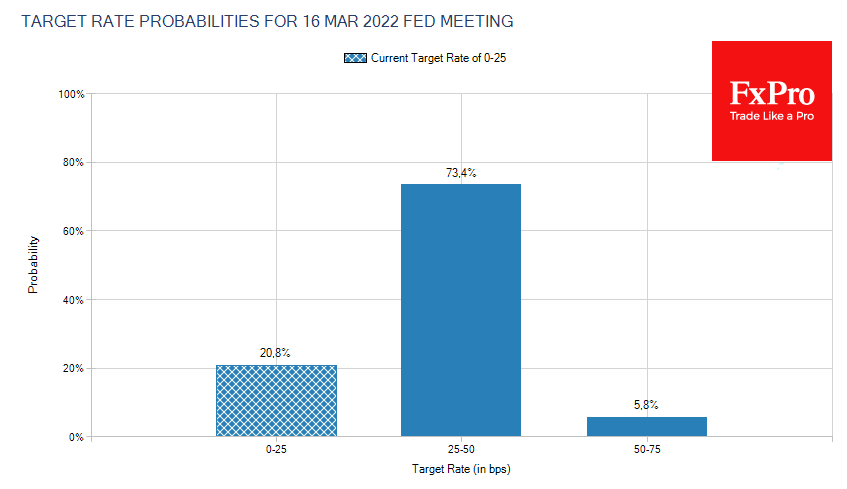

Rate futures are laying down a 70% chance of a Fed rate hike as early as March. Several forecasters also suggest that the rate will rise at each subsequent meeting. But this could come as an excessive shock to the economy, risking causing a recession without putting it firmly on the growth track.

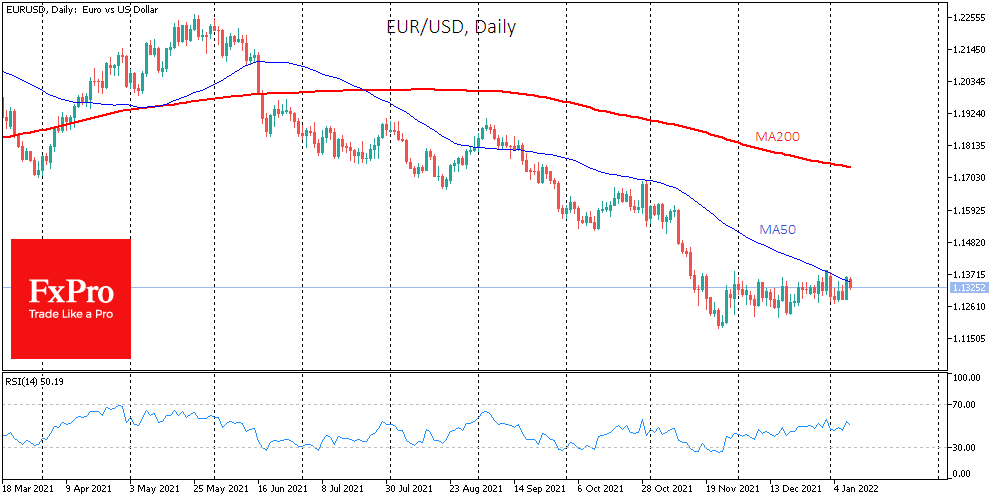

Interestingly, unlike the futures market, the currency market remains in a period of narrow sideways movement of just over 100 pips around 1.1300. It is unlikely that the ECB will act as quickly and decisively as the Fed.

If projections for a rate hike by the latter as early as March and an accelerated move into a balance sheet reduction phase will form a strong upside potential for the dollar.

However, after Friday’s weak data we have a growing belief that the market has jumped ahead in expectations and a reversal of such will start soon, which will play against the dollar and relieve pressure on stocks.

The FxPro Analyst Team