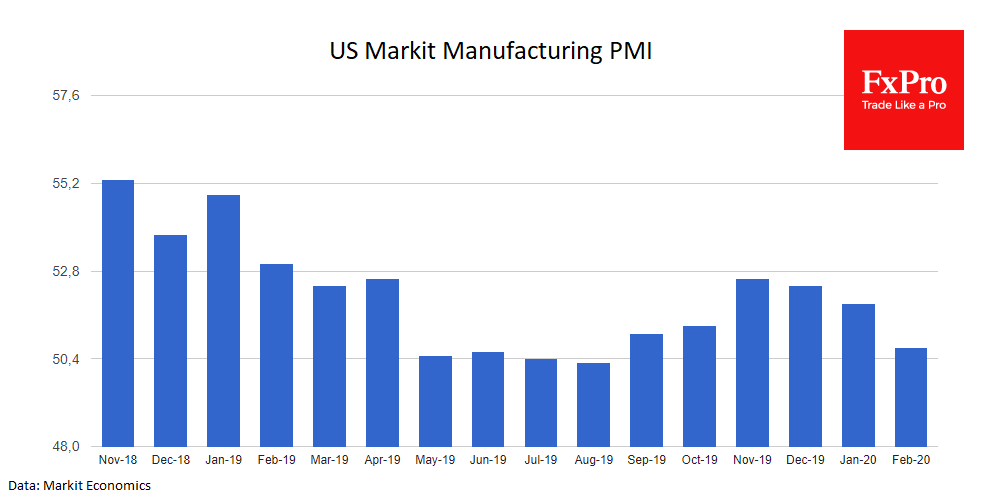

The US reaffirms that its economy is at the forefront of the global macroeconomic cycle. This is frightening news in the short term, as can be seen from the data published in previous days. That makes us expect with caution the most influential publication of this week – Friday’s NFP.

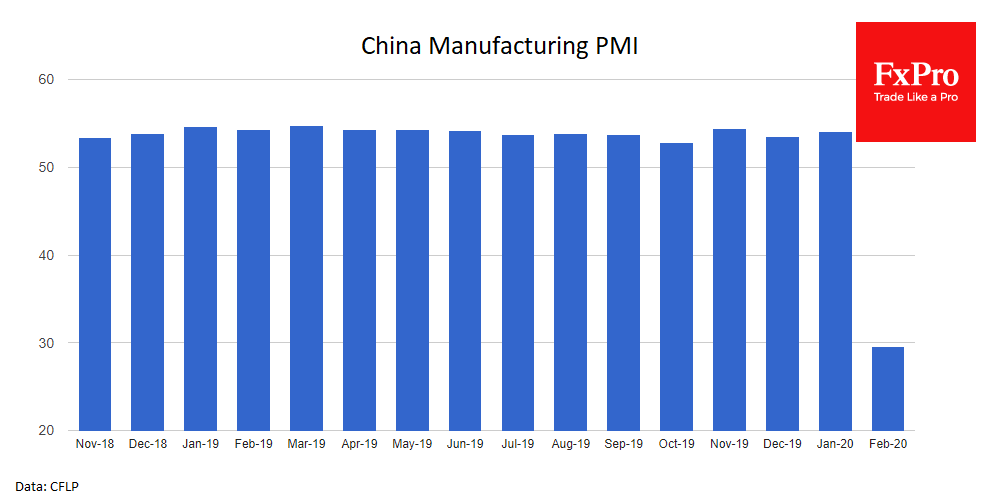

China published its industrial and service PMI estimates for February on Saturday. They were record lows, declining below dips of the midst of the global financial crisis. The manufacturing index fell from 50.0 to 35.7. The activity in service sectors was even worse, with the index collapsing from 54.1 to 29.6. The decline was markedly more devastating than economists expected on average. However, there are more questions to their forecasts than to the reliability of the data from China.

On Monday it was the turn for European and US data. The ISM Manufacturing PMI fell to 50.1, clinging to growth territory (above 50.0). Comments on the publication show that global supply chain disruptions have mostly affected real sectors, especially electronics.

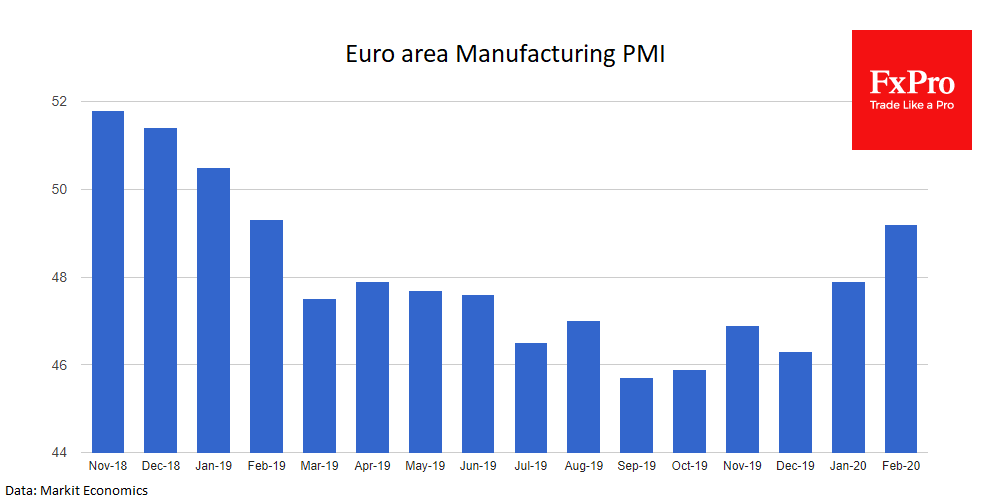

Although the review shows that positive sentiment prevailed, on the whole, it should not be overlooked that the indicator interrupted the growth. The PMI measured by Markit (like most other global indices) confirmed a slowdown in growth, falling for the third consecutive month.

In contrast, the final Eurozone PMI data not only came out stronger than expected but also confirmed the upward trend from the lows of September-October last year.

The weakening of the single currency in previous months was significant support for business activity and strong enough to overcome the negative sentiment from the coronavirus spread in China and beyond. Against this background, growth of the euro vs the dollar looks quite understandable. The contrast of data from the US and Europe is now clearly in favour of the latter.

However, these data should not be misleading. Business in America has traditionally been the first to respond to changes in the business climate around the world. However, it is also the first to be on the mend at a very rapid pace in contrast to Europe’s long-growing pace.

This means that we can see unpleasant surprises from the US statistics in the days and weeks ahead. On the contrary, comparatively positive data may come out from Europe, which may be late estimates of the past.

The FxPro Analyst Team