- Escalating tensions around the Strait of Hormuz push Brent toward higher targets as supply risks intensify.

- Oil may rise toward $100, but strong reserves and US shale output reduce recession risks.

Oil prices jumped to their highest levels since July amid Iran’s intention to set fire to all ships passing through the Strait of Hormuz. Donald Trump’s assurances that the US would provide the world with access to energy only temporarily calmed investors’ nerves. This involves American military ships escorting tankers for a moderate fee. However, these ships will be targets of attacks by Tehran. Simultaneously, the increase in transport costs will raise Brent and WTI prices.

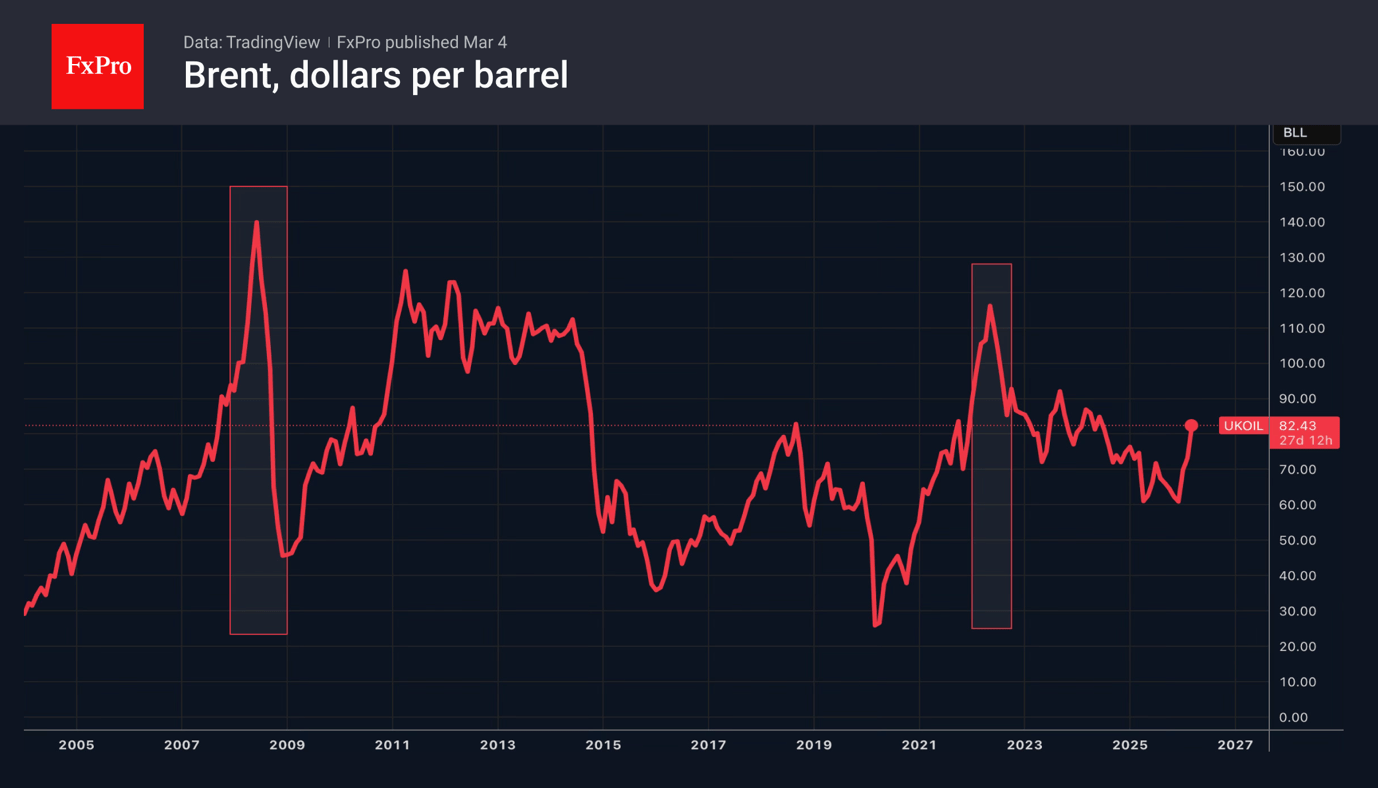

The IMF believes that US and Israeli attacks on Iran are increasing uncertainty in the global economy. However, we are still far from a crisis. Even the most ardent bulls do not expect oil to rise above $120 per barrel. Current prices are significantly lower than the $139 seen at the start of the armed conflict in Ukraine. Not to mention peaking at $147.5 just before the global financial crisis of 2008. It is doubtful that events in the Middle East will lead the world into recession, as happened after the oil shock of 1973-1974 or after Saddam Hussein invaded Kuwait in 1990-1991.

The main reason for a calmer reaction is that this geopolitical heat occurred amid the crude oil bear market. Shale production is a necessary trump card for the US. The IMF notes that countries have about 1 billion barrels in emergency reserves. How quickly they will be depleted will depend on the duration of the armed conflict in the Middle East.

According to Goldman Sachs, a prolonged five-week disruption of supplies through the Strait of Hormuz will cause Brent crude to rise to $100 per barrel. Wood Mackenzie cites the same price, assuming that oil flows are not restored soon. In this scenario, China may reduce oil imports, which will further drive up prices. JP Morgan believes that a prolonged pause in transit through the world’s main oil artery could lead to the Middle East reaching its storage capacity for black gold in tankers and onshore reservoirs. As a result, production will begin to decline.

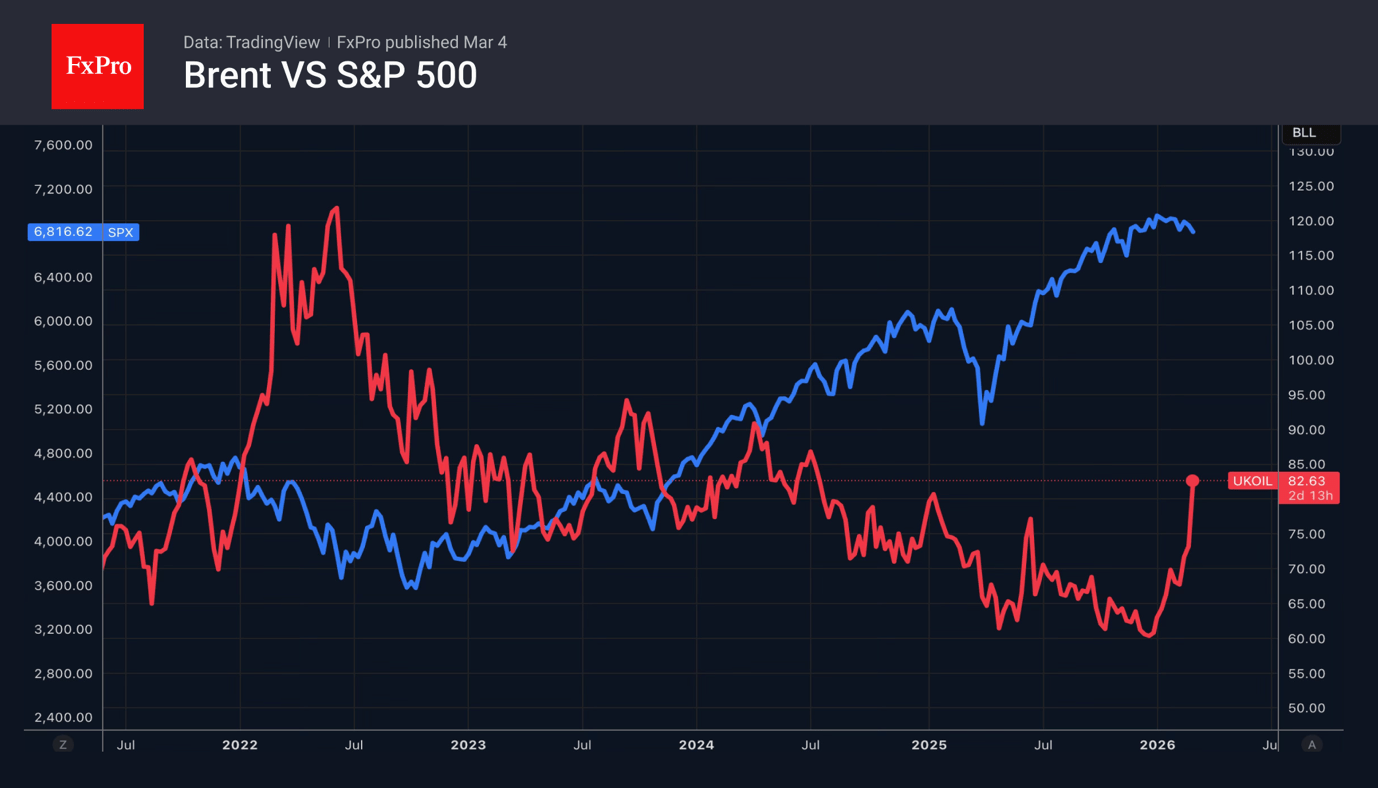

In contrast, production in the US will increase as prices rise. This may help the economy, but it is unlikely to support the stock market. The energy sector accounts for only 3.5% of the S&P 500’s capitalisation. Most companies are energy buyers, not sellers.

The FxPro Analyst Team