Technical analysis suggests deeper correction for the dollar

January 13, 2022 @ 12:38 +03:00

Fundamental and technical factors on the dollar locally give opposite signals. However, after a long period of strengthening the American currency, a corrective DXY pullback looks like a logical short-term prospect.

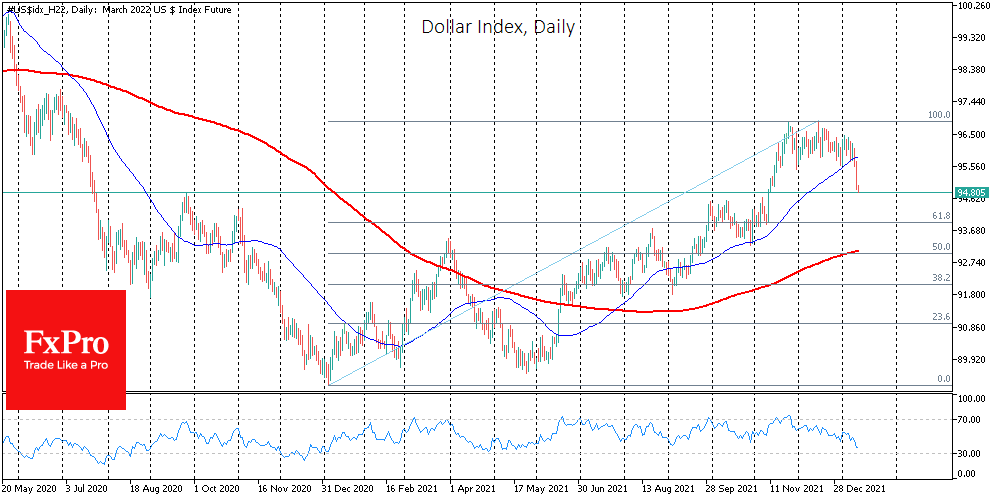

On Wednesday, the US dollar came under pressure, the sharpest loss since last May and coming out of a prolonged consolidation. The dollar index retreated below 95 for the first time in two months.

EURUSD surpassed 1.1400, trading at 1.1440 at the time of writing, having consolidated beyond the narrow range where the pair had spent the previous almost two months.

Often such a decisive move out of the range is followed by a further breakout move, which we may well see in the coming days.

The Dollar Index closed below the 50-day moving average on Tuesday and made a further move lower on Wednesday. The fall out of the range gave an informal start to the correction after the rally from May through most of November and the sideways movement in December.

A potential target for such a pullback is seen in the 93.50-94.00 area. Near 94 is the 61.8% Fibonacci retracement of the dollar’s move amplitude in 2021 and the starting point of the last rally in November. Near 93.50, the peak area of the index last year could be equally strong support.

It hardly makes sense to say now that we are seeing the start of a big wave of dollar decline, as solid fundamentals support its growth. It looks like Fed members started a competition on whose expectations and comments are the most hawkish, and consumer inflation has given little reason to change the rhetoric.

Among the latest comments is Powell’s reassurance that the economy can cope with rate hikes. Fighting inflation is a top priority for the US central bank. Mary Daly, president of the Federal Reserve Bank of San Francisco, predicts a first rate hike as early as March. This practically rules out a pause between the end of balance buying and the first policy tightening.

Furthermore, there are increasing signs that rate increases can continue to occur more frequently than once a quarter, as was the case in the previous tightening cycle. Many other central banks in developed countries are not yet prepared to tighten their policies as vigorously, which generally creates a sustained pull towards the USD on the interest rate differential in its favour.

The FxPro Analyst Team