The US market opens later today after a long weekend. S&P500 futures indicate a 1.5% gain to Friday’s closing level, playing off the positive outperformance on the outside. The currency market has also swung towards buying risky assets, reinforcing hopes of at least a rebound in the coming days after a 13.5% dip from the highs to the lows of the month in the first two weeks of June.

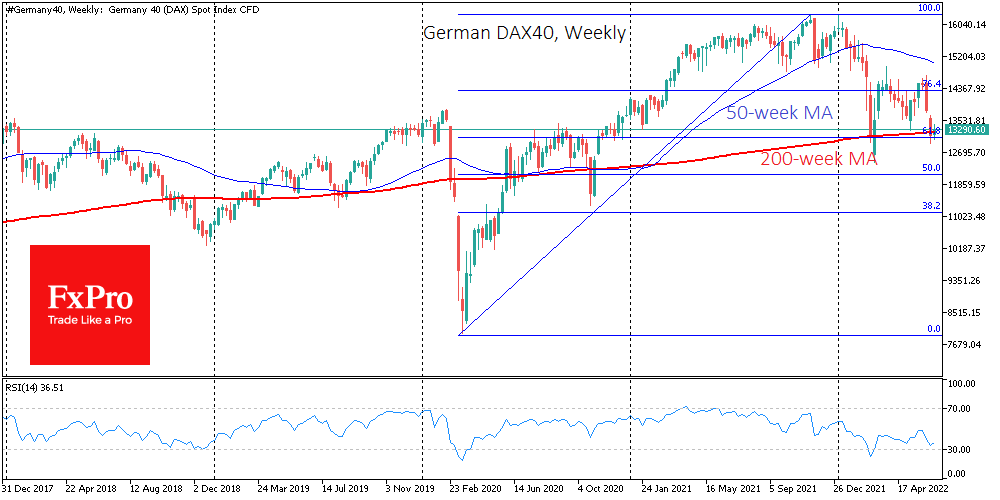

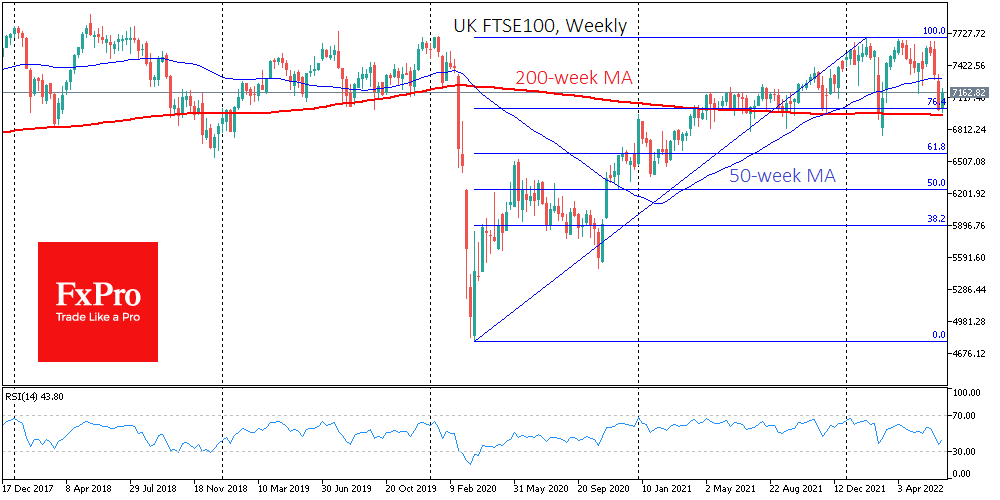

In equities, the positive tone is set by the performance of Asian equities and the recovery of major European indices from oversold territory. The DAX40 and FTSE100 are recovering from their lows of March. Both indices have stuck within the Fibonacci retracement pattern and got support at 61.8% for DAX and 76.4% for FTSE from the pandemic amplitude.

The weakening of the traditional shelter currencies – JPY, CHF – is setting a positive tone. The USDJPY has updated to a new high since 1998, above 136, indicating a return of risk appetite in some financial market segments. USDCHF settled near 0.9660, stopping the decline after last week’s unexpected SNB rate hike.

The euro and the pound are also gaining against the dollar, signalling a recovery in risk appetite.

However, it is essential to note the fragility of the current rebound. Most likely, we will see a corrective bounce after the worst week in equities in more than two years.

However, finding medium-term reasons to buy “risk” is still tricky. Aside from the BoJ, the main central banks are tightening policy or promise to do so as soon as next month. And so far, we see no sign that this trend is about to end or reverse.

Thus, cautious investors can still only tune in for a short-term bounce but do not hold out hope that the markets have bottomed out. The bear market in the USA will likely continue until we hear from the Fed the first hints of a halt to aggressive policy tightening. Until then, a bear market with occasional corrective bounces is likely.

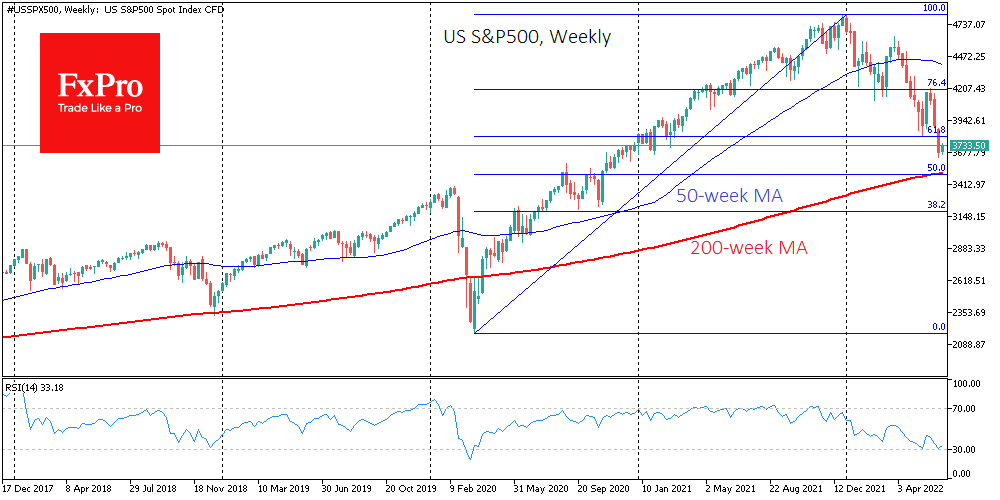

History also tells us that after entering a bear market phase and losing 20%, the market loses about another 20% on average (about 2900 for the S&P500) before it finds its footing. This scenario looks especially relevant when the Fed is not at all concerned about markets correcting, as it did at the beginning of the pandemic.

But it is too early for the bears to celebrate because they have yet to break the emerging rebound and push the S&P500 below 3500, significant psychological support, where the 200-week moving average and critical support/resistance levels of the second half of 2020 are located.

Our pessimistic scenario could be reversed if the S&P500 exceeds the 3900 mark during the emerging rebound. In that case, a reversal of the equity market to the upside would have to be considered.

The FxPro Analyst Team