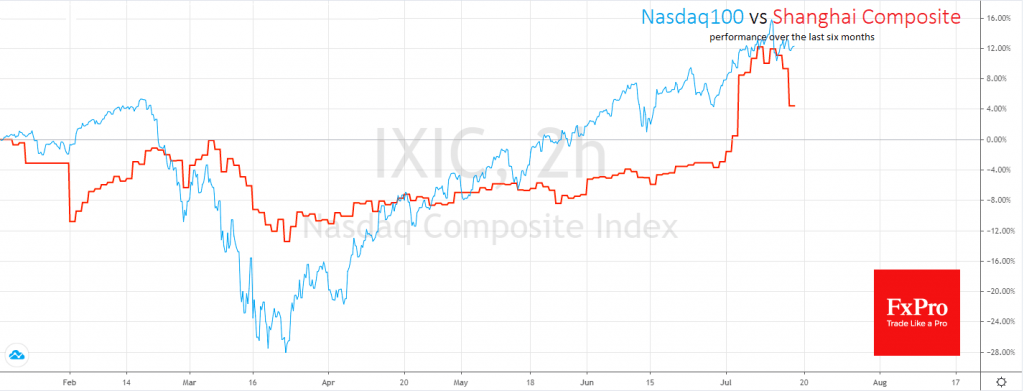

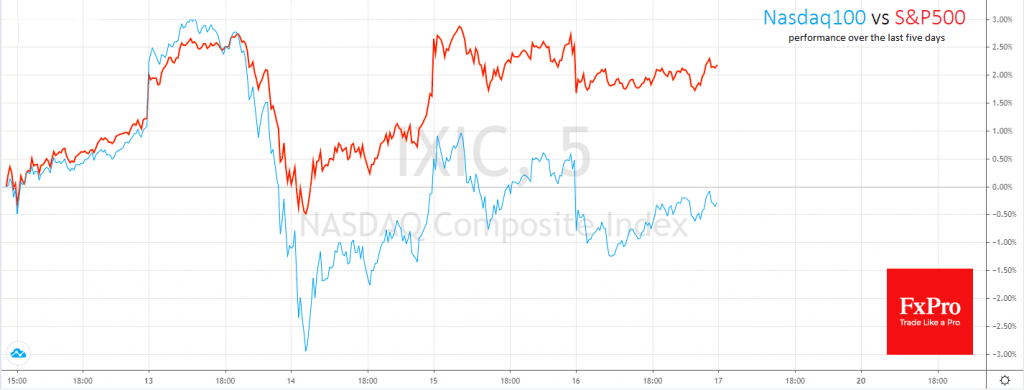

Relations between China and the US continue to heat up, putting pressure on financial markets. The main blow was to the Chinese exchanges, which have been losing more than 5% this week, correcting the rally that took place earlier in the month. Among the US indices, so far this week negative values are shown by Nasdaq, despite growth for S&P500.

Notably, the leaders of the last days and months are now feeling worse than the overall market. It’s probably not fears of a second wave of coronavirus, but a revaluation of economic prospects that drives the markets now.

China’s indices and Nasdaq contain many so-called growth stocks and cyclical companies. Their values are rising faster than before, showing economic growth and increasing consumer spending. However, if they slow down, they tend to lose the most.

Excessively low expectations characterize the current reporting season. Analysts expected to see a complete disaster, but 80% of companies that have already reported have exceeded expectations. This is a reason for a decisive impulse in response to publications. However, it is mostly short-lived, as earnings are seriously declining against last year’s values, hardly justifying new stock price highs.

There are also more unpleasant exceptions. Data on registrations of new Tesla cars in the US halved last quarter, which hardly explains the two-fold increase in stock prices over the same period. Fresh reporting by Netflix caused disappointment of investors, with a 9% share price drop in after-hours trading. Earnings per share in the second quarter was $1.59 vs expected $1.82.

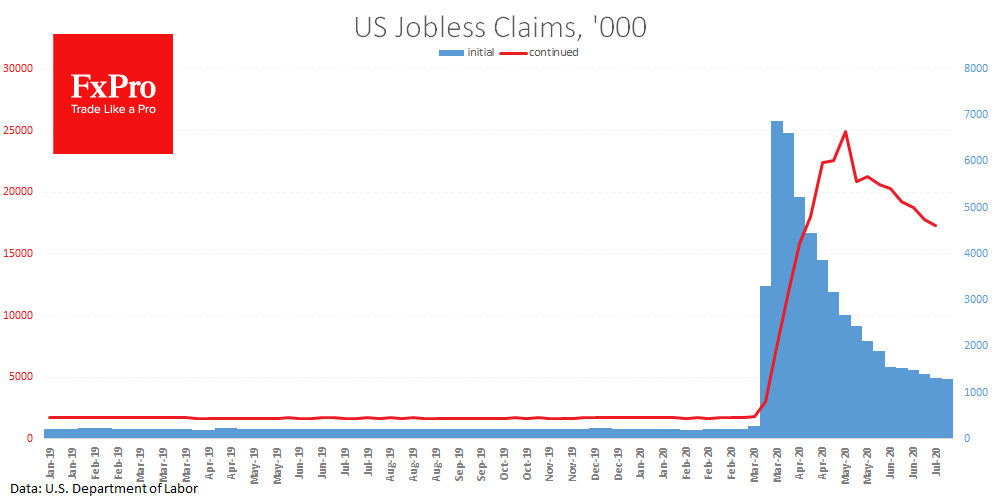

The US and many other economies are operating at full capacity not only due to forced holidays but also long-term layoffs and concerns about future earnings. The temporary coronavirus lock down is more and more notably causing another economic slump.

The latest weekly data showed 1.3 million initial jobless claims last week, with more than 17.3 million receiving them not for the first time. The latter figure was better than expected, but ten times higher than the pre-crisis norm. This suggests the economy is not recovering stronger than predictions. However, the forecasts themselves are hitting rock-bottom. As a result, we are witnessing more and more signs of rotation of investors from growth shares into protective sectors. It may still be too early to talk about the total winding down of risk positions in the markets, which manifests itself in the growth of the dollar and the widespread collapse of stocks. The only noticeable thing is the weaker performance of the star companies during the second-quarter rally.

The FxPro Analyst Team