Scary present vs bright future

April 29, 2020 @ 12:01 +03:00

Financial markets returned to growth on Wednesday morning, despite the decline in demand for risk assets at the end of the previous day. Futures on S&P500 added 1.3% on the back of further upward movement of China and Japan stock indices due to quarantine measures easing in different parts of the world. At the same time, there is a rather unusual situation in the markets.

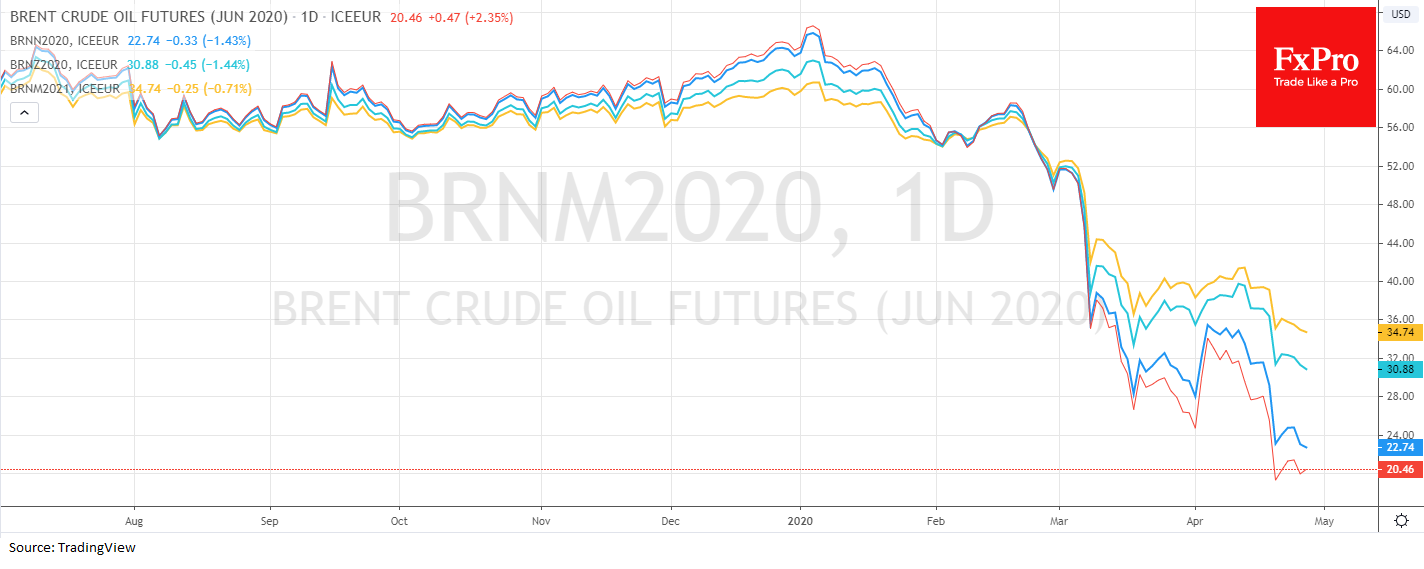

The difference between the prices of closer and longer-dated futures has grown sharply since last week and remains exceptionally high. June contract priced Brent oil at $20.5. The July contract is slightly higher ($22.7). The December contract is already at $30.9 (+50%). Contango is the norm for the commodity market, as this price includes storage costs. However, this gap is too high now. Investors are pricing in restoring the balance of supply and demand. Moreover, before March there was a backwardation in the market (when prices of longer-dated contracts were lower than closer deals).

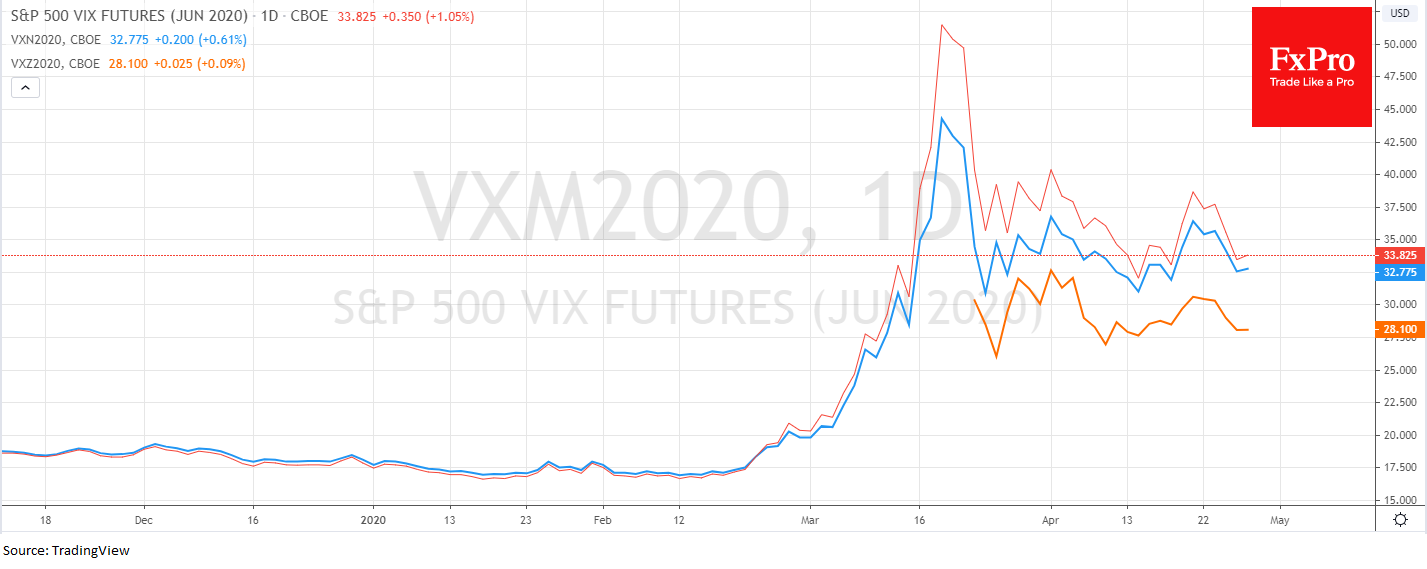

The situation with VIX futures is similar. For it, the norm is higher levels for longer-dated contracts: the further the maturity, the higher the uncertainty, which attracts a higher risk assessment. The situation is quite the opposite this time. December futures on VIX from the end of March remain below the closer-dated futures. Longer-dated contracts are constantly below the nearest futures since late February when markets began to fall aggressively in fear of the coronavirus.

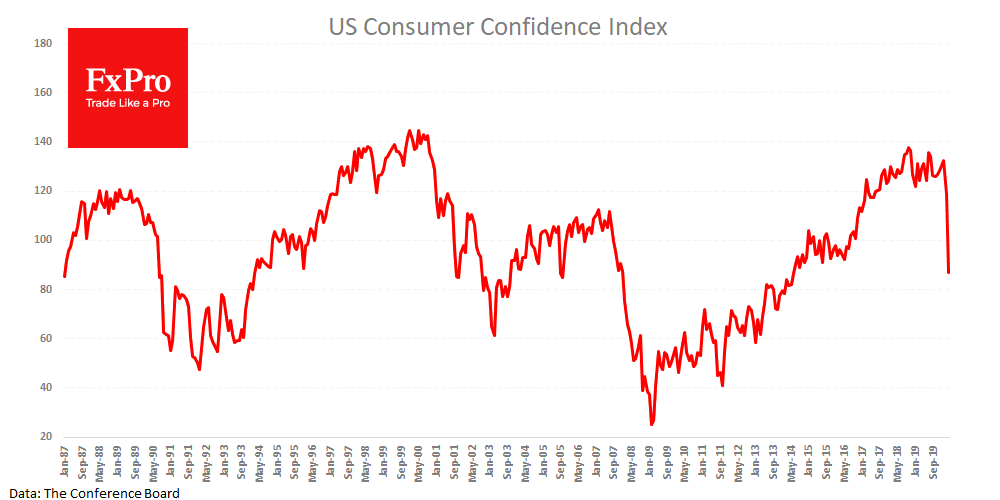

The US consumer confidence index released yesterday fits this pattern. The index’s sharpest monthly decline (far from recessionary levels, however) coincided with quite high consumer expectations.

It looks like the present is covered with fog, while the future is a better version of what is happening around us, drawing in more colourful tones. This is very good for the economy. But there are still risks that this optimism will face grim reality in the coming months.

The FxPro Analyst Team