Powell boosts the dollar, but not for long

March 08, 2023 @ 17:27 +03:00

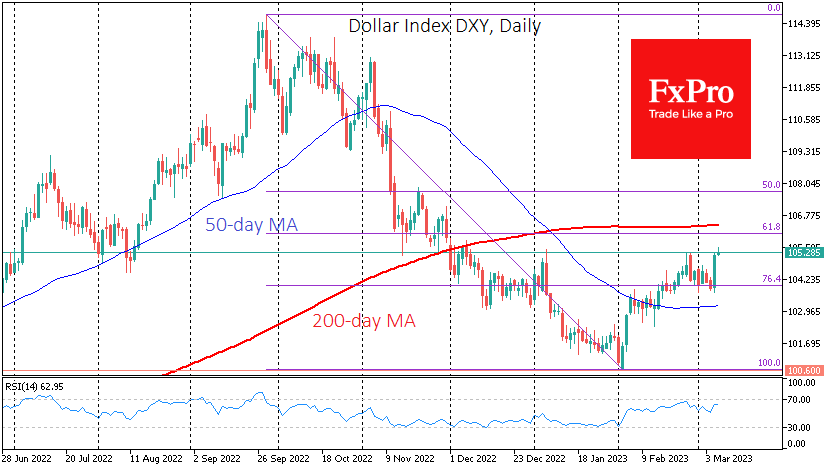

The Federal Reserve chief’s speech to Congress has suddenly proved to be a market troublemaker. The Dollar Index has gained more than 1.1% after Powell’s hawkish comments opened the door to a 50-basis point rate hike in March.

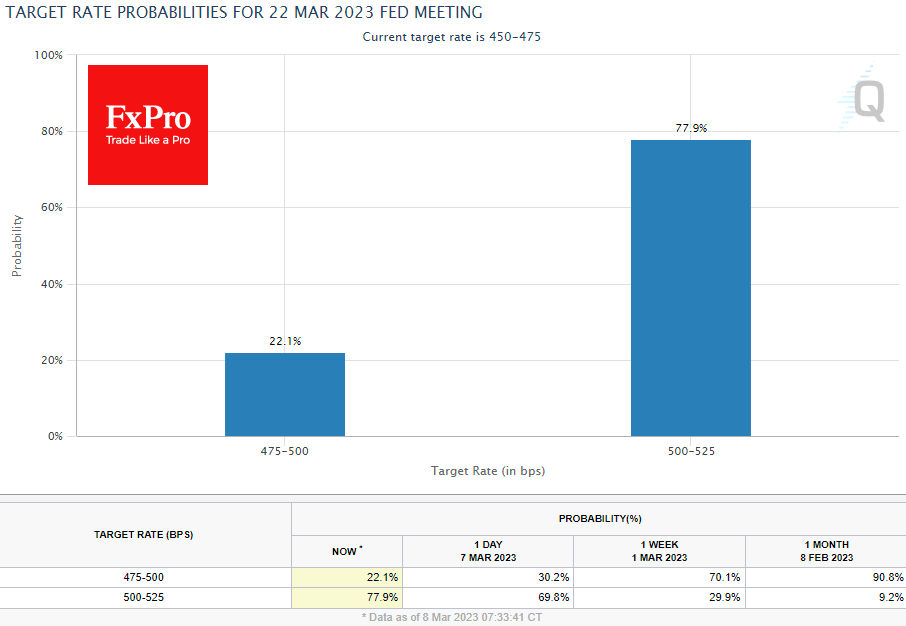

Interest rate futures are now pricing in a 70% chance that the Fed will raise rates by 50bps on 22 March. This is an impressive coup, given that markets were pricing in only a 30% chance of such an outcome only a week ago, and a month ago, they were pricing in a 9% chance. The sharp revaluation of expectations overnight has driven the bond market, dragging the currency and equity markets down against the dollar.

It is important to note that this repricing came after the Fed chief’s comments, not after the data. A month ago, we had the 517K jobs created in January, and a week before, we already knew about a big jump in consumer spending and a sudden rise in the PCE price index to 4.7% instead of the expected 4.3% YoY.

In addition, Fed officials have been trying for many weeks since the beginning of the year to make a case for a tighter monetary policy than implied by financial asset prices. We believe the markets expect more than the Fed is prepared to do.

It is a familiar story when the market initially ignores some risks but, at some point to see them only. On the face of it, the markets have gone too far in their fears.

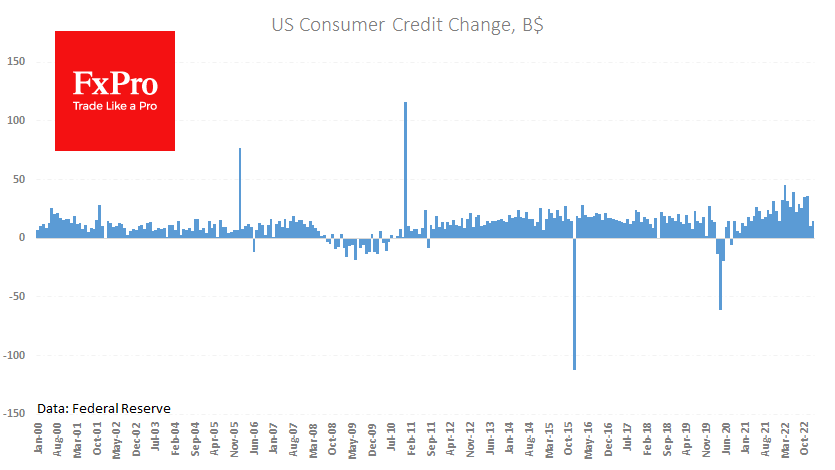

Yesterday, Powell pointed out that the full impact of the rate hikes that have already taken place has yet to be felt. The Fed’s data, released late on Tuesday, showed a net increase in a credit of 14.8bn in January after 10.7bn in December against an expected 25.2bn – a sure sign of cooling demand that is unlikely to go unnoticed by the central bank.

There has been a fundamental divergence between market expectations and the Fed’s comments on the timing of the reversal to a rate cut. At the beginning of the year, the markets were pricing the start of policy easing as early as late 2023, which directly contradicted the Fed’s projections.

More robust inflation data and an impressive jump in employment are reasons to raise rates further and hold them longer than expected. But a knee-jerk return to the 50-point hike after a 25-point tightening will not help the credibility of the Fed, which only recently signalled more fine-tuning of interest rates and cited signs of disinflation.

There could be a further reassessment of the odds in favour of a smoother rate hike scenario. It is reasonable to assume that the Fed will unlikely make a final decision before next Tuesday’s CPI data. In the meantime, we would not be surprised if FOMC members try to bring market expectations back to a standard 25-point hike, but with a target rate of 5.50-5.75% (a quarter point higher than previously expected).

If we are right, yesterday’s rally in the dollar will not be sustainable, and the DXY will fall back in the coming days, as it has done from these levels since early December.

The FxPro Analyst Team