Only the stock market now believes in a V-shaped recovery

May 08, 2020 @ 12:17 +03:00

World stock markets are showing growth, but these dynamics have less and less support from macroeconomic data.

Weekly data on the number of jobless claims in the United States looks like the most timely assessment of the labour market. This assessment can hardly be called optimistic. Last week, 3.169 million people applied for benefits for the first time. The wave of the end of March is fading, but too slowly. During the first six weeks of the pandemic wave in the US, 30.3 mln asked for unemployment benefits. 70% of them continue to ask for it so far. The number of those receiving weekly benefits reached 22.65 million, against expectations of 19.9 million.

Average forecasts on payrolls today assume a reduction in the number of those receiving wages by 21 mln. However, the latest data make us expect even higher figures – about 23 mln.

During the period of quarterly reports, more and more companies are announcing layoffs. All this is an argument against the V-shaped recovery. Recently, Fed members frequently said that we should not expect a quick bounce.

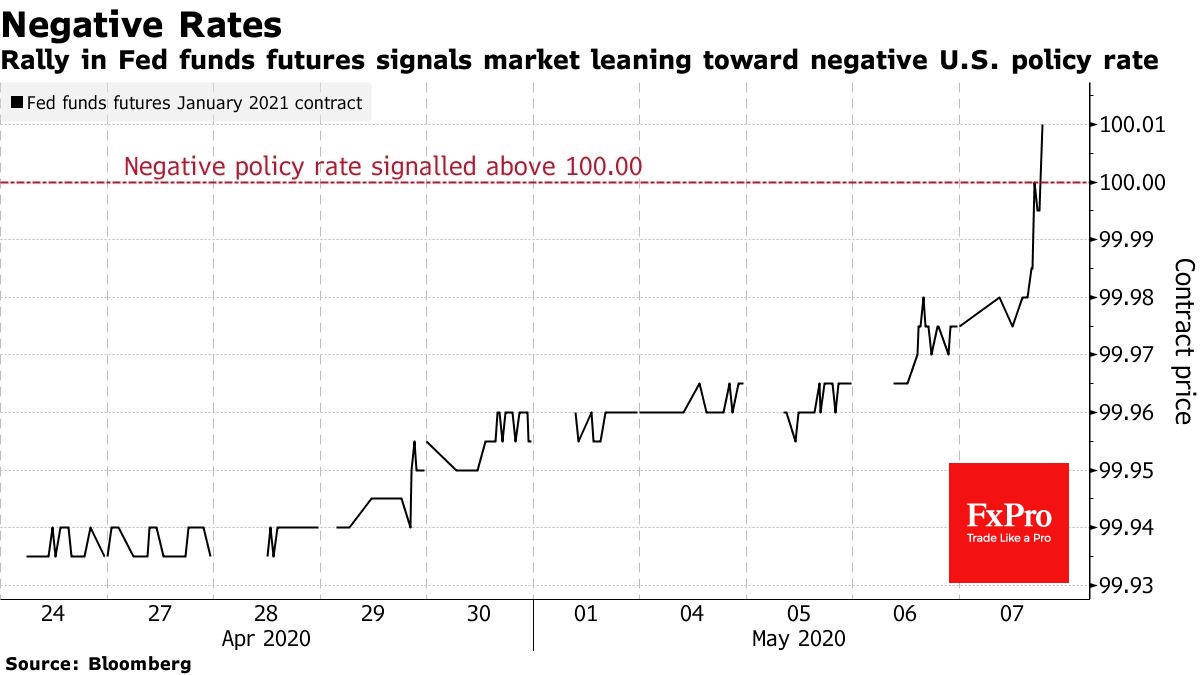

The debt markets also do not seem to take this scenario into account. Demand for US Treasury debt securities remains high, which drags down their yields. As a result, the implied Fed rate for the start of 2021 yesterday flirted with the negative territory.

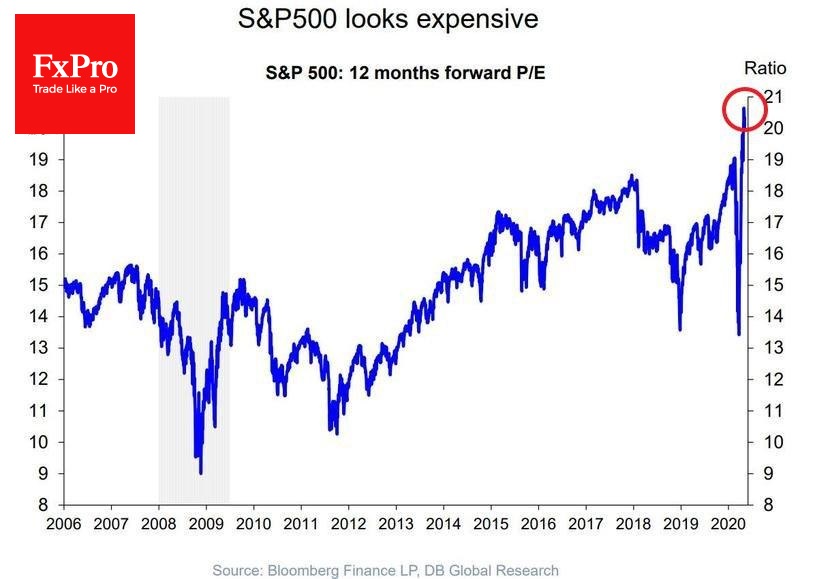

At the same time, the situation in the stock markets is different. Stocks of American companies offset a significant part of their decline in February and March. Nasdaq is even in positive territory so far this year. On the other hand, dividends and revenue forecasts are being reduced. The forward 12 month P/E ratio has updated the highs that the markets saw at the beginning of the year at the peak of index dynamics.

Perhaps, there has never been such a clear divergence between changes in the economy and the markets before. Of course, stock markets are often ahead of the curve, bouncing back before the global situation completely normalizes. However, false optimism is also often triggered. Now purchases are conditioned by the fact that investors remain confident that the worst for the economy is over.

This is true, but only partially. Yes, of course, some sectors of the economy are already being restarted. However, at the same time, fundamental changes are inevitable. No matter how many bonds the Fed buys on its balance sheet, it won’t be able to save companies from bankruptcies caused by a lack of sales. Most of all, it concerns the service sector, which accounts for 85% of all US jobs.

The FxPro Analyst Team