Events in recent weeks have brought back interest in assets that have benefited from tensions in previous decades, with gold rising as insurance against currency destabilisation and oil rising on fears of surging demand and shortages of supply if sanctions constrain supplies from Russia.

Interestingly, the West is trying to balance sanctions restrictions on oil as more encouraging comments come out of the talks with Iran.

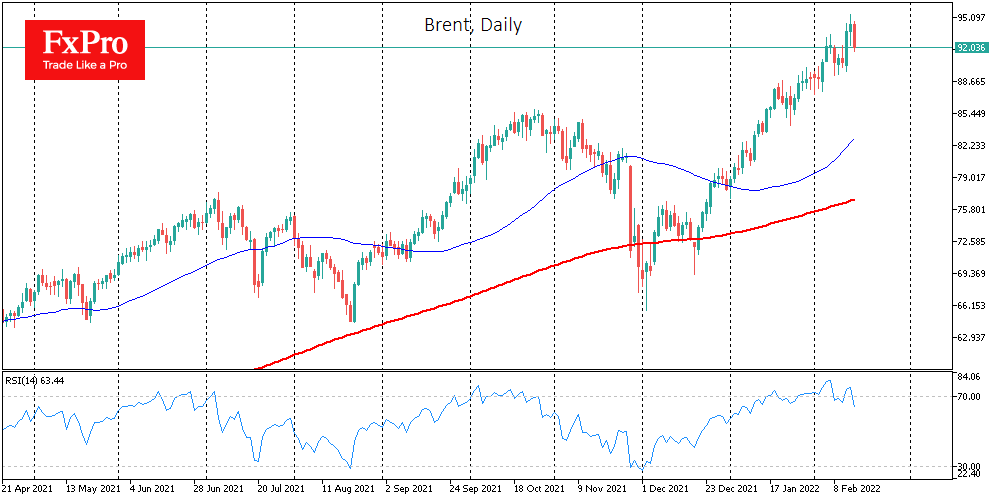

In our view, oil is very expensive, climbing to current heights faster than the economy can afford it. This rise is caused by geopolitical tensions around Russia, which acts as the world’s largest energy exporter by a wide margin.

Fears about the stability of future supply have so far outweighed any negatives, but it is still prudent to zero in on geopolitical influences over the medium to long term. And with that in mind, the oil price looks unsustainably high, vulnerable to a corrective pullback once the dust of military hardware settles.

About 12 years ago, we saw a similar picture when oil prices recovered quickly. And then, the result was another round of global economic weakness, which also knocked down demand for commodities and forced regulators to postpone policy normalisation steps. Will it be like that now? Quite possibly, and then in the second half of the year, oil could turn sharply to correction and cause another shock for the economy.

In recent weeks, significant factors are potentially capping price rises with increased drilling activity. Also, Russia will ramp up production as most of the wells are in areas with a harsh climate.

Looking locally, we can see how quickly any declines in oil over the last three months are being bought out. In such an environment, oil could soon find itself in short squeeze territory, with short positions being forced to close due to rising prices. This mirrors what we saw in April 2020. It is difficult to predict the peak price level in such an environment.

It would be an ideal market picture if the short squeeze occurred at the end of April on another major expiry, paying homage to events two years earlier. And ideally, if we saw a price return to the $112 area where the bear market in oil started in July 2014. But this is an idealised picture. The reality is likely to be less mathematically accurate, as so much is now tied to the actions and comments of policymakers.

The FxPro Analyst Team