Oil pressured despite verbal interventions

December 05, 2023 @ 17:54 +03:00

Oil remains under pressure, reflecting fears of demand cuts, despite verbal interventions by OPEC+ and US government officials over the past week to shift the balance in favour of a deficit.

Last week, the expanded OPEC+ agreed a production cut of 2.2 million bpd from the set quotas for the first quarter of next year. This is a reduction of 900k bpd from what we have had so far.

This news did not help to bring the oil price back above the 200-day average, which acted as resistance in November.

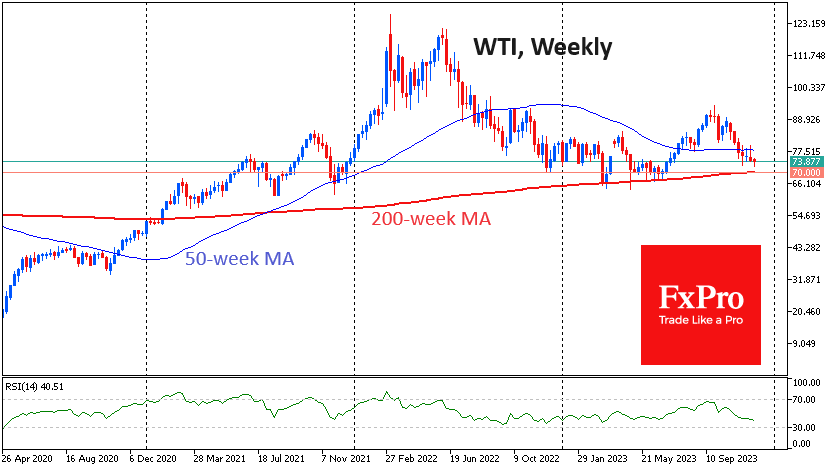

Already this week, cartel officials have reminded us that they may extend this or even deepen the cuts. But it seems that even this did not impress traders. WTI prices updated the lows for five months, going under $72.40. Brent, at the height of the European session on Tuesday, held slightly above the November low.

Even more interestingly, US Presidential administration officials have indicated that they will buy back as much oil to replenish the strategic oil reserve as they can at current prices. Technically, this also supports the price.

It was logical to expect oil to quickly move higher on such news, but we see a fourth session of declines.

Apparently, sellers are on the side of falling actual demand, which pressurises prices despite promises to cut production.

But it is quite possible that the pressure on prices in recent days was a sell-off after a failed test of the 200-day moving average. From current levels, oil has downside potential to $66-70 per barrel WTI and $70-73 for Brent, from where it was repurchased from March to the end of June and several more times from July 2021. A decline in this area would bring the 200-week average back into focus, which requires global events such as a rupture within OPEC, a global pandemic or abnormal volatility in financial markets to break.

The FxPro Analyst Team