Markets were confused by Friday’s US labour market data, not knowing how to react to solid job growth. This is a negative for equities, as it makes us expect a third consecutive 75-point Fed rate hike at the next meeting on 21 September. But job growth and the continued pace of wage increases is a positive signal from the economy, where companies continue to hire, and people continue to spend. In our view, there are more positives here, encouraging long-term buying in sagging stocks, despite the risks of local corrections due to short-term overbuying.

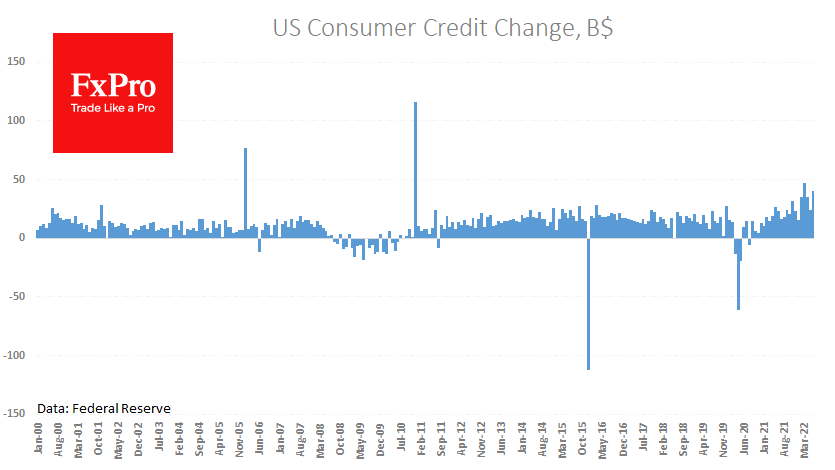

In July, the US labour market added over half a million jobs and maintained a 5.2% y/y growth in hourly earnings. The Fed on Friday also reported consumer credit growth of $40.2bn in June, up from $23.8bn in May and $25bn expected. This is a very high reading, as we only saw higher in March, excluding two spikes caused by one-off programmes.

People are rushing to borrow before rates get even higher. This promises to heat consumer inflation even more, so there will be pressure on the Fed to conduct policy tightening more quickly. But Americans are no longer as indebted as they were at the start of the financial crisis, so we can’t say yet that the situation will end in a global financial crisis – 2.0.

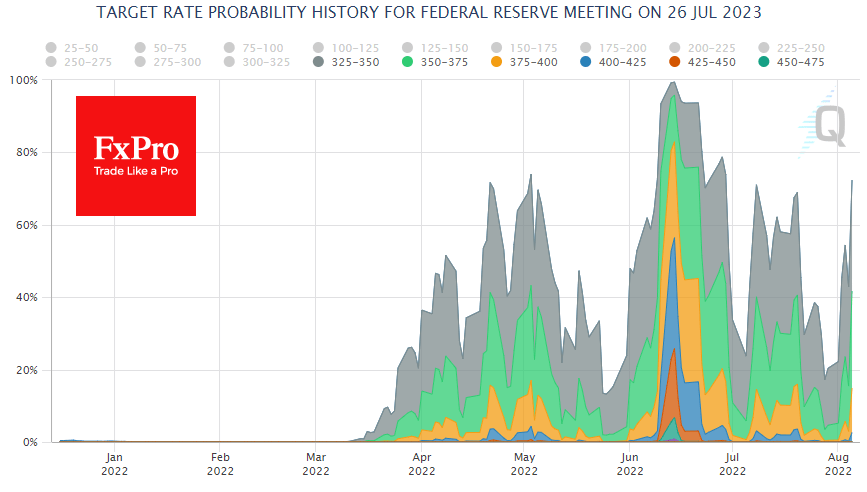

Debt markets, the so-called “smart money”, have eased their bets that on July 2023 the rates will be much higher. This trend broke in August but, as we can see, has not stopped stock buyers. Strong employment growth in July, credit data and durable goods orders confirm that the economy is coping with the Fed’s tightening. So far, rate hikes and rising inflation have only been a stimulus to accelerate consumption.

A caveat is worthwhile here too. In the next two quarters, the Fed will likely step on the brake pedal too much. In that case, the sell-off could return to the stock market. But this is just causing future turmoil. The current data, for now, sets the stage for continued careful stock buying.

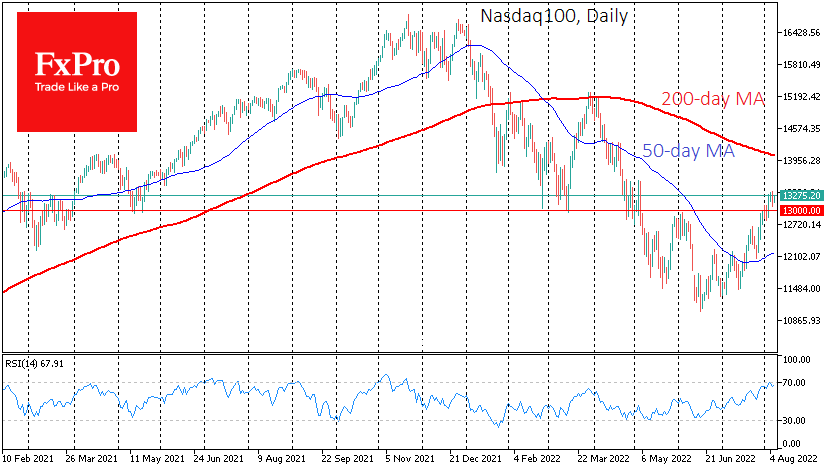

The nearest technical target for the Nasdaq100 looks to be the 200 SMA, which coincides with the round level of 14,000. If the markets opt for a swing-back before a new ascending impulse to clear the local oversold area, it is worth looking at 13,000. This area concentrates on the local highs of June and the lows of April, March, February, and May 2021.

The FxPro Analyst Team