More data confirms positive market sentiment

December 19, 2019 @ 11:13 +03:00

Markets reacted sluggishly to the vote in the US House of Representatives, which initiated the third impeachment of the president in the history of the country. This issue should be further considered in January by the Senate, where the majority is Republican, as is Trump. So the chances of a real removal of the president are negligible. The whole procedure should be seen as part of the Democrats’ election campaign aimed to pressure Trump’s position ahead of 2020 elections.

American stock indices and the dollar mostly ignored the results of impeachment voting. Asian markets are retreating on Thursday from the local highs reached earlier this week. However, such dynamics looks like a cautionary approach to close partly profitable positions before the holidays, rather than a complete rejection of risks.

The currency market also confirms that the positive mood among global investors remains in place. The USDJPY remains close to the half-year highs, showing signs of break of a downward trend. Previously, the pair broke above the resistance level of the downstream channel and consolidated confidently above the 200-day average. It can be an early sign of a principal change in investors’ sentiment towards optimism.

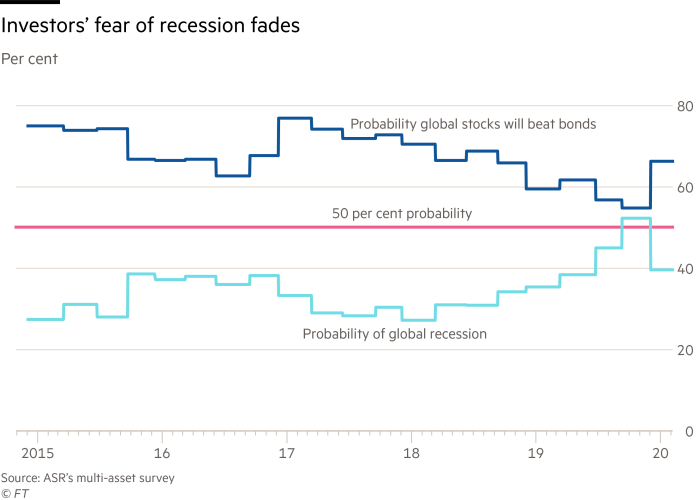

Other indicators have shown the same signals in recent days. A Bank of America weekly survey of portfolio managers showed the recovery of optimism related to the prospects of economic growth in 2020. These changes in sentiment were also confirmed in a regular study by Absolute Strategy Research, which showed the sharpest decline in fears of the global recession in the next 12 months from 53% to less than 40%.

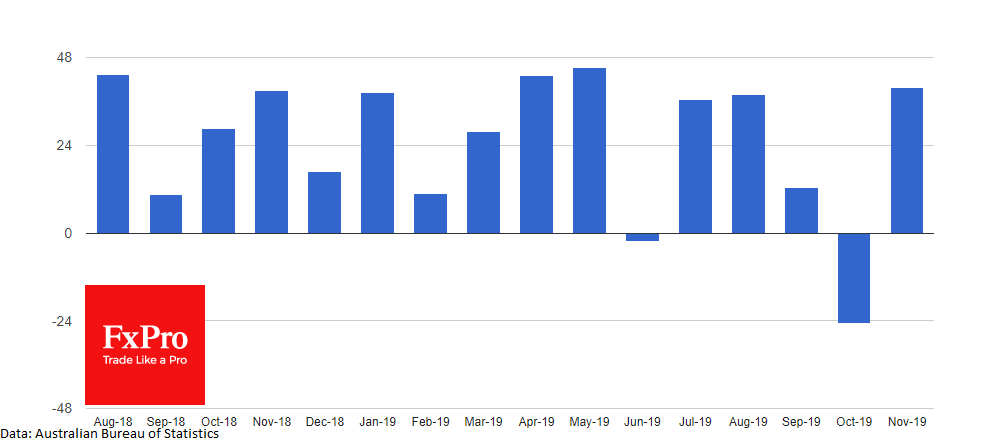

If that is not enough, positive macroeconomic data are already coming from the Asia-Pacific region. The published data on employment in Australia in the morning sharply exceeded expectations, which caused an AUDUSD to rally on decreased fears of further rates cut.

New Zealand also saw a sharp increase in GDP by 0.7% QoQ against the expected 0.5%. At the same time, the country’s trade deficit is persistently crawling down. Improvements in both countries are not only a good symptom for the national economies but also potentially reflect the strengthening of business activity in China and fuel demand for commodities. Oil is growing for the sixth consecutive trading session, rising to levels above $65.4, where it not seen steadily traded since July.

The market sentiment reversal and clear signs of accelerated global growth support speculation that the Fed, ECB and other key central banks have managed to turn the tide, overcoming the negative impact of trade disputes.

However, trade conflicts are far from over. We cannot exclude a new wave of trade confrontation between the US and the EU in addition to a trade conflict with China. So it is unlikely that the central banks should count on a long respite.

The FxPro Analyst Team