Politics will continue to influence financial markets next week as details emerge of the policies that Trump and his administration envisage pursuing. These statements, as well as those from influential Republicans, may have a greater impact on markets as that party secures a majority in the Senate and appears to retain a majority in the House of Representatives, not to mention a Republican presidential victory.

Among the key scheduled events, the following releases could impact the markets.

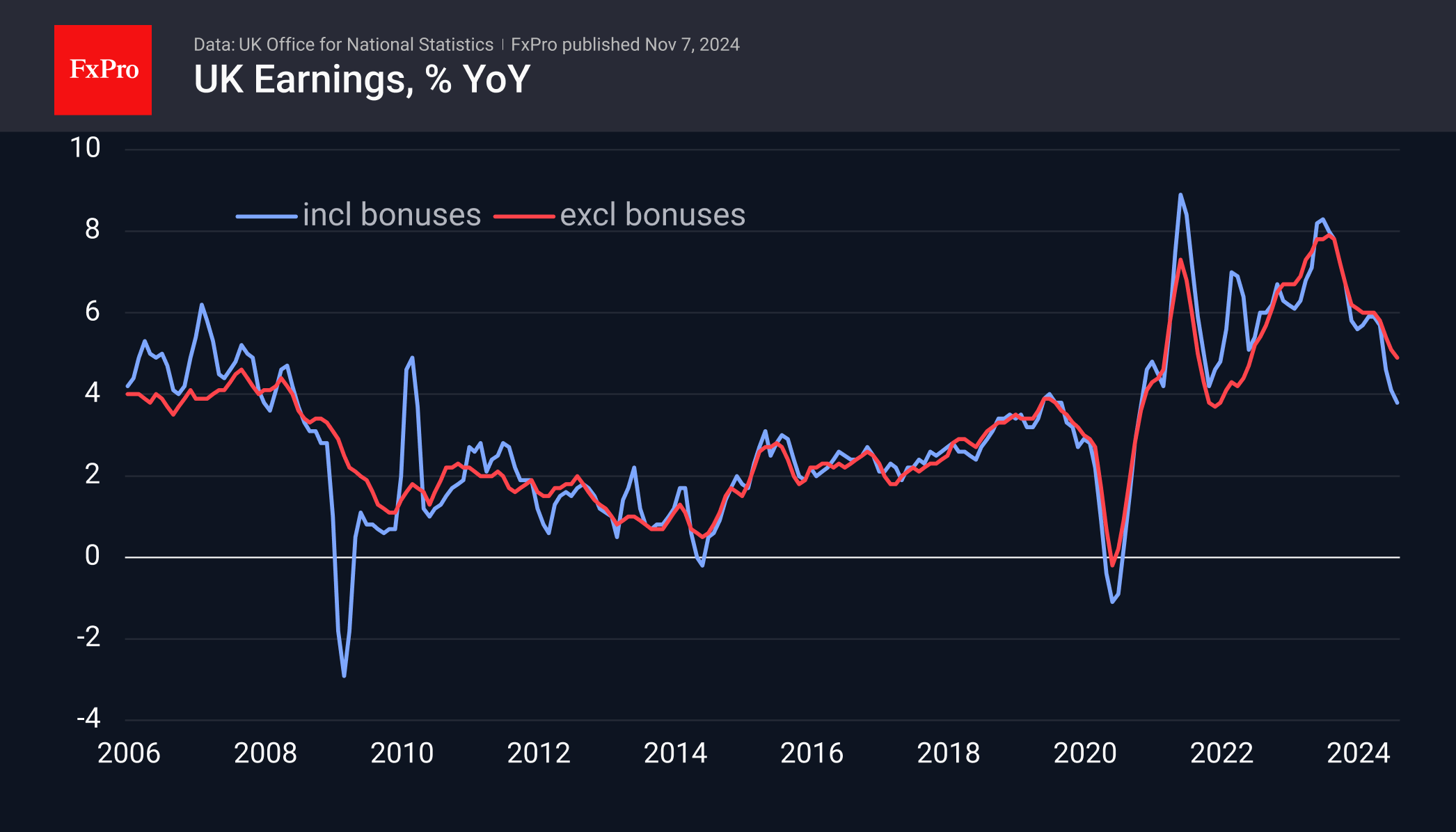

On Tuesday morning, we will see the release of UK employment data. Wage growth has been slowing there for about the last year and a half, but it has been outpacing inflation and is about double the 2% level that the Bank of England is targeting. These are pro-inflation risks that could be to the pound’s advantage if we don’t have a surprise bounce.

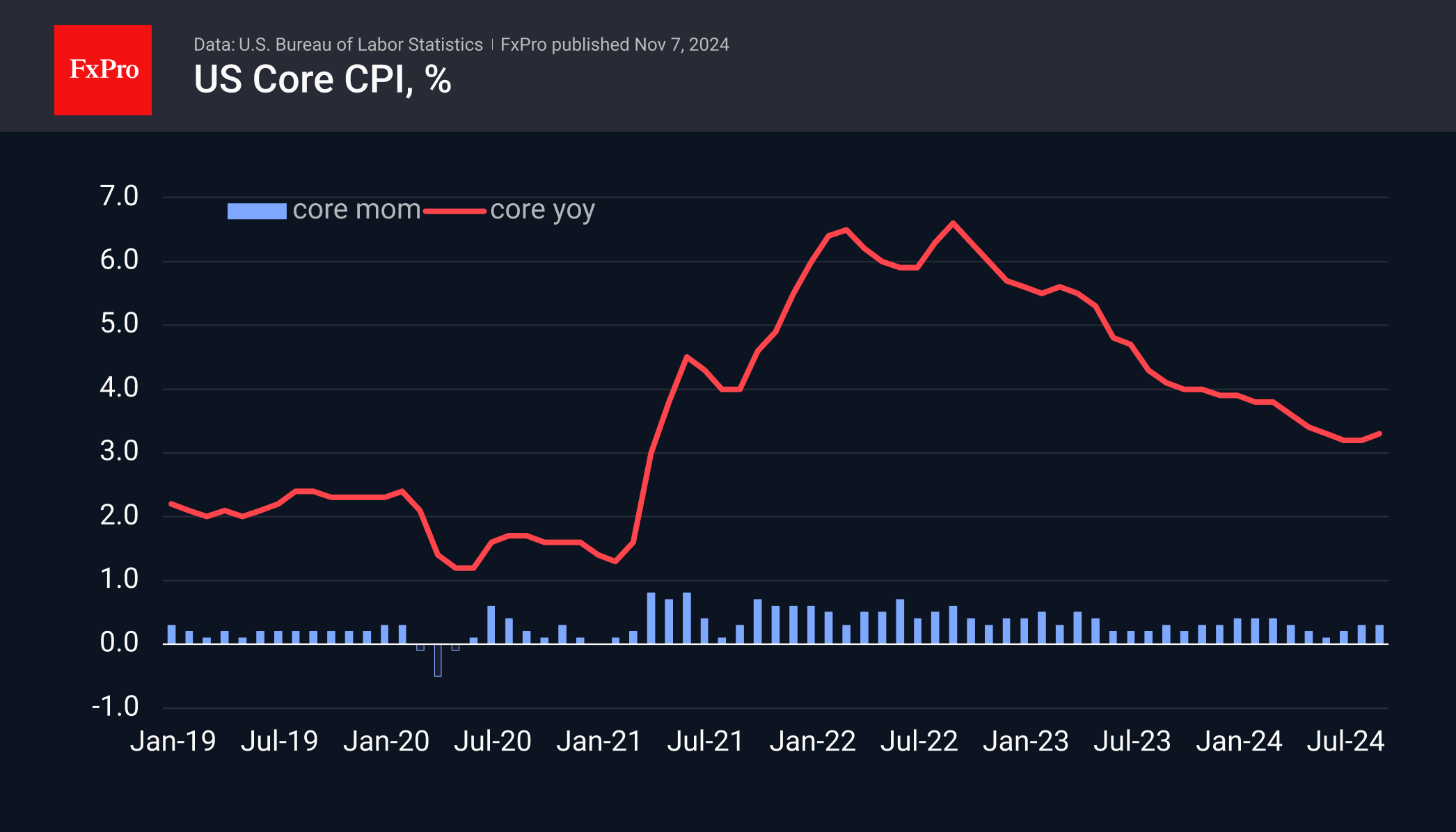

Wednesday’s blockbuster for markets promises to be the release of US consumer inflation. Since March, overall growth has slowed from 3.5% y/y to 2.4%. Core inflation, excluding food and energy, fell from 3.8% to 3.2% in August and ticked up to 3.3% in September. All eyes are on whether this is a reversal of acceleration. If so, it favours a fundamental revision to the Fed’s key rate expectations for next year, causing a shift in markets in the form of a rising dollar and pressure on risk assets, from equities to commodities.

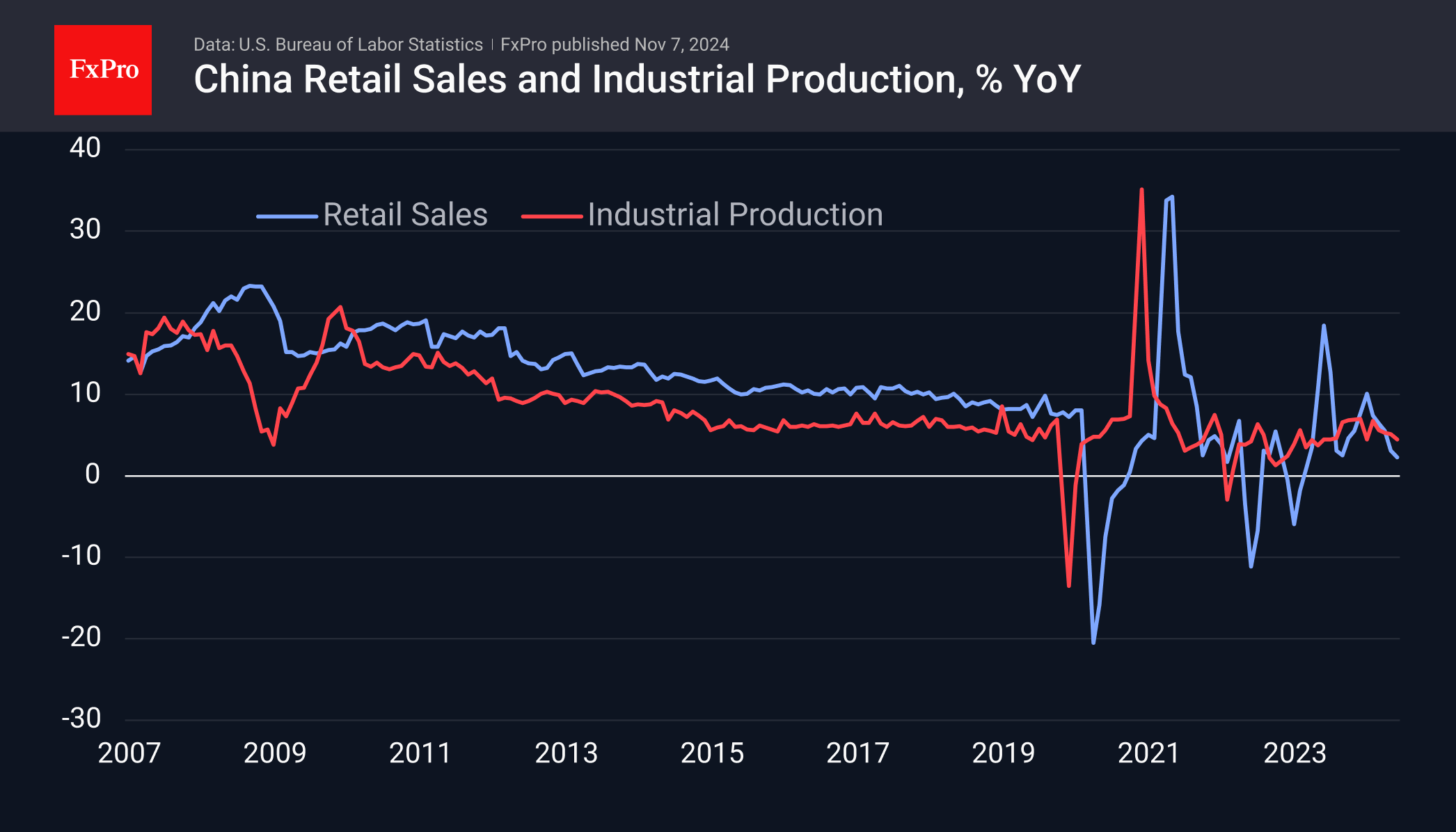

On Friday morning, attention is focused on a batch of October statistics from China, from new home prices and the unemployment rate to industrial production and retail sales figures. Investors are waiting for further signs of accelerating growth in the Celestial Empire, which could boost not only its stock markets but also create a positive mood for markets in Europe and Asia.

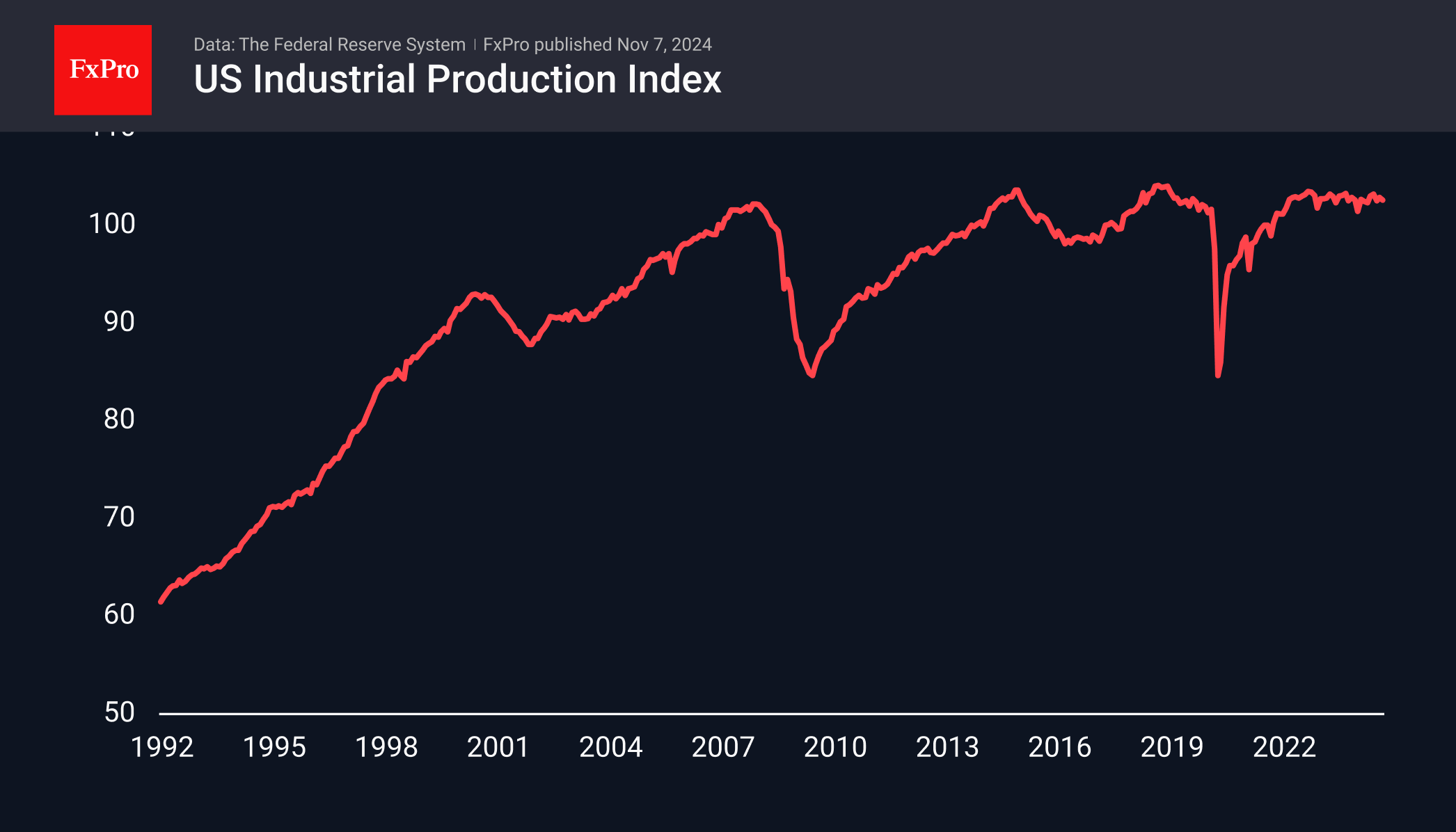

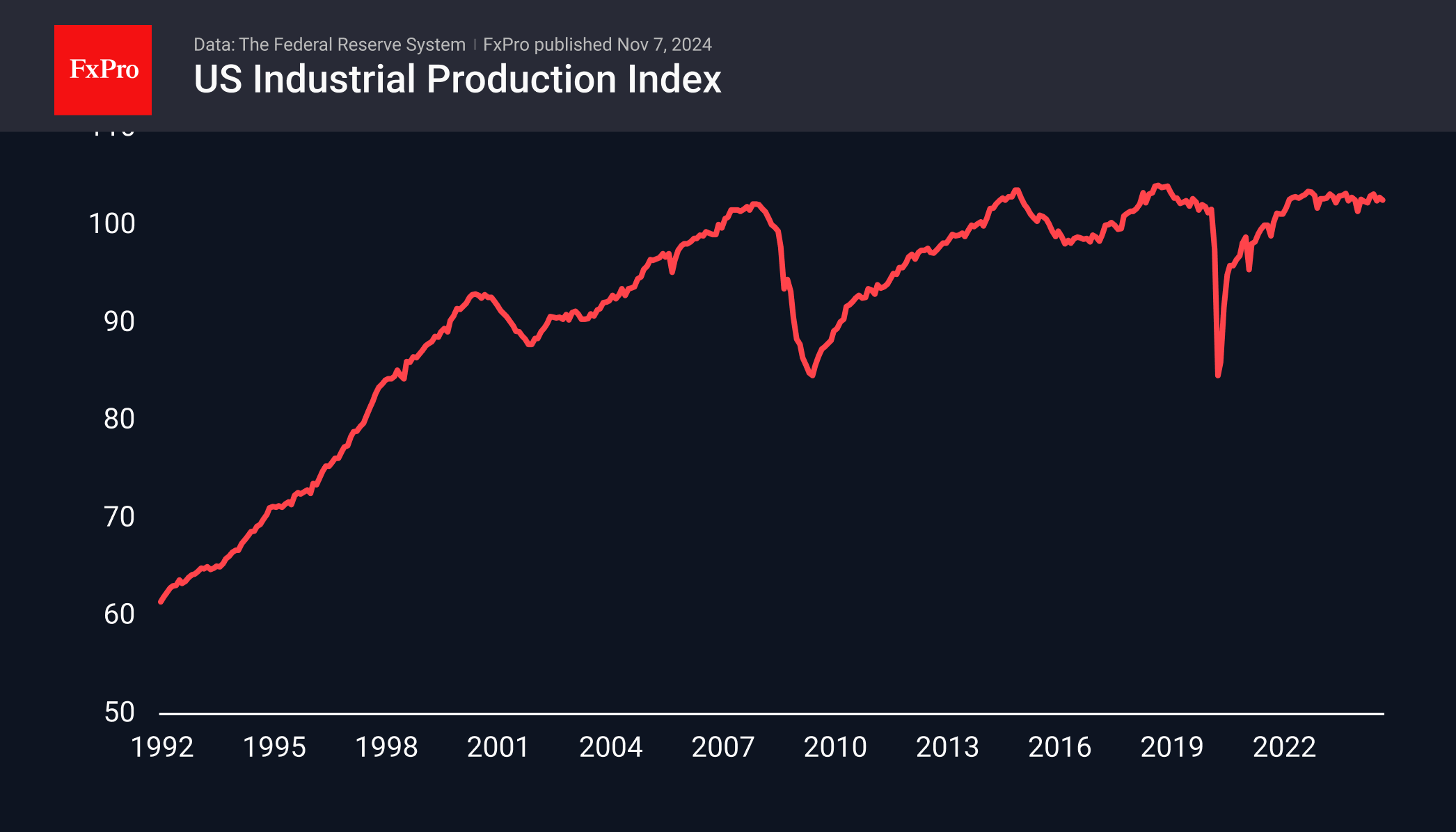

By Friday evening, the focus will shift to retail sales and industrial production in the US. Sales growth has not kept pace with inflation, falling in real terms in recent months, but this is not much of a concern because of the overall upward trend, which allows a recession to be rejected.

US industrial production has been stagnant since about the beginning of last year, a little short of the peak levels of 2015 and 2019. It is possible that with Trump in power, there will be an increase in this index. Then, the index from 2017 to 2019 was down by about 5%, but don’t expect a quick effect. It could take a year for that to happen.

The FxPro Analyst Team