Yesterday the head of the Federal Reserve Powell announced changes in the monetary policy framework. The main changes concern the desire to maintain an average 2% inflation, compensating for periods of lower inflation with times of higher price growth.

The foreign exchange and stock market reaction was mixed. The euro and pound fluctuated more than a 1.2% range in the first few hours after Powell’s address.

Fundamentally, pronounced changes imply softer monetary policy in the coming months and even years as the Fed will focus on restoring employment while taking a relaxed view on inflation.

Naturally, the approach will be symmetrical, so the Powell inflation acceleration promises to compensate for a period of increased inflation suppression, which, on the contrary, will someday be positive for the dollar.

The market reaction can also be seen as a “buy the rumour, sell the facts” strategy. Announced changes were widely expected by knowledgeable market participants, that partly pressured the dollar in previous weeks.

Moderately positive for the dollar is also the fact that the Fed still refuses to adopt a negative rate policy, preferring to keep rates at zero for longer.

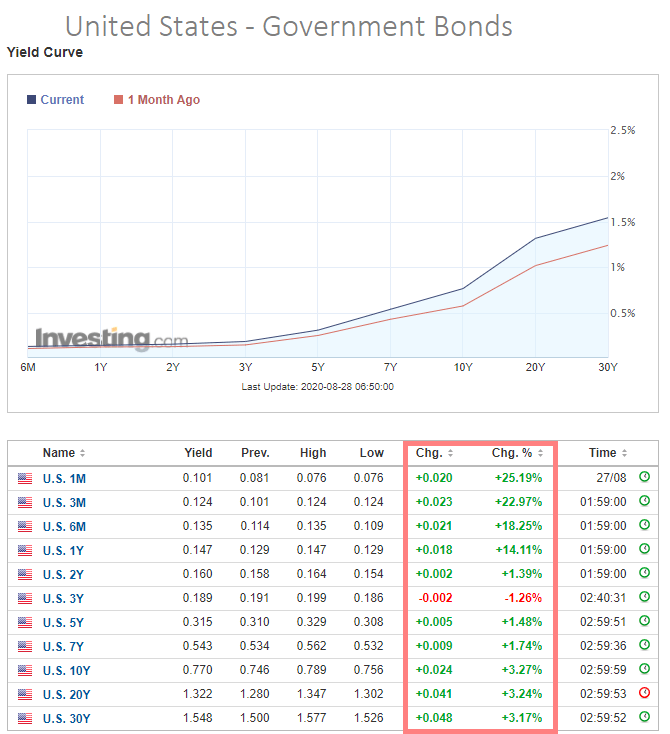

However, outside of short-term market fluctuations, the announced changes in monetary policy may hurt the US debt market. After all, investors will now put into quotes a methodical weakening of the dollar’s purchasing power.

Rising yields (falling prices) on US bonds have previously often been accompanied by sell-offs in emerging debt markets. But then, we saw a flow of funds from long-term US government bonds into short-term bonds. On Thursday, however, the most powerful sell-off was in shorter-term Bills.

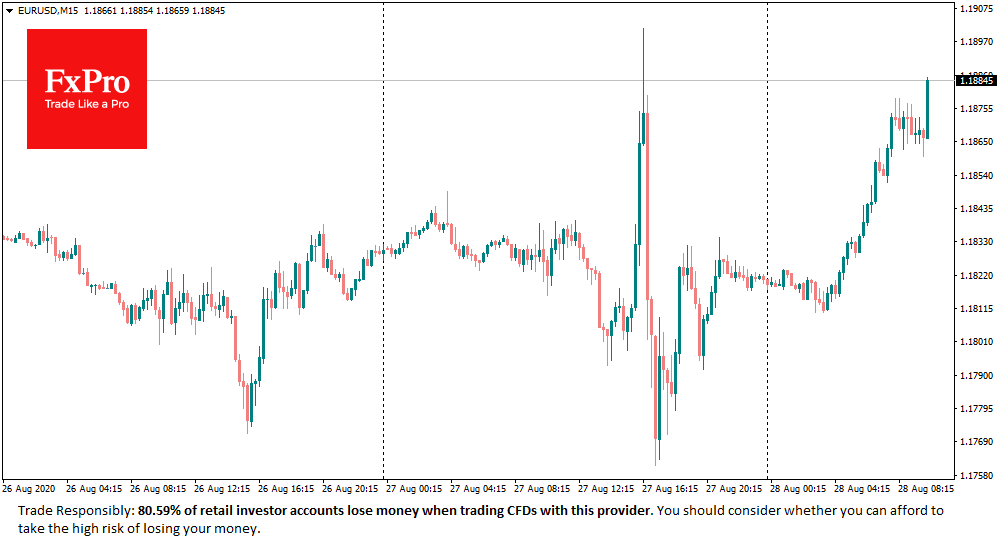

On Friday morning, the pressure on the US currency has returned. EURUSD traded at 1.1870 against a peak of 1.1900 on Thursday on initial reactions to Powell and bottomed at 1.1760. GBPUSD has again approached its highs from December 2019 above 1.3260.

The Australian dollar, an excellent indicator of risk demand in the foreign exchange market, rose above 0.73, reaching highs from December 2018. The Chinese Yuan is close to this year’s highs at 6.86 for USD.

The debt and currency markets are signalling a sell-off in US debt securities, which could put severe pressure on the dollar, finally ending a 9-year trend of USD strengthening. Potentially, changes in Fed policy are laying the foundation for a multi-year weakening of the US currency against European competitors.

We may also see a repetition of the commodities bull market in the coming years, as was the case in 2000-2008 when the dollar was under systematical pressure.

The FxPro Analyst Team