In March, cash was the number one choice for both stock players and the public. Demand for the dollar is off the charts from the population, and even more so – from the business. The Fed is unprecedentedly pumping the markets with money in an attempt to support lending and satisfy the financial market’s dollar thirst.

Judging by the currency market reaction, where the dollar index skyrocketed since the last week even against the developed countries peers, the thirst is not nearly quenched. Among them, Britain and Australia were particularly vulnerable, whose national currencies lost 13% and 14% since the beginning of last week to 35- and 17-year lows, respectively. The yen, the franc, and the euro have also declined over this period. However, they just returned to late February or early March levels, while the pound and Aussie collapsed into an abyss.

The central banks of developed countries continue to press the monetary easing pedal. And this is a traditional way for them to support the economy in the face of a looming recession.

What goes beyond tradition is the reaction of the central banks of emerging market countries. Brazil, Turkey, Ukraine, and many others, following China, have turned a blind eye to the collapse of national currencies and the risks of capital outflows, and softened their monetary conditions along the lines of developed countries. Yesterday the Bank of Brazil reduced its policy rate by 50 points to 3.75%, although the real has lost more 20% YTD. The Bank of Turkey reduced its rate three times this year, cut it by 225 points. Indonesia, Taiwan decreased their rates this morning, too.

This is an anomaly because earlier in the conditions of outflow of investors, central banks of developing countries sharply increased rates to maintain investor interest in high-yielding currencies. Now their focus has shifted from attracting money to preserving already attracted investors and the desire to support lending within the country.

In times of heightened market volatility, investors are demanding a higher premium on bonds in emerging and troubled developed economies. In contrast, higher interest rates intensify their short-term decline. The economic damage is even worse, as the economy will stop due to a double shock: currency volatility and interest rate hikes.

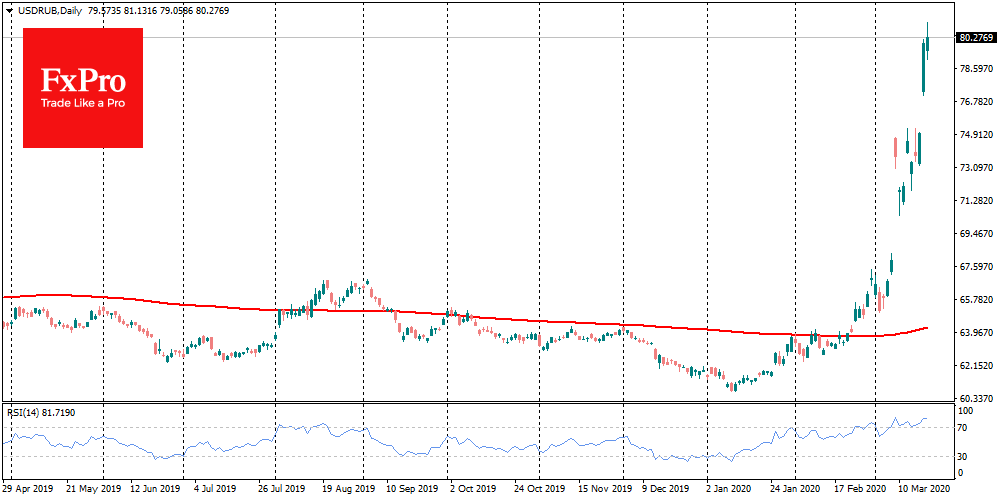

On Friday there will be a meeting of the Bank of Russia, which may confirm or deny the trend of other central banks. The Russian ruble has lost 23% against USD so far this year – the most significant drop among the 40 most popular currencies.

Initially, analysts expected tightening of the policy, suggesting to see the same response as in the previous currency crises. However, the reaction of monetary authorities of other countries makes us expect that the Russian central bank will give priority to the country’s economy and not to the currency rate.

It may sound paradoxical, but in this case, the rate cuts may even support, not weaken, the ruble. This is what we saw in Australia in 2009 and earlier today, which is also heavily dependent on commodity prices and experienced a currency shock after the global financial crisis. The decisive easing provided investors with confidence that the economy would be on the mend faster and even led to the growth of the Aussie at the time. This could also work for other currencies.

The FxPro Analyst Team