Economy may be the reason for ECB rate cuts

December 01, 2023 @ 10:36 +03:00

The euro was down 0.5%, close to 1.09, on a continuing wave of weak data from Germany and the eurozone, reinforcing expectations of a policy reversal.

Wednesday saw weak inflation reports from Germany and Spain. On Thursday, equally weak French (-0.2% m/m and 3.4% y/y) and Italian (-0.4% m/m and 0.8% y/y) data added to the feeble inflation picture. For the entire eurozone, price growth slowed in November from 2.9% to 2.4% y/y, the lowest since July 2021. Core inflation is not falling as fast, dropping to 3.6% y/y.

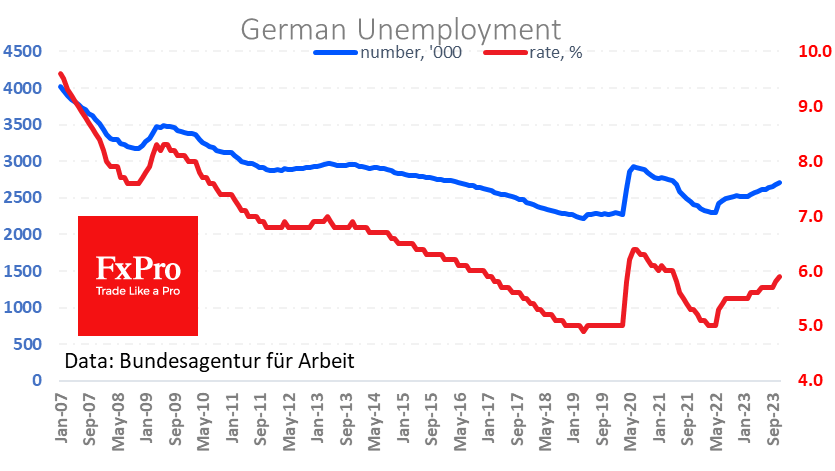

This return to normal comes at a high price. Europe is losing jobs, as seen in 10 months of non-stop jobless growth in Germany. The unemployment rate there rose to 5.9% in November, having bottomed out in February-May 2022 at 5%.

Fresh data also showed a 0.9% drop in personal spending for October – after zero change in September and a 0.6% decline.

Weakness in the labour market and consumer spending form the basis for a monetary policy reversal. Building on the weakness in demand, the ECB may move to cut rates before inflation steadily returns to target. By comparison, in the US, inflation is slowing, but the labour market continues to create jobs, requiring current rates to be maintained at the very least.

We would not be surprised if, in the coming weeks, debt market traders markedly lower their rate forecasts for next year, pushing the single currency down against its major peers.

The FxPro Analyst Team