Crude’s U-turn. Maybe heading for $75

October 03, 2023 @ 16:35 +03:00

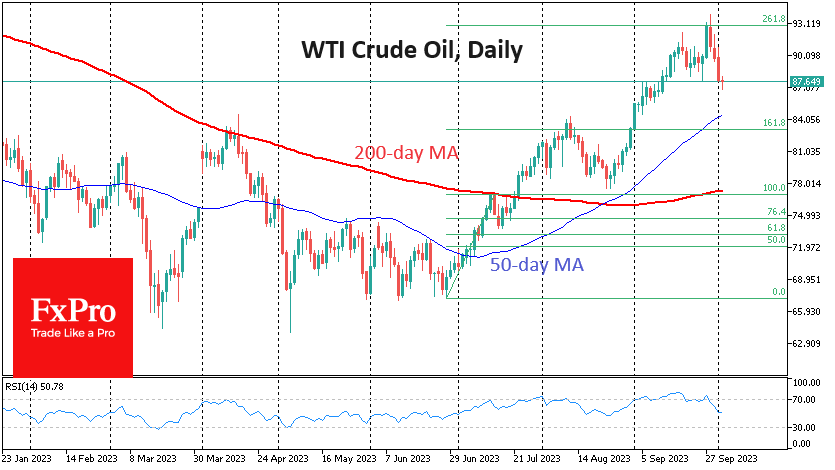

Oil prices fell for the fourth session after hitting 13-month highs. The spot price of a barrel of WTI approached $94 in what looked like a desperate last-ditch attempt by the bulls to assert their superiority.

However, this appeared to be the third wave of gains in the rally since the price collapse in June. Since last Thursday, intraday rallies have been suppressed by heavy sell orders. WTI briefly dipped below $87 on Tuesday, down 7.5% from last week’s peak.

Concerns over a slowing global economy triggered heavy sell orders that overwhelmed intraday rallies. This sustained pressure appears to be more than just a moment of market cooling and is in line with the typical wave pattern, which now suggests three downward impulses.

Last month, RSI formed a divergence on a daily timeframe when a higher price peak coincided with a lower oscillator peak. This is often a sign of exhaustion of bullish momentum. It is also important to note that the index has already retreated from the overbought zone, indicating the start of the decline.

Potentially, the next downside target is the $84.4 per barrel area. The 50-day moving average and peaks in early August and mid-April are concentrated here.

However, oil could go even lower. The global economic slowdown and falling final demand are now working against it. Moreover, black gold has long been rising against a rising dollar and falling markets. And now it may well catch up with the markets, which are falling, with redoubled strength.

An essential signal from exporters: reports of rising oil exports from Russia and Saudi Arabia last month, reducing the market deficit and raising questions about whether the cartel’s production ceiling is as firm as it seems.

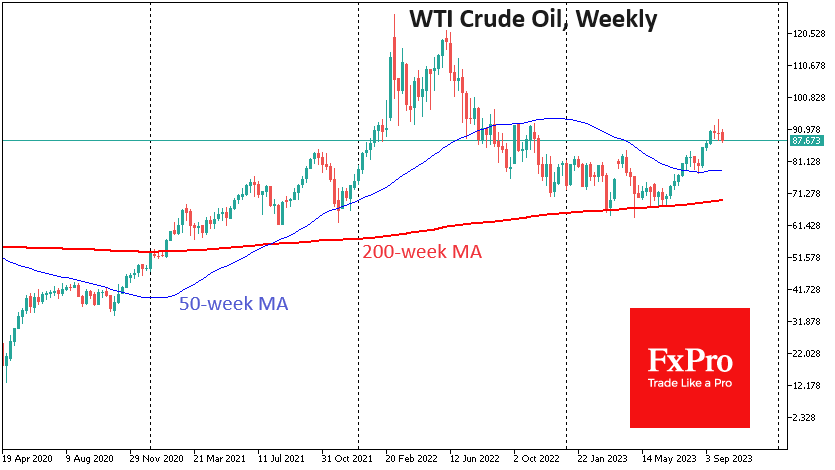

More solid support for oil may only come with a drop to $78. That’s the 50-week moving average, but we wouldn’t be surprised to see a drop to $75 by the end of the year. These are high levels by historical standards, but they no longer look like a drag on the economy and a good reason for further policy tightening.

From a global perspective, lower oil prices will now be a boon for equity indices rather than a sign of waning risk appetite, as is usually the case.

The FxPro Analyst Team