Volatility Markets Brace for Election Drama Like Never Before

August 28, 2020 @ 18:37 +03:00

Traders across major asset classes are sending the same message: Prepare for what could be the most-contentious U.S. presidential elections in decades.

One measure of hedging in the stock market is higher than at any point in the past three presidential elections. In the interest-rates market, implied volatility is well above levels reached in 2016 or 2012. And three-month implied volatility in the dollar-yen pair — a classic haven trade — has risen above the two-month tenor by the most in two decades, signaling demand for protection from turbulence near Election Day.

Trades protecting against election-induced volatility have been around all year, with “unprecedented” levels of hedging seen as early as January. Yet the potential for drama has only grown since then as the coronavirus leaves the U.S. mired in a recession and President Donald Trump rages against mail-in voting, raising concerns about a prolonged dispute over vote tallies. That uncertainty is complicating more conventional topics, such as how the results will affect tax policy and the trade war with China.

The November election is shaping up to be the most-contested in modern U.S. history, as changes to balloting prompted by the coronavirus fuel legal challenges that could stall the outcome for days or weeks.

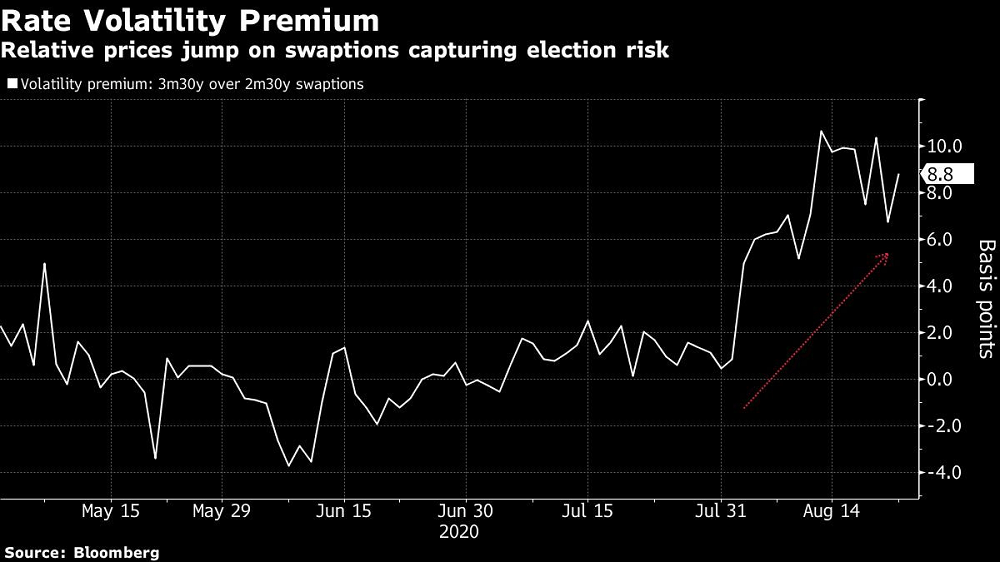

One area that highlights how much traders are bracing for election drama is swaptions, or options on interest rate swaps, which typically mirror the overall direction of Treasury yields. Wells Fargo analysts found that Election Day is priced for four times the volatility of a “typical” trading day in this market, based on the difference between at-the-money volatility on two-month and three-month swaptions on 10-year interest rate swap contracts. That compares to roughly two times at a similar point in the 2016 election cycle and about 1.7 times during the 2012 campaign, they wrote in a note.

The election premium in swaptions is most pronounced in contracts for longer maturity swaps, such as those with 30-years to maturity, according to Goldman Sachs Group Inc.

Though the Cboe Volatility Index — known as the VIX — has been grinding lower since March’s dizzying peaks, anxiety is building for contracts tied to it that are meant to protect against stock-market losses. October VIX futures — which reflect the market’s expectations for volatility from Oct. 21 to Nov. 21 — are elevated relative to both September and November contracts. That “kink” in the term structure is roughly 3 volatility points higher than the average VIX curve at this time before past presidential elections, according to UBS Group Inc.

The spread between September and October VIX futures is already higher than at any point in the past three presidential elections. Currently, the October contract is trading 3.75 vol points above September’s — in 2012, the gap was 2.5 percentage points at its widest point, according to Susquehanna Financial Group LLP.

The dollar-yen pair also shows signs of larger-than-normal election hedges, with the spread between two- and three-month implied volatility touching its highest level since November 1999 last week.

Volatility Markets Brace for Election Drama Like Never Before, Bloomberg, Aug 28

April 17, 2024 @ 17:10 +03:00

April 16, 2024 @ 17:37 +03:00

April 15, 2024 @ 16:30 +03:00

April 15, 2024 @ 13:53 +03:00